William_Potter

Thesis

In June 2022, I argued that Pinduoduo (NASDAQ:PDD) is a ‘Buy’. With the stock being up close to 110% since my writing, this has undoubtedly been an excellent call. However, my then base case target price was $62.99/share — a much less excellent call. Now, with the stock having doubled, and reflecting on the China COVID reopening push, it is a good time to revisit the investment thesis for PDD.

Although, I continue to be bullish on Pinduoduo’s pioneering business model and ongoing initiatives in agriculture technology, and although I upgrade my target price to $80.34/share, I view PDD as too richly valued to allow for a balanced risk/ reward opportunity. Accordingly, as a function of valuation concerns, I downgrade PDD stock to ‘Hold’.

The Reopening Thesis

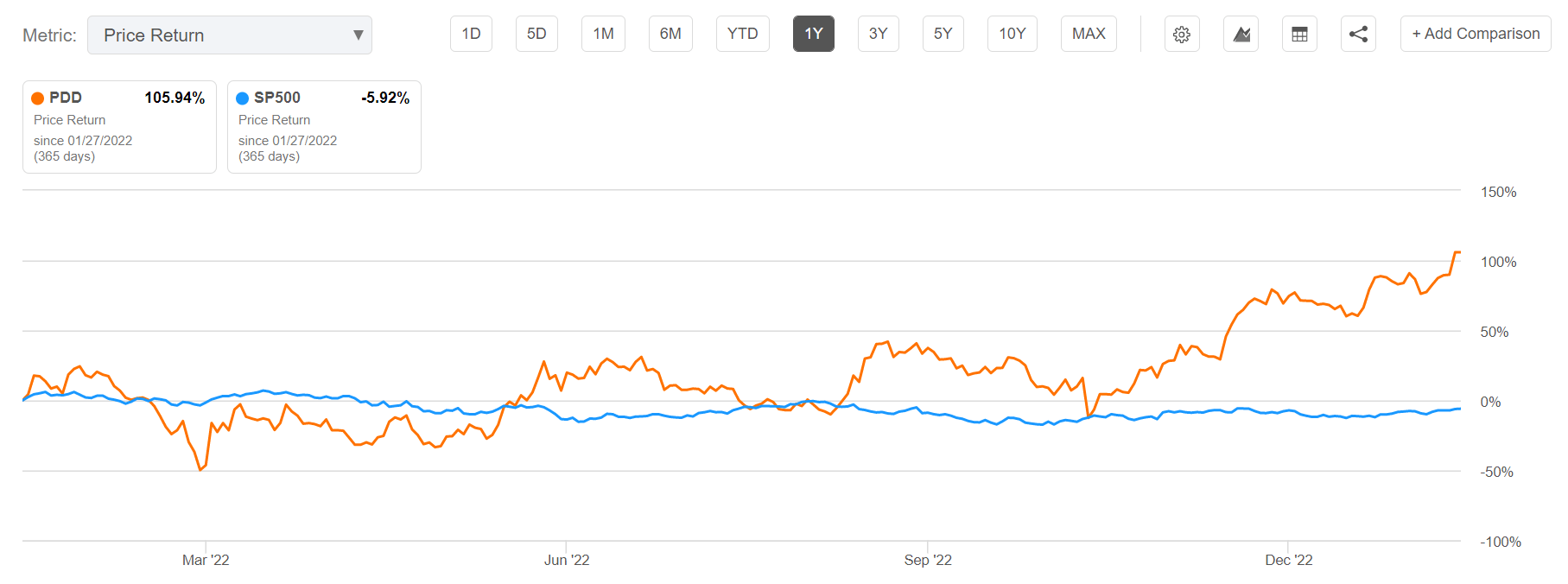

After being down close to 90% from all-time highs, Pinduoduo stock has rebounded sharply. For reference, for the trailing twelve months, PPD stock is up approximately 106%, as compared to a loss of almost 6% for the S&P 500 (SPY).

