D-Keine

Introduction

I like to write about companies that lack coverage on SA and today I’m taking a look at Park Lawn Corporation (TSX:PLC:CA). This is Canada’s largest publicly traded death care company and while it might look expensive at almost 30x price to TTM earnings, I think that it has a bright future. Park Lawn has been growing rapidly over the past years and it aims to reach $150 million adjusted EBITDA and EPS of $2.00 by 2026. In my view, this goal is achievable. Let’s review.

Overview of the business and financials

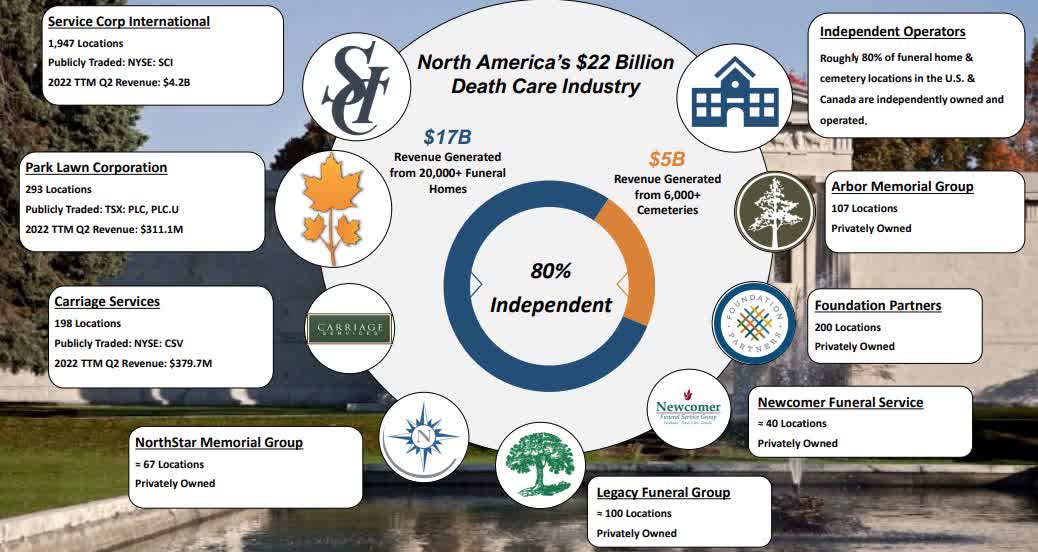

Park Lawn was founded in 1892 and is involved in the operation of cemeteries, crematoriums, and funeral homes across Canada, and the USA. About 90% of its net sales come from the USA. The death care market in the region is worth about $22 billion but is highly fragmented as about 20,000 independent funeral homes account for some 80% of revenues.

Park Lawn

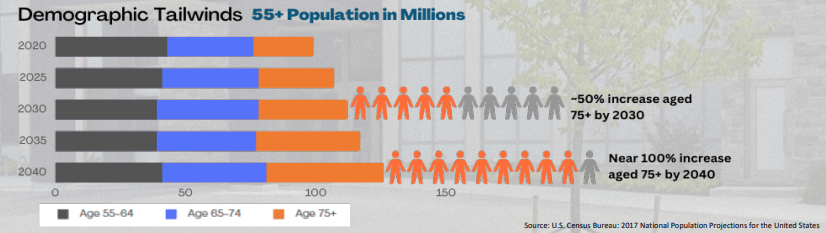

The industry has high fixed costs and it’s growing at a moderate pace considering the US has an aging population.

Park Lawn

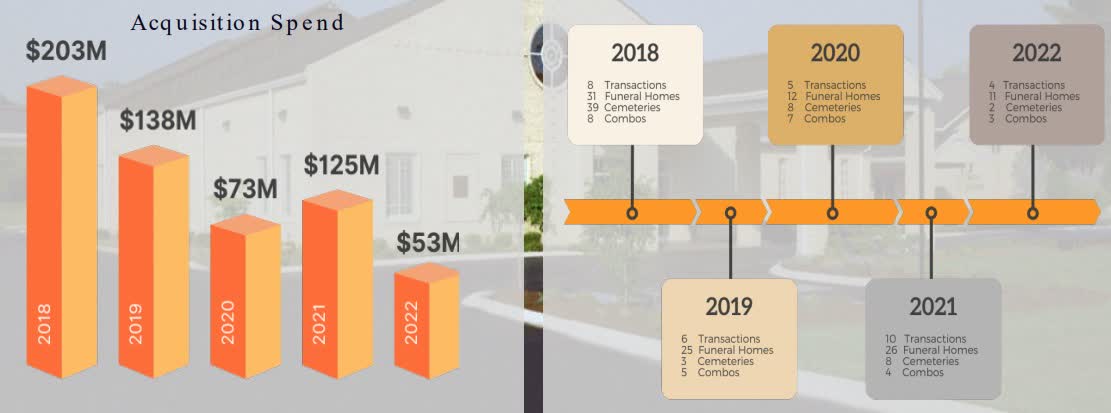

In my view, this market is ripe for consolidation, and this is exactly what Park Lawn has been focused on over the last few years. Back in 2017, the company had a network of 28 funeral homes and 53 cemeteries across Canada and the USA. Today, it has 300 locations across 3 Canadian provinces and 17 U.S. states. Since 2018, Park Lawn has made between 4 and 10 acquisitions every year, investing over $200 million in M&A across a single year on one occasion. Overall, its strategy is to invest an average of $75 million to $125 million in acquisitions per year.

Park Lawn

This acquisition spree has enabled the company to increase its footprint from about 700 employees and 13,000 families served in 2017 to around 2,500 employees and 58,000 families served today.

Turning our attention to the financial results of Park Lawn, we can see that annual revenues grew from $13.2 million in 2012 (when the company had just 6 locations in Toronto) to $280 million for the last 12 months. Unfortunately, it appears that no economies of scale exist as the operating income margin has slumped from 21.97% in 2013 to 14.43% for the last 12 months. Yet, the profitability of Park Lawn has improved at a rapid pace in absolute terms as the TTM operating income is above $40 million.

Seeking Alpha

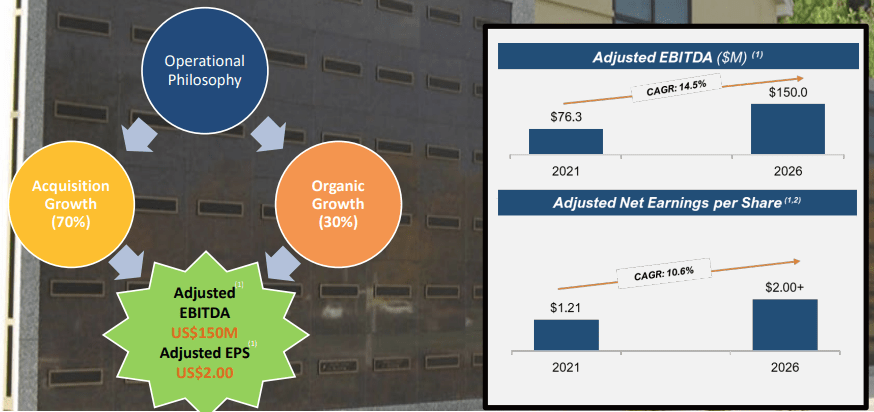

Looking at what to expect for the future, Park Lawn plans to continue to grow mainly through M&A over the coming years and it has set an ambitious target of reaching annual adjusted EBITDA of $150 million and EPS of $2.00 by 2026. Only around 30% of the company’s growth is expected to come from organic growth thanks to tailwinds such as the aging U.S. population.

Park Lawn

In my view, these targets are achievable considering the operating income has tripled since the end of 2018. Admittedly, revenue growth has been limited since 2021 but this is because the whole death care market received a significant boost during the COVID-19 pandemic as a result of higher death rates. The company said during its Q3 2022 earnings call that the 10.7% revenue growth during the period exceeded its expectations considering the decline in the death rate. Unfortunately, adjusted EBITDA was flat as the company felt the pressure from inflation as operating costs such as labor, utilities, fuel, and maintenance increased significantly.

Park Lawn

In my view, Park Lawn’s revenue growth is likely to return to above 20% in the near future as the death rate in the USA returns to normal. The company has also been busy on the M&A front over the past few months as its Q3 2022 financial report revealed that it inked agreement for four acquisitions between October 1 and November 9 alone (see page 48 here).

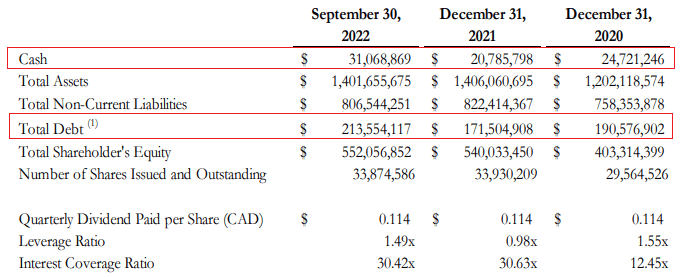

Turning our attention to the balance sheet, I think that the situation looks good considering Park Lawn has carried out 14 acquisitions since the end of 2020. The net debt stood at $182.5 million as of September 2022, compared to $165.9 million in December 2020 and I think this level is manageable. As of September 2022, the leverage ratio was 1.49x while the interest coverage ratio stood at above 30x.

Park Lawn

Park Lawn currently has a quarterly dividend of C$0.114 (0.085) per share, which translates into an annual dividend yield of 1.65%. I don’t expect the size of the dividend to be increased anytime soon as the company will need a significant portion of the free cash flow to fund acquisitions over the coming years.

Overall, I think that Park Lawn can return to exponential growth in the near future and that its goal of reaching $150 million adjusted EBITDA and EPS of $2.00 by 2026 seems achievable. The company is trading at 29.94x price to TTM earnings as of the time of writing but this could drop below 10x in about 4 years if the market valuation remains unchanged. Since 2018, Park Lawn has achieved a 33% adjusted EBITDA CAGR and a 16% adjusted EPS CAGR.

Looking at the risks for the bull case, I think that there are two major ones. First, rising interest rates could make it challenging for Park Lawn to secure funding for its acquisitions, which could lead to a slowdown of its revenue growth rate. Second, the daily trading volume rarely exceeds 50,000 shares which means that there could be significant share price volatility. In my view, it could be dangerous to start a large position as it would be challenging to exit without putting pressure on the share price.

Investor takeaway

Park Lawn looks expensive based on fundamentals at first glance, but the company has an excellent track record of growing revenues and net income over the past decade, and I think that it’s likely to achieve its goal of reaching EPS of $2.00 by 2026. The balance sheet is strong, and I think Park Lawn should be able to finance its M&A strategy without a hitch. The share price has tripled since 2013 and I think there is good upside potential here as revenue growth rates return to above 20% in the near future. However, it seems dangerous to open a large position due to the low trading volume.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment