Elisabetta Villa/Getty Images Entertainment

As with others in the video streaming sector, Paramount Global (NASDAQ:PARA) has been crushed this year. The company has several hit shows now, but the DTC service is getting further away from profits due to higher content costs just as the business is maturing. My investment thesis is Neutral on the stock until the media business becomes far less competitive while only attracting low priced subscribers.

No King Here

While the Tulsa King series starring Sylvester Stallone has been a success, Paramount is not close to the king of video streaming. The current Paramount+ offer highlights the problem the service is having with becoming profitable.

Source: Paramount+

Paramount+ offers a free 7 day trial where viewers can cancel anytime. After that, a viewer has to choose a subscription costing $4.99 per month with limited ads or the Premium service at $9.99 per month with no ads and additional features. The service even offers annual billing that reduces the monthly cost to $4.17 for Essential and just $8.33 for Premium.

The DTC business now has an incredible 67 million global subscribers with Paramount+ having 46 million subs. Though, the problem is that the streaming service is now losing $343 million a quarter, up from $198 million last Q3.

Source: Paramount Q3’22 earnings release

Revenues are growing at a fast clip, but Paramount isn’t even covering the 44% boost in expenses. New series like Tulsa King and spinoffs from the very successful Yellowstone come at huge additional costs that free trails and only $5 a month don’t cover.

Disney (DIS) rehired Bob Iger in part to restructure the DTC business. The market is starting to realize the sector is overly competitive with consumers having at least 6 or 7 strong options for subscriptions. In addition, the services offer too many options for free trials and the easy ability to cancel reducing the possibility of hitting the massive subscriber predictions at launch.

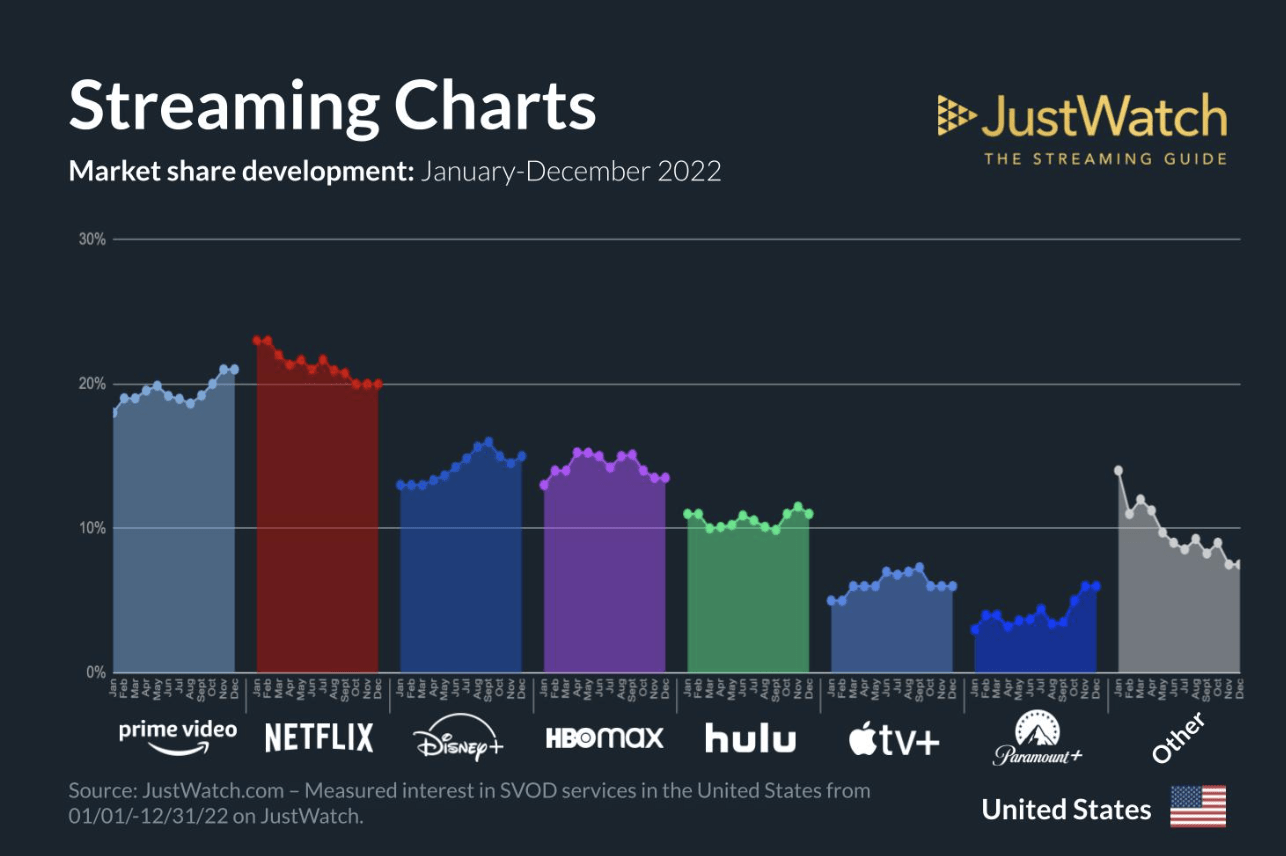

According to JustWatch, Amazon Prime (AMZN) has a surprising market share lead over Netflix (NFLX) with both streaming services having ~20% of the market. Both Disney+ and HBO Max (WBD) are struggling with only 15% of the market questioning how much success Paramount+ can achieve at only 6% of the market.

Source: JustWatch

The combination of a service with large, and growing, losses along with a market share position competing with a tech giant like Apple (AAPL) with unlimited funds isn’t ideal. According to Wells Fargo, Apple has no plans to slowdown content spending and recently bid aggressively against YouTube (GOOG) for the NFL Sunday Ticket to further expand spending from $8+ billion annually.

Wait For The Turn

While linear TV is still poised to lose more viewers to video streaming services, Paramount has a TV Media business producing $5.0 billion in quarterly revenues in comparison to just $1.2 billion in DTC. Loup Capital sees continuing weakness in linear TV causing problems for the media company leading to reduced cash flows in 2023.

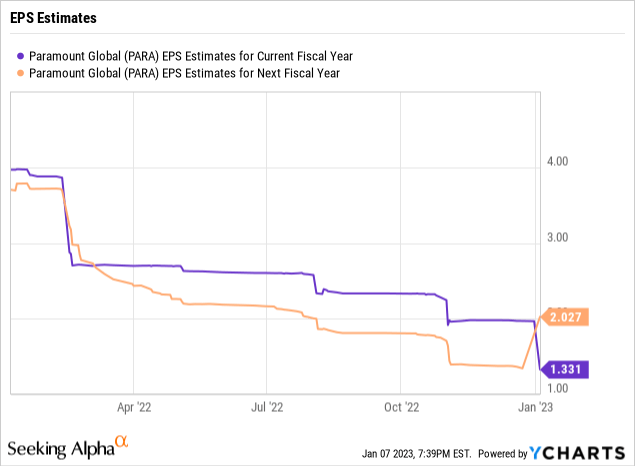

Analysts now forecast EPS estimates collapsing next year to only $1.33 per share from an estimate of $1.97 in 2022. Paramount will face a difficult time turning around the business with the tech giants like Amazon, Apple and now Google spending aggressively on media content along with near unlimited budgets due to impressive cash flows from their primary business units.

The consensus estimates forecast an EPS rebound for Paramount in 2024, but investors shouldn’t invest in the stock at $20 assuming such a scenario occurs. The business needs to hit rock bottom before a turn will ever occur and investors should wait for this bottoming process to even start before thinking about starting a position. After all, the consensus estimates were originally forecasting a rebound in 2023 and now the expectation is for a large dip.

Paramount isn’t necessarily expensive at ~10x the 2022 estimates and the 2024 forecasts for a rebound, but investors need to be careful assuming this rebound occurs. The large tech giants could make life very difficult for the media company with a net debt balance topping $12 billion. Paramount doesn’t have the financial firepower to match a Amazon or Apple.

Takeaway

The key investor takeaway is that Paramount is a value trap here until the competitive position changes in the video streaming space. Hope is not a good investment thesis.

Be the first to comment