anilakkus

Investment Thesis

The global market for tobacco products went from worth $234.84 billion in 2021 to $250.51 billion in 2022, a growth rate of 6.7% per year. At least in the short term, the Russia-Ukraine war made it harder for the world economy to get better after the COVID-19 pandemic.

At a compound annual growth rate [CAGR] of 3.5%, the market for tobacco products is expected to hit $287.09 billion by 2026. Today, there are 8 billion people worldwide; by 2050, that number is projected to rise to 10 billion. This will lead to increased demand for tobacco products down the road.

As one of the best tobacco businesses in the world and a stock recommended as a best buy by motley, Philip Morris International Inc. (NYSE:PM) has a higher opportunity of benefiting from this expansion. This is a solid dividend-paying firm. Although the company has specific financial issues that need to be addressed, its overall state is not terrible. When comparing the stock’s current price to its true worth, I conclude that it is attractively underpriced and recommend buying it.

Financial Health

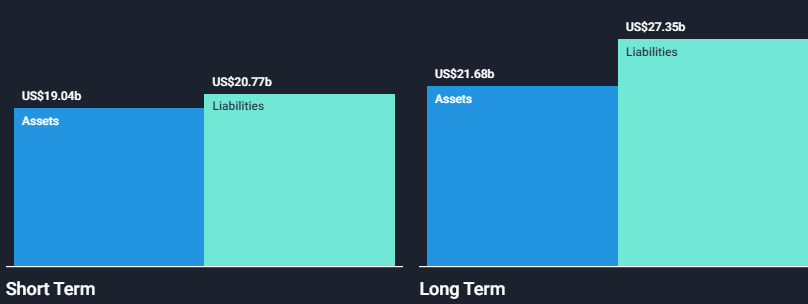

The company’s financial stability is critical in determining its worth and estimating its future. If a company’s finances are in good shape, investors will place a higher value on it and look favorably at its prospects. Looking at PM’s financial health, the company has negative shareholder equity both in the short and long term, which is not a good attribute.

Wall Street

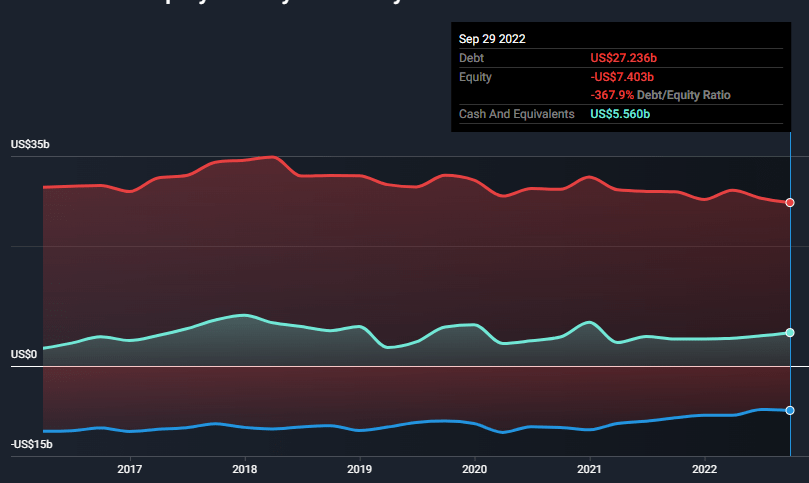

Additionally, despite having good liquidity of almost $6B, the company’s debt level is relatively high, with a debt of about $27B and equity of about -$7B. This translates to a debt/ equity ratio of -367.9%.

Wall Street

However, despite these worrying statistics, it is worth noting that its debt coverage is adequate. PM’s operating cash flow covers 43.1% of its debt, which I believe is a good coverage ratio. Further, Its EBIT is sufficient to repay its interest payments on its debt 25.1x. This relieves some of the pressure built up due to the company’s mounting debt.

Dividend

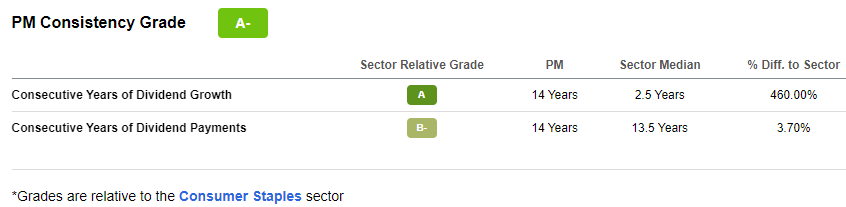

PM is a reputable company for its consistency n dividend payment. It has an appealing dividend history which is well above the industry medians. It has a 14-year growth history compared to the company’s average of 2.5 years. Further, the company has paid dividends consecutively for the last 14 years compared to the industry median of 13.5 years. This trend, in my view, makes the company one of the most dividend-paying companies in the industry.

