Just_Super

Thesis

At FWD x5.9 EV/Sales and x30 EV/EBIT, Palo Alto Networks (NASDAQ:PANW) is trading too expensive to warrant an investment, in my opinion. Although I acknowledge that the company is likely to benefit from a strong growth tailwind in the demand for cybersecurity solutions, Palo Alto must deliver on very optimistic assumptions to justify a $40 billion enterprise value. In addition, I am concerned about Palo Alto’s cost structure, which discloses more than $1 billion of share-based compensation per year.

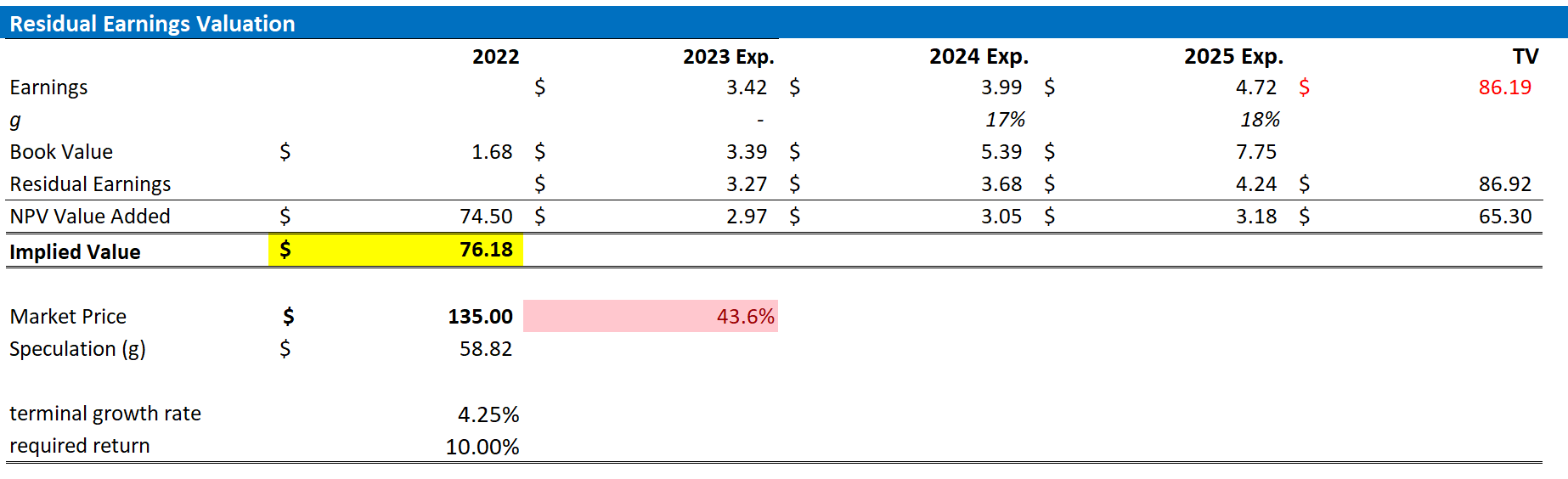

Personally, I value PANW stock with a residual earnings model and calculate a fair implied share price of $76.18. Accordingly, as a function of valuation concerns, I initiate coverage with a ‘Sell’ recommendation.

