Wolterk

Paychex, Inc. (NASDAQ:PAYX) has a long history of offering top-tier payroll, human resource, and benefits outsourcing services to small and medium-sized enterprises in the U.S. It has a rising consumer base and a solid market presence. However, macroeconomic risks, notably an increased unemployment rate, might harm the company’s overall revenue. Furthermore, PAYX trades at a premium as compared to its historical performance and peers, making it an unfavorable investment at the time of writing.

Potentially A Healthy Demand Environment

Small to medium-sized businesses are generally considered to be more vulnerable during a recession due to their limited resources and financial flexibility and the decline in consumer spending, which can have a greater impact on their revenue and profitability. Despite this, according to PAYX’s survey, business leaders are optimistic about next year and anticipate substantial revenue growth. In fact, 38% of respondents expressed a desire to outsource HR activities. In my opinion, this could be more cost effective than laying off employees in order to cut costs and survive. This will help businesses to not lose valuable employees, and also save additional cost of hiring, and training new employees when the economy recovers. Overall, this could benefit PAYX in the long run, more specifically help the company to deal with the potential recession this year, and reduce risk from today’s rising unemployment rate sentiment.

On top of that, PAYX has consistently received leadership awards, as shown below, implying that its portfolio stays relevant and effective, which might be a favorable indicator for its future development.

I’m very excited about our Retention Insights offering, which continues to deliver strong results for our clients at a time when businesses remain committed to retaining their existing staff. This feature uses predictive analytics, coupled with our vast data sets, to provide insights on potential employee flight risk. Clients leveraging the Retention Insights offering are showing a 15% reduction in turnover when compared against their industry peers. We’re very pleased we received the Bronze Brandon Hall Group Excellence Award for Best Advance in HR Predictive Analytics Technology for this solution. This is the 10th consecutive year they’ve recognized us.

During the quarter, we also were recognized with the IDC 2022 SaaS Customer Service Satisfaction Award for Core HR and we are honored to have received this award as another confirmation of the power of our HR technology and the quality of our advisory services. These awards continue to validate that Paychex is a technology leader and that our focus on HR is delivering real impact for our clients and their employees. Source: Q2’23 Earnings Call Transcript

Additionally, Paychex won the 2023 BIG innovation award. With these positive catalysts, PAYX remains relevant and well-positioned to gain from the growing HCM market. In fact, it showed outstanding figures on its customer base growth which is now running around 730,000 payroll clients, up from 670,000 payroll clients in FY’19. However, when we look at its customer retention trend, we can see some disruption, as indicated in the image below, which might be an early warning of a tougher competitive environment.

PAYX: Client Retention Trend Falls for the First Time In The Last 4 Years (Source: Company Filings. Prepared by the Author)

Q2’23 Overview

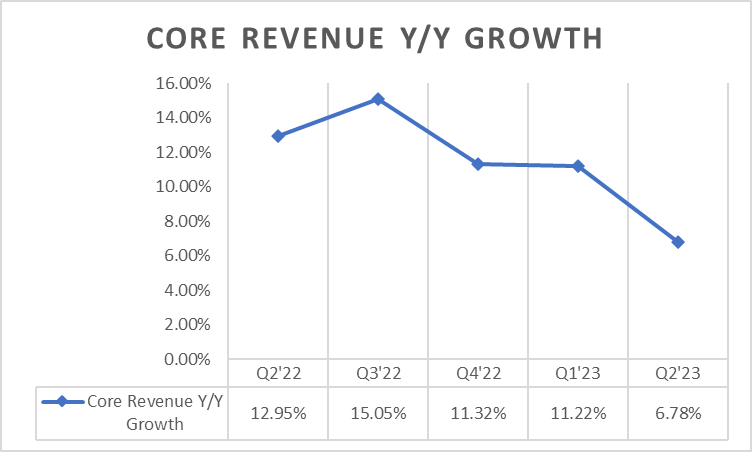

Paychex, Inc. ended the quarter with a slower growth in its core total service revenue of $1,168.6 million, as shown in the image below.

PAYX: Declining Y/Y Core Revenue Growth Trend (Source: Data from SeekingAlpha. Prepared by the Author)

Despite the previously mentioned potential of a healthy demand environment, PAYX has been regularly printing a downward growth trend, implying weakness on its profitability. This makes the company risky, especially considering the negative unemployment rate outlook.

On the other hand, the growth on both its Management solutions and PEO and Insurance Solutions has slowed compared to its respective Y/Y growth rates of 14% and 11% in Q2’22, as seen below.

Management Solutions’ revenue increased 8% to $895 million driven by higher client employment levels and revenue per client.

PEO and Insurance Solutions revenue increased 4% to $273 million, driven by growth in average worksite employees and revenue per client.

Furthermore, its outlook for Management and PEO and Insurance Solutions revenue in FY’23 is unappealing when compared to its FY’22 performance of 14% and 14%, respectively.

Management Solutions revenue expected to grow in the range of 7% to 8%. PEO and Insurance Solutions expected to grow in the range of 5% to 7%. Source: Q2’23 Earnings Call Transcript

Its non-core revenue has seen some solid growth and is benefiting today’s high interest environment, as quoted below.

Interest on funds held for clients increased 54% for the quarter to $22 million primarily due to higher average interest rates along with growth in investment balances. Source: Q2’23 Earnings Call Transcript

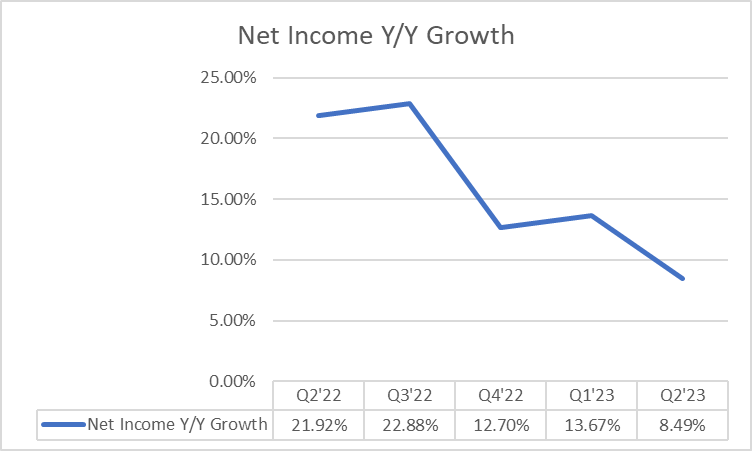

Overall, this moderation in its total revenue growth for FY’23 seems to be unattractive, especially considering the slowing net income growth, as shown in the image below.

PAYX: Slowing Net Income Y/Y Growth (Source: Data from SeekingAlpha. Prepared by the Author)

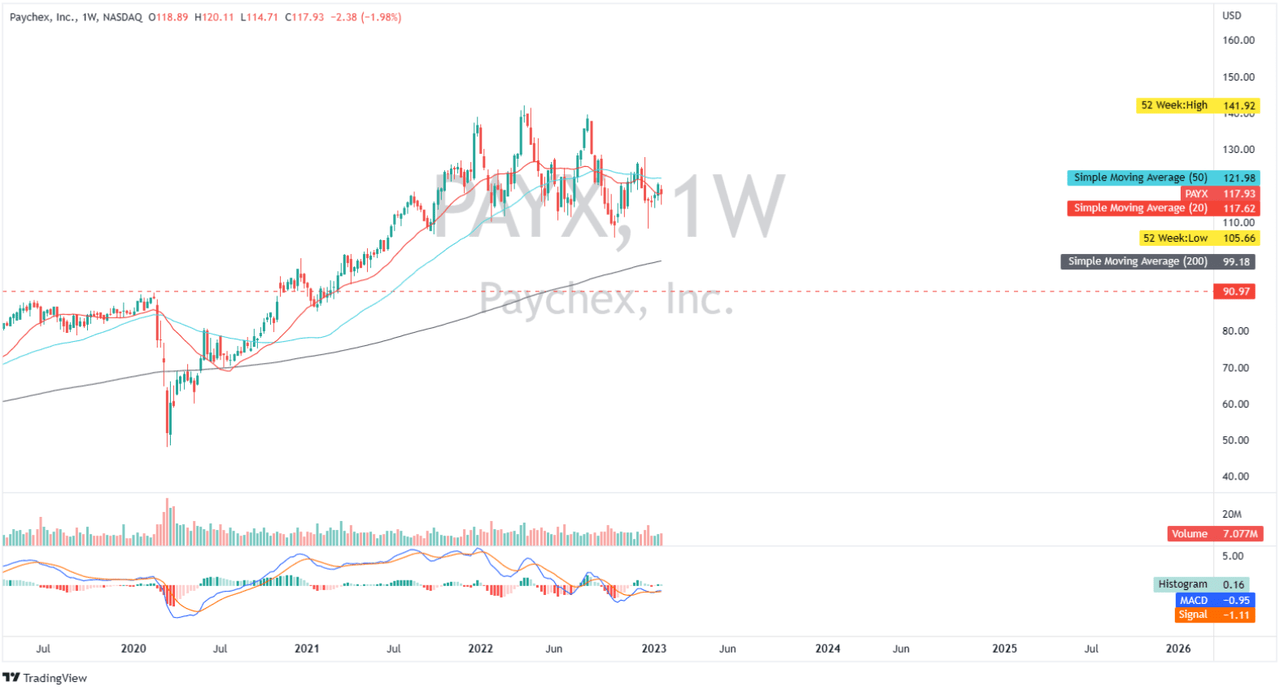

Potential Lower Swing High

PAYX: Weekly Chart (Source: Author’s TradingView Account)

The triple-top formation around the 52-week high on the chart indicates an extended period of weak price action. As of the time of writing, PAYX may retest its lower swing high at $127. This coincides with negative sentiment from its MACD indicator, which is trading below its zero line and shows potential negative catalyst with the possible bearish crossover from the Signal line. If negative pressure persists, I believe the $90 to $100 support level would serve as a strong support to monitor.

A Bit Expensive

PAYX: Relative Valuation (Source: Data from SeekingAlpha. Prepared by the Author)

PAYX trades at a slight discount when compared to its peers – Automatic Data Processing, Inc. (ADP) and H&R Block, Inc. (HRB) – based on its forward P/E ratio (27.59x compared to the peer average of 30.82x). However, when looking at the forward EV/EBITDA ratio (18.93x compared to the peer average of 17.13x), Paychex appears to trade at a premium, as of this writing. When compared to its historical performance, PAYX trades somewhat lower than its 5-year P/E average of 29.41x and slightly higher than its 5-year EV/EBITDA average of 8.22x. In considering the possibility of a recession, this makes PAYX an unappealing investment.

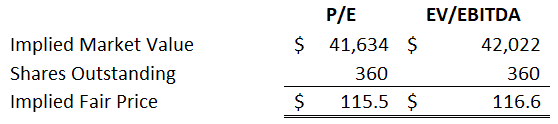

PAYX: Relative Valuation (Source: Prepared by the Author)

Based on the information provided, using an implied P/E ratio of 30.82x, an EV/EBITDA ratio of 19.64x, the estimated EPS of $4.24, the EBITDA amounting to $2,224.88 million in FY’23 and applying a 10% discount, the average fair price for PAYX would be $116. As a result, it offers no margin of safety, making it an unappealing buy candidate.

Final Key Takeaways

Paychex, Inc. remains liquid with $1,262.1 million in cash and cash equivalent in the balance sheet and a declining total debt amounting to $874.8 million as of this writing. It recorded an improving debt to equity ratio of 0.27x better than its 0.31x.

Despite the moderating growth mentioned earlier, Paychex has a strong and diverse product portfolio that will be well-suited to taking advantage of market growth when it recovers. However, at this point in time, I believe that waiting for a significant pullback in Paychex, Inc. would create a higher reward potential and, in fact, raise its present dividend yield of 2.68%.

Thank you for reading and good luck!

Be the first to comment