Pinduoduo (NASDAQ:PDD) continues to sizzle higher as investors welcome China’s great reopening together with the fact that Pinduoduo is just so cheaply valued.

I’ve been an ardent Pinduoduo bull for some time. In fact, just over a month ago, I wrote,

[…] according to my own estimates, I believe that if PDD were to grow its operating profits next year by 25% y/y, that would see Pinduoduo’s full-year GAAP operating profits reaching $6.3 billion.

Of course, I believe that this figure is extremely conservative. But there again, even my extremely conservative estimate is dramatically higher than what analysts are expecting.

So, either I’m extremely foolish and wrong in my expectations. Or analysts’ financial models are fully inadequate. It’s probably a bit of both.

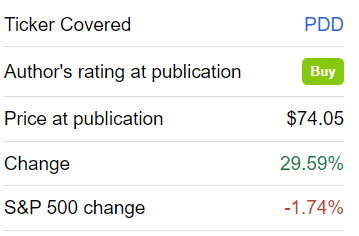

PDD author’s work

Less than 2 months later, with the stock up significantly, what should investors now think about?

What’s Happening Right Now?

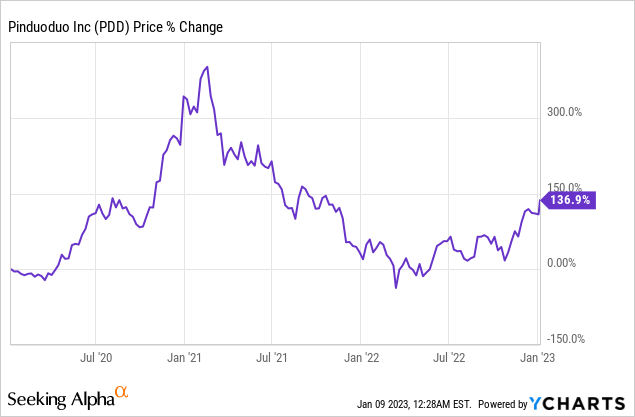

Investing in hindsight is always easy. What makes me say so? Consider just how volatile Pinduoduo has been in the past 3 years.

The stock soared higher, then dropped lower abruptly and kept dropping. And now, with the news out of China becoming steadily more welcoming, this cheaply valued stock has sprung back to life.

Pinduoduo in a Nutshell

Pinduoduo is a very young e-commerce company.

Pinduoduo is both similar and different to many e-commerce platforms we are well accustomed to in the West. What’s similar is that Pinduoduo gets a cut for joining both buyers and sellers.

What’s different is that Pinduoduo is much more interactive than the online shopping experience we are accustomed to in the West. Pinduoduo is a social shopping experience, with live-streaming as part of its platform.

Pinduoduo sells electronics, beauty, and cosmetics. But where its strong focus comes into play is in digitalizing agriculture. That means connecting farmers with consumers.

Pinduoduo wants to disrupt the way we purchase agricultural products. How products go from farmers’ fields and farmers can cut out some of the indirect suppliers and operators, leading to the food ultimately landing at the household’s table.

How does a farmer benefit from this? By knowing what products households are actually interested in buying, and better servicing that demand, farmers are able to raise their prices and can stop growing lower-yielding crops and products.

Put simply, it provides farmers with the tools to know how to better service households’ needs. This avoids agriculture waste too, which indirectly increases farmers’ pay.

Can You Remember the Bear Case?

The bear case facing Pinduoduo is that the business couldn’t possibly ever become profitable, as its core customers ”only” shopped on the platform because its customers were given coupons that heavily discounted its merchandise. And that once Pinduoduo cut back on its coupons, its growth rates would implode and its earnings growth rates would become negative.

That being said, for Q3 2022 Pinduoduo’s earnings were clearly very strong on both a GAAP and non-GAAP basis. This led me to state in my previous article:

[…] consider this, analysts presently expect that from seasonally strong Q4, and well into the next several quarters, non-GAAP EPS figures are going to be at least 30% lower than the recent non-GAAP EPS figure. I’m speechless.

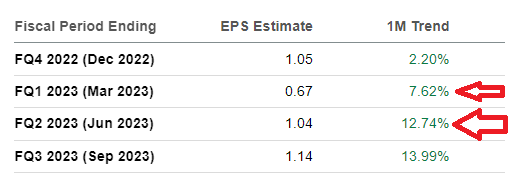

Since I made the above statement, observe what analysts have been busy doing:

PDD EPS consensus estimates

That’s right. Analysts have been upwards revising Pinduoduo’s EPS estimates. Indeed, H1 2023 in particular has been upwards revised by high-single digits to low double digits, in the past month alone!

What this is telling you is two things. Firstly, Pinduoduo is expected to continue to be profitable in 2023. That in and of itself shatters the bear case that investors had against the stock.

Secondly, and perhaps more important, Pinduoduo’s earnings are rising. And fast.

PDD Stock Valuation – 19x GAAP Operating Profits

In my previous article, I argued that Pinduoduo is likely to report $5 billion in operating profits in 2022. I continue to believe that’s likely.

For 2023, as I noted in the introduction, I believe that $6.3 billion is very much inside the realm of what’s possible.

That means that by estimates, Pinduoduo is still priced at 19x this year’s GAAP operating profits. For a business that’s clearly rapidly growing, I believe that paying anything less than 25x GAAP operating profits provides investors with an ample margin of safety.

In sum, for now, the stock is still cheap enough to provide investors with a much-needed margin of safety.

The Bottom Line

Pinduoduo is set to benefit from a change of sentiment towards cheaply valued Chinese stocks.

As investors, there’s probably no better setup to be long a stock than one that has three tailwinds to its back.

The stock is bombed and significantly down from its highs.

There’s a catalyst that’s driving a change in investors’ sentiment.

Analysts are upwards revising the company’s earnings.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment