DINphotogallery

Introduction

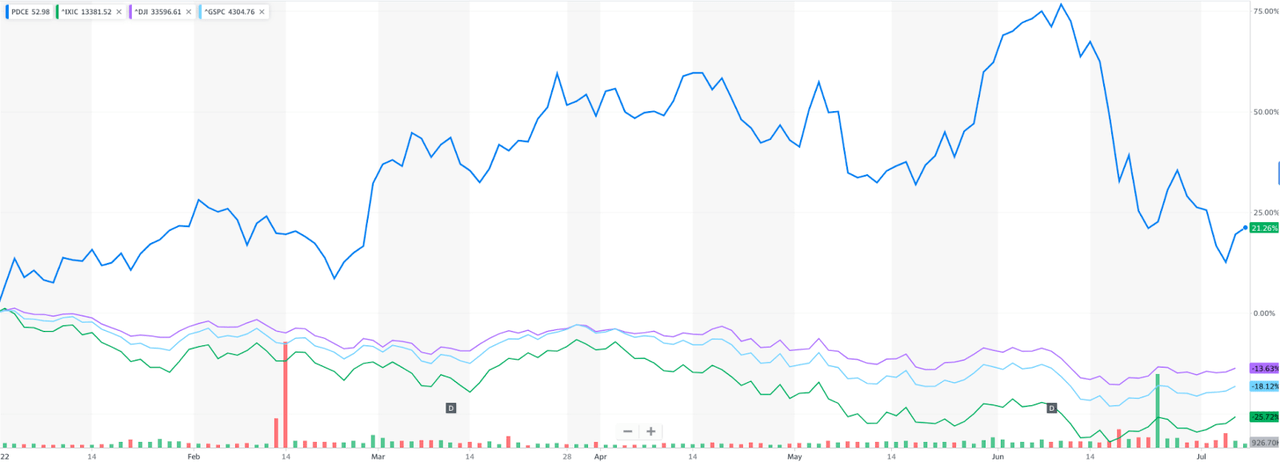

Year to date, PDC Energy (NASDAQ:PDCE) rose by 21.26% whereas broader markets and index funds have declined by over 13%.

Price Changes (Yahoo Finance)

I believe that PDCE is only seeing the beginning of its growth tailwinds, especially with catalysts such as long-term high oil prices being comparable to the times after the 2008 stock market crash. Additionally, this stock is recovering nicely from the pandemic. Its forward 5-year average EBITDA growth multiples are 99.46% above its sector median of 24.49%, suggesting above-average growth. I believe that there are a multitude of positive signs that investors are overlooking, such as the recent Great Western Petroleum acquisition leading to more capital return to shareholders and an increased likelihood of rapid approval of development plans for oil drilling sites in the near future. Let’s take a closer look at the primary drivers for my assumptions on a bullish outlook.

Company Activity

The company has now fully closed on the acquisition of Great Western Petroleum and with that shareholder returns are coming back. This acquisition leads to immediate growth in both material inventory and financial values. PDC Energy has a tremendous amount of FCF on hand and leadership appears confident in their business prospects. Here is a good quote from President and Chief Executive Officer Bart Brookman’s recent announcement on the future of the company:

We are excited to roll out our updated 2022 budget, which not only delivers top tier FCF generation of $1.7 billion each of the next two years, but also allows us outstanding shareholder returns of at least $1 billion annually. In the face of significant inflation, our operating teams have done a tremendous job innovating, driving additional efficiencies, and ensuring our capital budget remains at or below $1 billion. As we streamline our operations, the Great Western acquisition provides the Company with additional scale and high value inventory with increased shareholder returns.

The primary bullish signal presented here is the increased return of excess capital back to shareholders given that PDC optimistically is expecting to generate $1.7 billion in FCF for the next 2 years. This is great news and shows that PDC Energy is taking a step in the right direction to sustain and grow profits over time. More specifically, the detailed framework of shareholder returns is provided here by management:

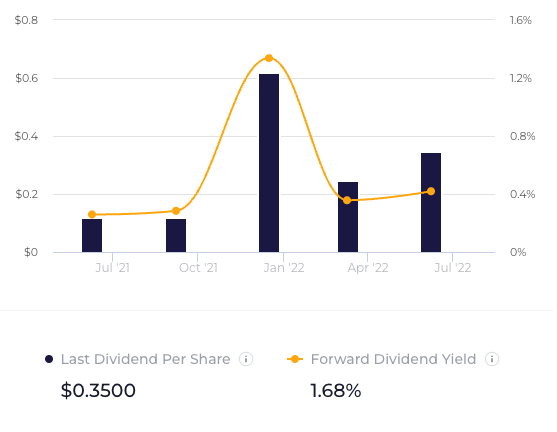

..at least 60% of FCF after base dividends will be returned to shareholders in the form of share repurchases and, if necessary, a year end special dividend. The Company has a $1.25 billion Board authorized share repurchase plan that it expects to fully utilize by the end of 2023. On May 26th, the Company’s’ board of directors approved a raised base quarterly dividend of $0.35 per share. The second quarter dividend is payable on June 23, 2022 to stockholders of record at the close of business on June 9, 2022. Based on our current estimated FCF and assuming we reach our annual $625 million share buyback goal, we anticipate that our year end special dividend could exceed $300 million.

The implementation of repurchasing programs and increasing dividend rates shows that the Board of Directors is well aware of the current undervaluation of the PDCE and is committed to increasing shareholder value for investors. Such actions will further supplement PDCE as a great investment for income-seeking investors as the company already is in the top 75% of US-listed companies for dividends. The company has reported strong EPS (EPS of $5.07) which is more than enough to cover the annual dividend per share of $1.34. This is fantastic news for investors.

PDCE dividend stability and growth (WallStreetZen)

More Oil & Gas Development Plan Success

Another reason why I am optimistic about PDCE is due to the major catalyst involving government regulations. PDC Energy recently announced on June 29 its third approval —Broe— in the last 12 months regarding their Oil and Gas Development Plan (OGDP) to permit 30 more drilling sites in rural Weld County, Colorado. In total, PDC Energy is rapidly expanding their arsenal of drilling sites to capitalize on the rising demand for oil/gas prices. Their recent news release gives us a better picture on this:

Combined with the previously announced Kenosha OGDP approval earlier this month, the Company has added 99 new wells to its inventory in June and will soon have over 675 permits and drilled and uncompleted wells (“DUCs”)

The rapid adoption and execution of the company’s OGDP shows that management is committed to investing in the future and is doing a good job of increasing their drilling footprint across the nation. With regards to what the future entails, I think that oil prices will still remain high for consumers and even rise. Since demand growth is outpacing supply growth, the oil market is likely to remain undersupplied. PDC Energy clearly has picked up on this and that these investments will help to increase the company’s operations and profits down the line.