Seeking Alpha

There are a few reasons that might have contributed to the sharp price appreciation: Strong quarterly results, optimism surrounding the company’s international expansion, and the China COVID reopening trade.

Strong quarterly results

Despite an almost overwhelming collection of macro-economic challenges in China — that certainly need not be explained to SA readers –, Pinduoduo continued to post excellent results. In Q3 2022, the company generated total revenues of about $5 billion, an increase of 65% as compared to the same quarter of 2021. The company’s operating profit for the quarter jumped to $1.5 billion, an increase of 388% respectively.

For the trailing twelve months, Pinduoduo’s revenues have expanded to $16.6 billion, and the firm’s operating income has grown to approximately $4 billion. Given that TTM operating income almost quadrupled as compared to FY 2021, it is no surprise that investors and speculators have a hard time not being bullish.

For reference, see below PDD’s 5 year top line growth and profitability snapshot.

Seeking Alpha

Seeking Alpha

Optimism in context of international expansion

Positive sentiment in relation to Pinduoduo’s expanding top line and profitability was certainly complemented by the e-commerce giant’s successful first initiative towards international expansion. In late 2022, Pinduoduo launched Temu, the company’s first US storefront. The platform offers discounted products, mostly sourced directly from China and has enjoyed enormous success in a short period of time: Since its launch in September, Temu has amassed close to 20 million installs in the US and has consistently been one of the most downloaded apps across all categories in the US. In fact, information collected from data.ai highlights that in the January period Pinduoduo’s app Temu has claimed the number one spot in ‘free’ app downloads for both IOS and Google’s Android. With Temu, Pinduoduo aims to achieve $30 billion in sales within five years.

The China COVID reopening trade

As COVID restrictions in China are lifted, the domestic economy is expected to experience a strong and rapid recovery. This boost is expected to be particularly evident in the first and second quarters of 2023. To provide context, while the Chinese economy only grew by around 3.3% in 2022, Goldman Sachs predicts that it will expand by 4.5% in 2023, while Morgan Stanley estimates GDP growth for 2023 to be at 5.4%.

In any case, the reopening will likely be a catalyst for an enormous consumption spree. According to estimates, Chinese households are sitting on approximately $2.6 trillion of bank deposits. If parts of these savings are considered ‘pent-up demand’, then the reopening will likely push-up Pinduoduo’s top line considerably.

Too Much Optimism?

