Andrii Yalanskyi/iStock via Getty Images

Summary

I still think Paycor HCM (NASDAQ:PYCR) is undervalued today. A combination of a robust economy, a growing number of available jobs, and PYCR’s dedication to ongoing product improvement provide the company with a strong growth runway. Consequently, I expect PYCR to maintain this >20% growth in recurring revenue, driven by stable employment trends and strong performance in Tier 1 regions. At 7.3x forward revenue and a slightly higher revenue base in FY23, the upside remains appealing to me.

Earnings overview

PYCR had a great 2Q23, beating expectations in terms of recurring revenue, EBIT margin, and 3Q23 guidance. Similarly to 1Q23, the majority of the increase in guidance was driven by upside to float, while recurring revenue growth remains at 22%. The strong float income is also an extra $10 million benefit embedded in FY23 guidance. The micro-environment has shown slight signs of softening, but management has seen no change in the macro-environment.

Results

With recurring revenue of $125m and Float revenue of $8m, PYCR 2Q23 revenue grew 29% to $133m, surpassing the consensus of $127m. Rising demand and increased price per active user (PEPM) were responsible for the beat. 2Q23 gross profit was $90 million, with a margin that increased by 120bps to 67.8%. Operating margin increased 330 basis points to 13.3%, which was better than consensus of 10.4%.

Operation updates

PYCR’s Talent module continues to gain popularity, with management attributing this to the module’s unique selling point. Despite the fact that the Talenya acquisition is still in beta testing, management has described the solution as using AI to simplify and streamline talent sourcing. The other good news is that PYCR is seeing continued success in the upmarket, with particularly strong results among customers with more than 500 employees. Importantly, the full list PEPM for the entire product suite now reaches $44, 11% from the previous year, which means that there is still a lot of room for ARPU to grow. This indicates that PYCR’s ARPU will continue to grow as the company’s cross-sell initiative bears fruit, it wins new customers with this newest product bundles, and a greater proportion of sales are made up of bundles.

Demand outlook

With no discernible shift in demand from previous quarters, management is maintaining its upbeat outlook on the HCM market for the 2H23. Indeed, the numbers don’t lie. Bookings hit a new high for 2Q23, and I expect PYCR to maintain its trend of bookings growth of >20% in the years to come. Overall, I think Paycor had a solid quarter and that the company has the potential to continue executing as planned in 2H23.

Guidance

For 3Q23, PYCR guided revenue between $155 and $157 million, representing growth of 26 to 28% percent year over year. Operating margin guidance of 23% at the midpoint is also 2 points above market expectations.

For FY23, PYCR is now guiding revenue between $539 and $545 million for FY23, an increase of $11 million from their previous forecast. Additionally, management increased operating income guidance by 15% at the midpoint, indicating a 14% margin, an increase of 1.5 points from the previous guide. The growth in expected interest income and PCYR ongoing ability to leverage its operations are the primary factors driving this upward revision to operating margin estimates. Furthermore, Paycor reiterated its belief that it will have a positive FCF in FY23.

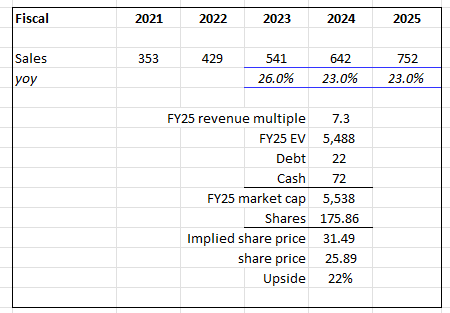

Valuation update

With the new FY23 guidance – a slightly higher base for FY24/25 – and a slightly lower multiple of 7.3x (previously 8x), I reiterate my view that PYCR upside remains attractive at 22%.

Own calculations

To monitor

It is worth keeping an eye on what is happening at the micro level since management cited softness in it. While it is not a big issue today, I am afraid it will snowball to a big one, leading to underperformance. I would size down if this happens.

On the other hand, PYCR guided FY23 float revenue of $28-30 million and an increase in the effective rate on client fund balances to 330bps. One notable omission from management’s guidance was taking into account future rate hikes. Any additional interest income would almost certainly be highly incremental to the bottom line. I would size up if rates continue to spike to higher levels.

Conclusion

In conclusion, I think PYCR is still undervalued and has a strong foundation for growth. Management maintains an upbeat outlook on the HCM market, with bookings hitting a new high in 2Q23, and I think the momentum can go on for FY23 and beyond. PYCR has guided revenue of $539 to $545 million for FY23, with an increase in operating income and positive FCF expected. Despite a slight softness in the micro-environment, the upside remains appealing at 7.3x forward revenue.

Be the first to comment