2021 ESG Report

Stock Valuation

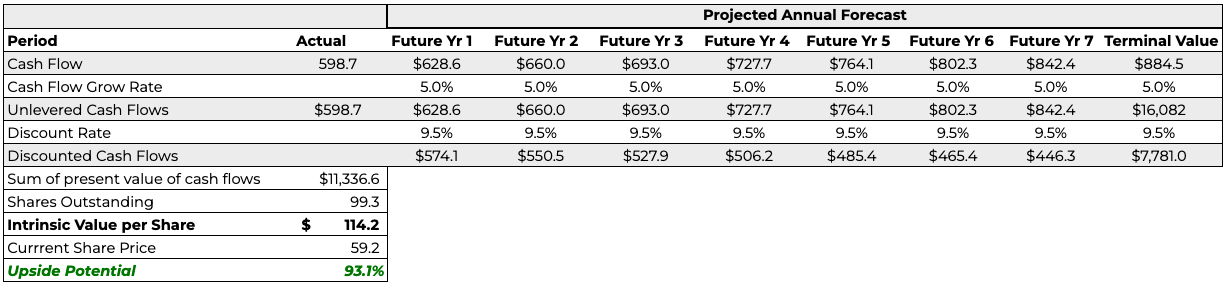

PDC Energy is operating with profitability and based on the management’s FCF projections for the company in 2022, I decided to use the Discounted Cash Flow method to predict how much PDCE stock is worth right now using baseline assumptions. First, I calculated the Weighted Average Cost of Capital to get a 9.5% discount rate. I then assumed a terminal growth rate of 4% to slightly outperform expected medium-term inflation rates. Lastly, using a conservative annual FCF growth rate assumption of 5%, my model resulted in an intrinsic price of $114.20 which represents a 93.1% upside potential. Expansion opportunities and acquisitions are already proving to be a success and it is likely that the FCF growth rate will be much higher than my current conservative assumptions.

Google Sheets

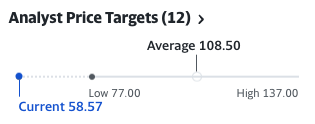

Additionally, my valuation is supported from multiple sources such as data from Yahoo Finance. The average price target among 12 analysts resulted in a mean price of $107.50 and the range spans $77.00 to $137.00. The lowest valuation estimate still represents at least a 30% upside from the current price of PDCE.

Analyst Price Targets (Yahoo Finance)

Risks

The biggest risk that stands for PDC Energy is the potential of oil prices dropping due to 2 factors: the end of conflict between Ukraine and Russia and the success of recent monetary policy efforts by the Federal Reserve. Right now, the Federal Reserve is raising interest rates to taper down the current inflation levels and many are speculating that the global economies are headed into a recession. If all of these do succeed, the demand for goods and services will see a decrease and directly lower oil consumption. However, with the war tensions between Ukraine and Russia showing no signs of stopping anytime soon, it is my view that oil prices will remain consistently high due to the undersupply and the Federal Reserve’s policy is not enough to offset enough demand to meet the low supply of oil.

Comparisons

Though PDCE is not an industry leader, the company ranks close to the top of the Energy Sector for shareholder return. What is impressive is the fact that PDC Energy has only been paying out dividends for only a year and is able to provide returns that are comparable with these companies in the energy sector. With increasing free cash flow generation and the company’s commitment to shareholder value, I think that PDC Energy has positioned themselves well competitively to outperform the industry and will further advance as one of the industry leaders in a short amount of time.

|

Company |

Ticker |

Dividend Yield |

Return on Equity |

|

PDC Energy |

2.28% |

18.66% |

|

|

ConocoPhillips |

2.11% |

27.83% |

|

|

EOG Resources |

2.69% |

20.69% |

|

|

Diamondback Energy |

2.31% |

22.40% |

|

|

Coterra Energy Inc |

2.28% |

23.31% |

|

|

Pioneer Natural Resources |

5.51% |

20.08% |

Yahoo Finance

Conclusion

I believe Petroleum Development Corporation (PDC) Energy is a great oil and gas company with huge potential for growth. Management has proved to be effective in expansionary efforts by executing well on their Oil and Gas Development Plans. In addition, with the acquisition of Great Western Petroleum now fully closed, the company will realize the great synergies and help to generate $1.7 billion in FCF for the next 2 years all while implementing repurchasing programs and raising dividends for shareholders. The results from my DCF valuation resulted in a 93.1% upside as FCF margins are likely to remain solid. Compared to other companies in the oil and gas industry, PDC Energy ranks well amongst competitors and has high rates of dividend and return on equity. The biggest risk that stands for PDC Energy is the potential of oil prices dropping due to the end of conflict between Ukraine and Russia and the success of recent monetary policy efforts by the Federal Reserve. Though again, I do not believe that this is the likeliest scenario as oil will continue to remain undersupplied and PDC Energy is well-capitalized. Overall, PDC Energy is full of bullish signals and I recommend a strong buy.

Be the first to comment