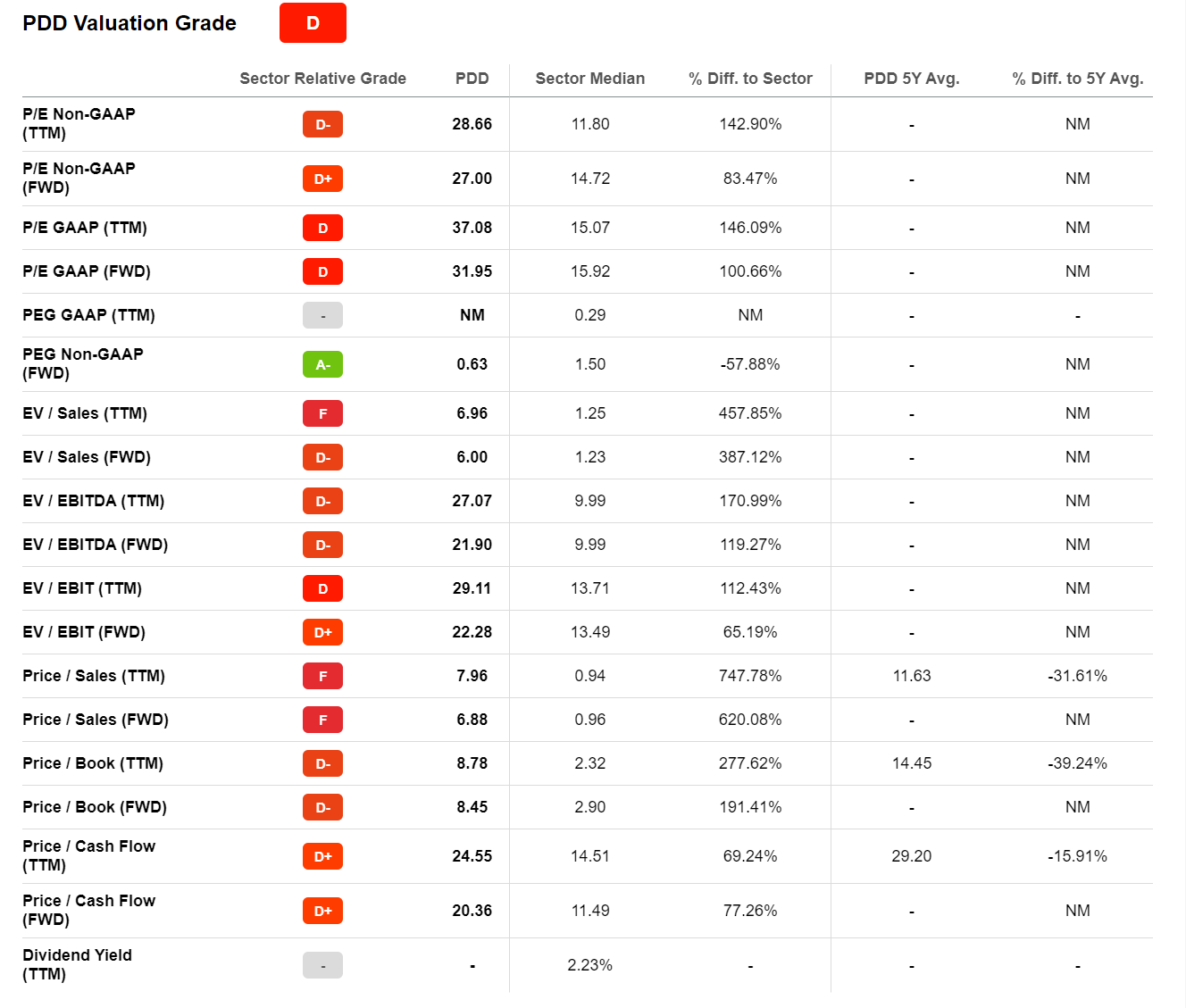

With so much optimism surrounding Pinduoduo’s fundamentals, business strategy and macro environment, the stock has been priced accordingly in my view. According to data compiled by Seeking Alpha, PDD stock is currently priced at a FWD EV/Sales of x6 and an EV/EBIT of x22.3. Notably, these multiples reflect a premium to the median industry valuation of about 390% and 65% respectively.

Seeking Alpha

Personally I believe that investors might be pricing too much growth. While China’s COVID reopening is likely a positive for Pinduoduo, investors should consider that the company was arguably a net beneficiary of the lockdowns, as restrictions pushed the need for online shopping of agricultural products, and food/ grocery in general. In my opinion, insights from the next 2-3 quarters would be needed to make any conclusion how sustainable Pinduoduo’s past business expansion has been.

Moreover, Pinduoduo’s growth in the US, despite initial successes, remains risky. With high inflation and pressured consumer sentiment, shoppers turn to low-cost platforms such as Temu. But can Temu capture a strong margin from such cost-conscious consumers? I somewhat doubt it. Moreover, isn’t the e-commerce market in the US not saturated enough already, with exceptionally strong players such as Amazon (AMZN) and Walmart (WMT)?

