William_Potter

Chinese stocks have been incredibly popular over the past couple of months, since the Chinese ruling party has initiated a complete reopening of the economy following two years of strict zero-COVID policy. Pinduoduo Inc. (NASDAQ:PDD), as many other Chinese stocks rallied consistently since then as many international investors are starting to move money again in the sector. Moreover, the tension between the U.S. government and the Chinese communist party has relaxed a bit, and Pinduoduo together with other major U.S.-listed Chinese companies seem to have put on hold their plans to list on the Hong Kong stock exchange. The news is a clear sign that Chinese companies are feeling more comfortable with their U.S. listings given that the Chinese government has allowed regulators in the United States to access the audits of Chinese companies, a clear concession that has effectively deflated the risk of delisting.

The result after waves of good news is a complete shift in sentiment by the market. PDD shares are now trading for about $104 per share, basically double since October and up even a more astounding 225% since March 2022. The latest quarter release by the company back in November also helped alleviate some worries as the company returned to high growth and continued on their path to reach higher and higher profitability. Unfortunately, that means that the company’s shares are no longer a bargain after such a great rally and can now be considered at the most reasonably valued. For this reason, I consider Pinduoduo as a hold in this environment.

Pioneer in social commerce

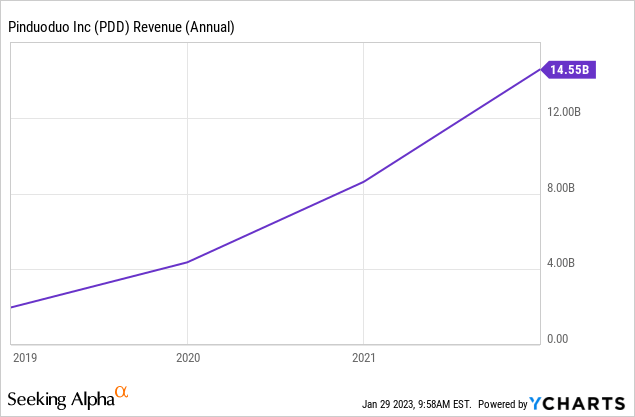

Pinduoduo operates a mobile e-commerce platform in China focused on the social aspect of commerce. Buyers are incentivized to share their finds on social networks, to pool together with friends and family to form shopping teams in order to unlock better value. This innovative model was a tremendous success: the company in 2017 generated only $268 million in revenue as per Seeking Alpha data. Fast forward a few years, and the company run rate for the past 12 months is $16.5 billion in revenue. In the meantime PDD has not reached consistent profitability both on a Free Cash Flow and GAAP Net Income basis.

YCharts – Seeking Alpha

Pinduoduo does not handle product fulfilment directly, which allows them to maintain a generally high Gross Margin (73% on average since 2019). They earn revenue primarily in two ways: Online marketing services and Transaction services. Online marketing services revenue is generated through services offered to merchants to operate their account, such as keywords bidding or advertising; Transaction services revenue is directly correlated to GMV and orders as Pinduoduo charges fees to merchants for managing the orders on the platform. To draw a comparison with a Western company, the model resembles more a company like Etsy (ETSY) rather than Amazon (AMZN), as Pinduoduo purely operates the online marketplace while leaving to the merchants the onus of fulfilment.

The company is very young, and it’s really hard not to be impressed by what the management has done in just 7 years of life. Although the e-commerce space in China is highly competitive, Pinduoduo has pioneered an innovative business model and is investing hard into brand recognition, a clearly successful endeavor, as after only a few years of activity it has become an ubiquitous brand in China.

Great results in the latest quarter

The company reported earnings for the third quarter on November 28. The stock reacted very positively thanks to strong top-line growth of 65% to $4.99 billion, as well as positive GAAP Net Income of $1.48 billion. Investors have cheered the return to blistering growth after the slowdown experienced during 2021, when the zero-COVID policy designed by the Chinese ruling party strongly tampered economic activity and consumer sentiment nation-wide.

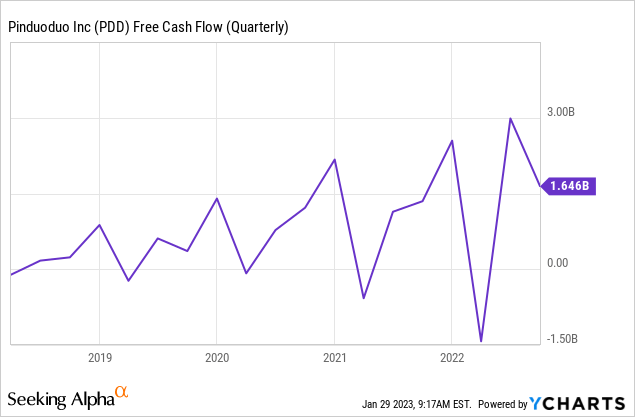

On a cash flow basis PDD has reported about $1.6 billion in cash from operations and only $50 million spent on investing activity, which would translate to about $1.550 billion of Free Cash Flow for the quarter. The quarter was definitely a bit of an outlier due to the very low amount of investments made, which was due to seasonality in investments as it already happened in the same quarter two years ago when the company reported only about $67 million of cash invested. Nevertheless, by considering the first 9 months of 2022 PDD has generated $3.0 billion in operating cash flow while using $1.9 billion for investing.

YCharts – Seeking Alpha

The company is clearly reaching meaningful scale and is hinting at amazing profitability going forward. In the latest quarter total Cost of goods sold grew only 13% YoY, while operating expenses grew 38%. Both growth rates are far lower than the top-line growth which directly translates to margin expansions.

On the same note, a key metric to monitor is growth in Sales and marketing expenses. This line of expense represents the lion’s share of operating expenses for Pinduoduo, as in order to grow very fast the company has heavily invested particularly into coupon issuance to buyers to entice them to join the platform. As for every e-commerce platform, attracting the highest number of buyers possible is paramount to the bull thesis as is the primary way to build a moat through network effect: the more buyers will attract more merchants, and the more merchants will in turn attract more buyers. The idea is that over time PDD will not need to actively invest anymore into marketing as the network effect will do the trick by itself.

The good news is that S&M expenses are indeed starting to slow. In FY2019, they represented 84% of total operating expenses, while in 2021 that share went down to 80.9%. Based on the latest filings, for the nine months ended on September 30 2022, this figure still trended in the right direction and actually came in at 78% of total operating expenses.

Valuation and key takeaways

Valuation is where my conviction for Pinduoduo Inc. starts to falter a bit. Currently, Pinduoduo is trading at a 2022FY Price to sales of 6.88 as per Seeking Alpha compiled data, against an average of the past 5 years of about 11.6. The revenue growth rate implied by the analysts is on average around 19% per year, projecting revenue for FY2025 of $32.8 billion (P/S of 4). During the same time period, earnings are expected to grow actually a bit slower than that at 17% per year, which would imply a FY2025 P/E of 16.

I won’t argue against these projections, as they actually appear to be quite reasonable. However, since the Pinduoduo Inc. stock price basically has doubled since October 2022, PDD does not appear to be such a bargain anymore. A reasonable valuation for a growth company could be good enough for some people, however, it now implies a high level of growth to justify the projected 2025 valuation, which adds too much risk for Pinduoduo Inc. in my opinion.

Be the first to comment