Seeking Alpha

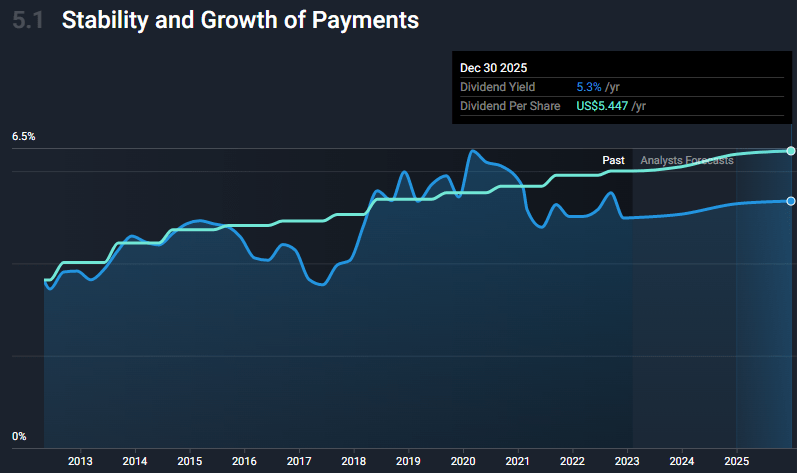

The company’s dividends per share have been pretty consistent in the last decade. Interestingly, estimates show that its dividend will keep growing way beyond 2025.

Wall Street

Its dividend yield of 4.99% places it in the upper quarter of dividend payers in the US market, above the top quarter’s yield of 4.22% and above the bottom quarter’s gain of 1.49%. I believe this is a desirable position for the company.

Earnings fully cover the current payout ratio of around 84%. It demonstrates the company’s dedication to returning a considerable share of its earnings to shareholders, which is important for long-term viability. Its cash payout ratio is roughly 70%; therefore, it is well covered by cash flows. The existing dividend policy is both appealing and sustainable for the company.

Valuation

According to Seeking Alpha’s valuations, PM is cheap relative to its competitors when measured by the P/E ratio. The stock trades at a discount of 18.12X to the sector average of 21.15X. However, this company is overvalued compared to the median PS ratio in its industry. Its P/S ratio is 4.98X, which is significantly higher than the average of 1.23X in its sector. Despite the plight of these two ratios, Seeking Alpha still assigns PM a B in valuation when all relative valuation criteria are taken into account, indicating that the stock is cheap.

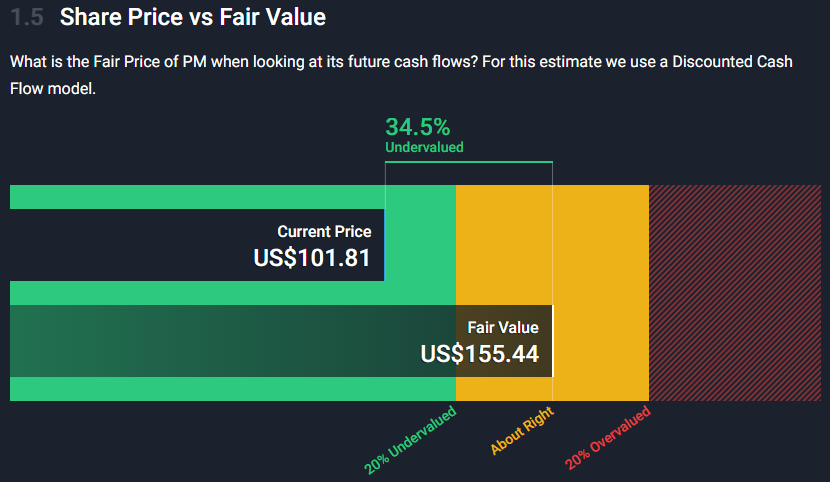

The fundamental question is, to what extent is this company undervalued? To answer this question, I will use the share value against the company’s fair value. Going by data from simplywall.st, the company is trading at $101.81, below its fair value of $155.44. This implies that it’s undervalued by about 35%, which is a good growth potential for the company.

Wall Street

Conclusion

Since the tobacco market is expected to grow, PM has a better chance of taking advantage since it is one of the best companies in the field. Over the years, the company has always paid dividends, and its dividend policy is very sustainable because its earnings are more than enough to pay for them.

In terms of valuation, the company is trading at a 35% discount, which is an excellent discount for people looking for a tobacco company that pays a steady dividend and is growing. As such, I give the company a buy rating.

Be the first to comment