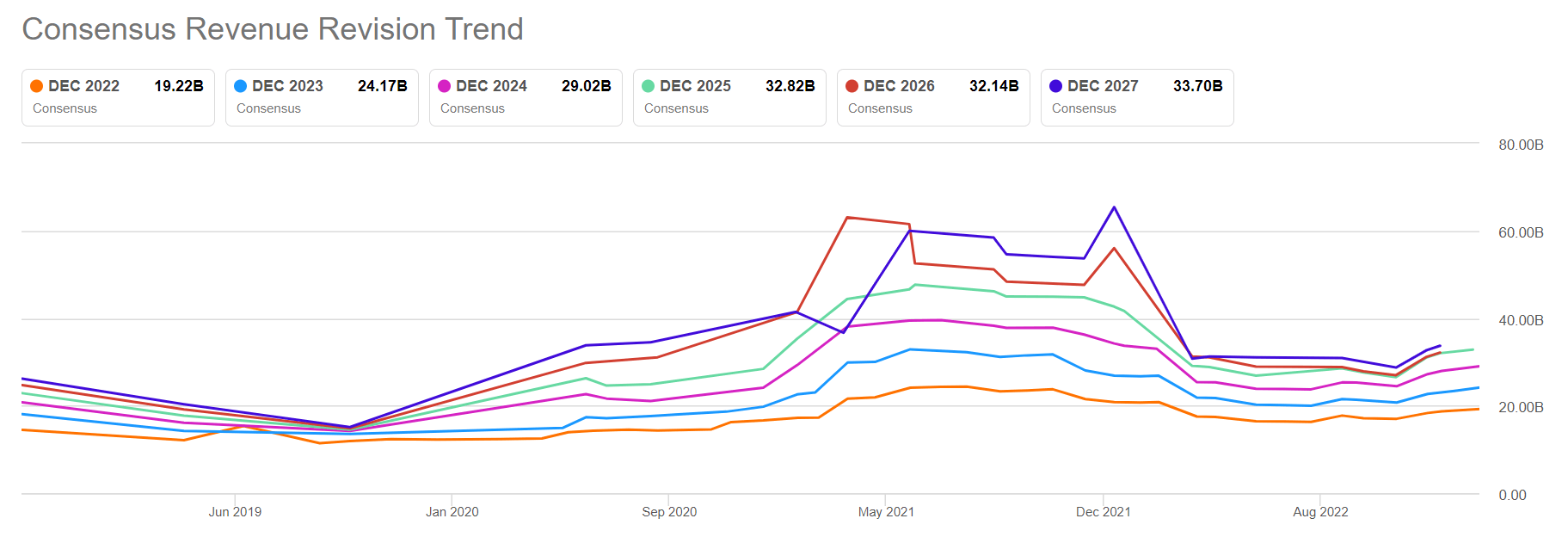

Analysts’ predictions seem to agree: Consensus expects that Pinduoduo’s top line will expand to about $33.7 billion in 2027, which would reflect a 5-year CAGR of approximately 12% with 2022 as the baseline–and a sharp slowdown as compared to Pinduoduo’s growth in the period from 2019 – 2022.

Seeking Alpha

Target Price: Raise To $80.34

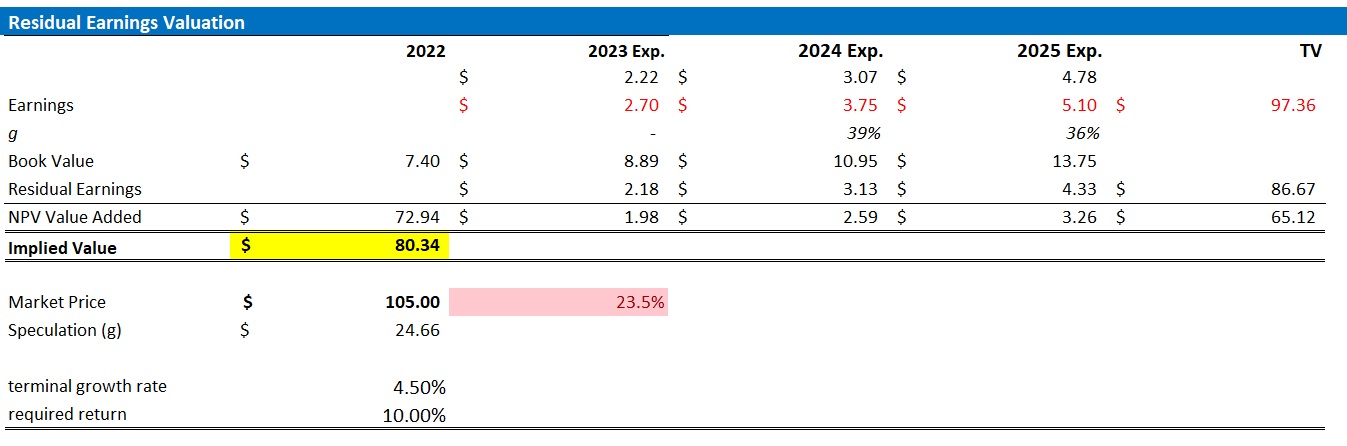

Expecting a sharp economic rebound in China, I estimate that PDD’s EPS in 2023 will likely expand to somewhere between $2.5 and $2.9. Moreover, I also raise my EPS expectations for 2024 and 2025, to $3.75 and $5.10, respectively.

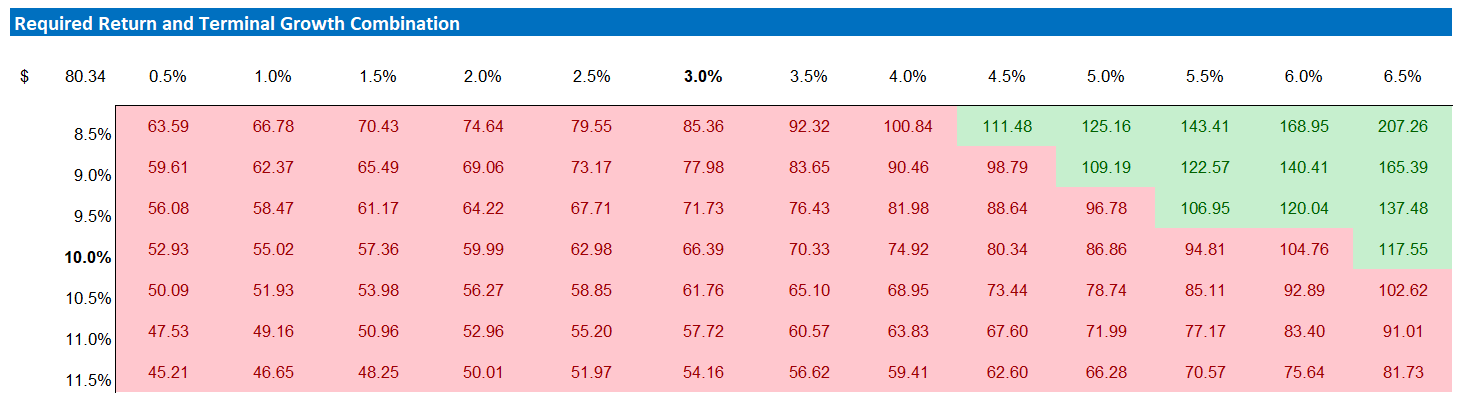

I continue to anchor on a 4.5% terminal growth rate (one percentage point higher than estimated nominal global GDP growth), as well as on a 10% cost of equity.

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price of $80.34.

Author’s Estimates and Calculations

Below is also the updated sensitivity table.

Author’s Estimates and Calculations

Conclusion

I continue to be bullish on Pinduoduo’s pioneering business model and ongoing initiatives in agriculture technology. And there are lots of reasons to be optimistic about the company’s near-term future, including (1) strong quarterly results, (2) optimism surrounding the company’s international expansion, and (3) the China COVID reopening trade. However, although I upgrade my target price to $80.34/share, I view PDD’s $105/share currently as too richly valued to allow for a balanced risk/ reward opportunity. And accordingly, as a function of valuation concerns, I downgrade PDD stock to ‘Hold’.

Be the first to comment