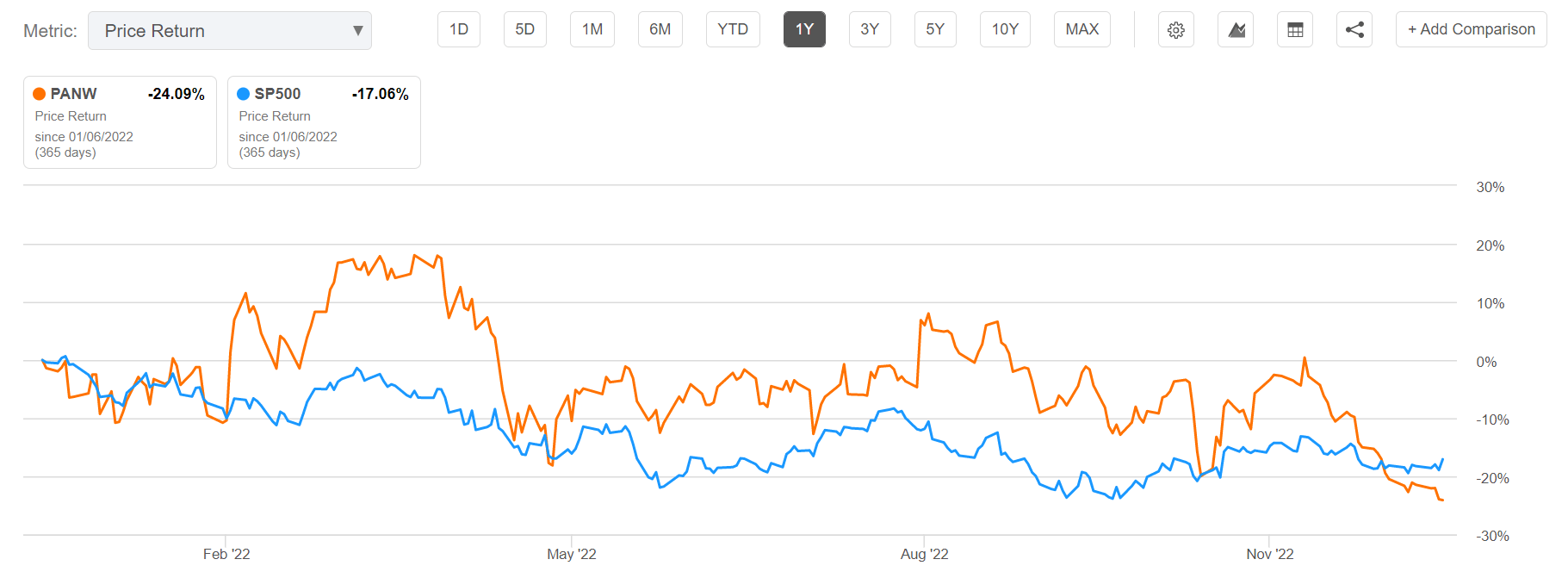

For reference, PANW stock is down approximately 24% for the past twelve months, as compared to a loss of about 17% for the S&P 500 (SPY).

Seeking Alpha

About Palo Alto Networks

Palo Alto is a leading provider of cybersecurity solutions. The company’s value proposition is designed to detect and prevent both known and unknown threats, as well as to provide visibility and control over network activity. In that context, Palo Alto offers products related to firewalls, intrusion prevention systems, and endpoint protection software.

PANW Q3 2022 results

As of Q3 2022, Palo Alto served 1262 ‘millionaire customers’, which the company defines as clients that have spent more than $1 million of booking value on Palo Alto’s products and services within the last 4 quarters. The company closed the quarter with $5.8 billion of TTM revenues.

Palo Alto Networks was founded in 2005 and is headquartered in Santa Clara, California. The company has offices in over 50 countries around the world.

The Cybersecurity Market

The cybersecurity market is expected to be at a significant rate in the coming years due to increasing threats from cyberattacks, data breaches, and other forms of cybercrime. Arguably, the growth is being driven by the rapid adoption of new technologies such as cloud computing, the Internet of Things, and 5G networks, which are creating new vulnerabilities that need to be protected. This trend is likely to continue in the post-pandemic world, as more organizations adopt hybrid work models and look to take advantage of the scalability, flexibility, and cost savings of cloud computing.

Another key driver of demand for PANW’s solutions is the increasing complexity of the threat landscape. Cyber threats are becoming more sophisticated, and attackers are using a wider range of tactics, techniques, and procedures (TTPs) to breach organizations’ defenses. PANW’s solutions are designed to fight these threats through the usage of, amongst others, artificial intelligence and machine learning to analyze network activity and identify anomalies that may indicate an attempted breach.

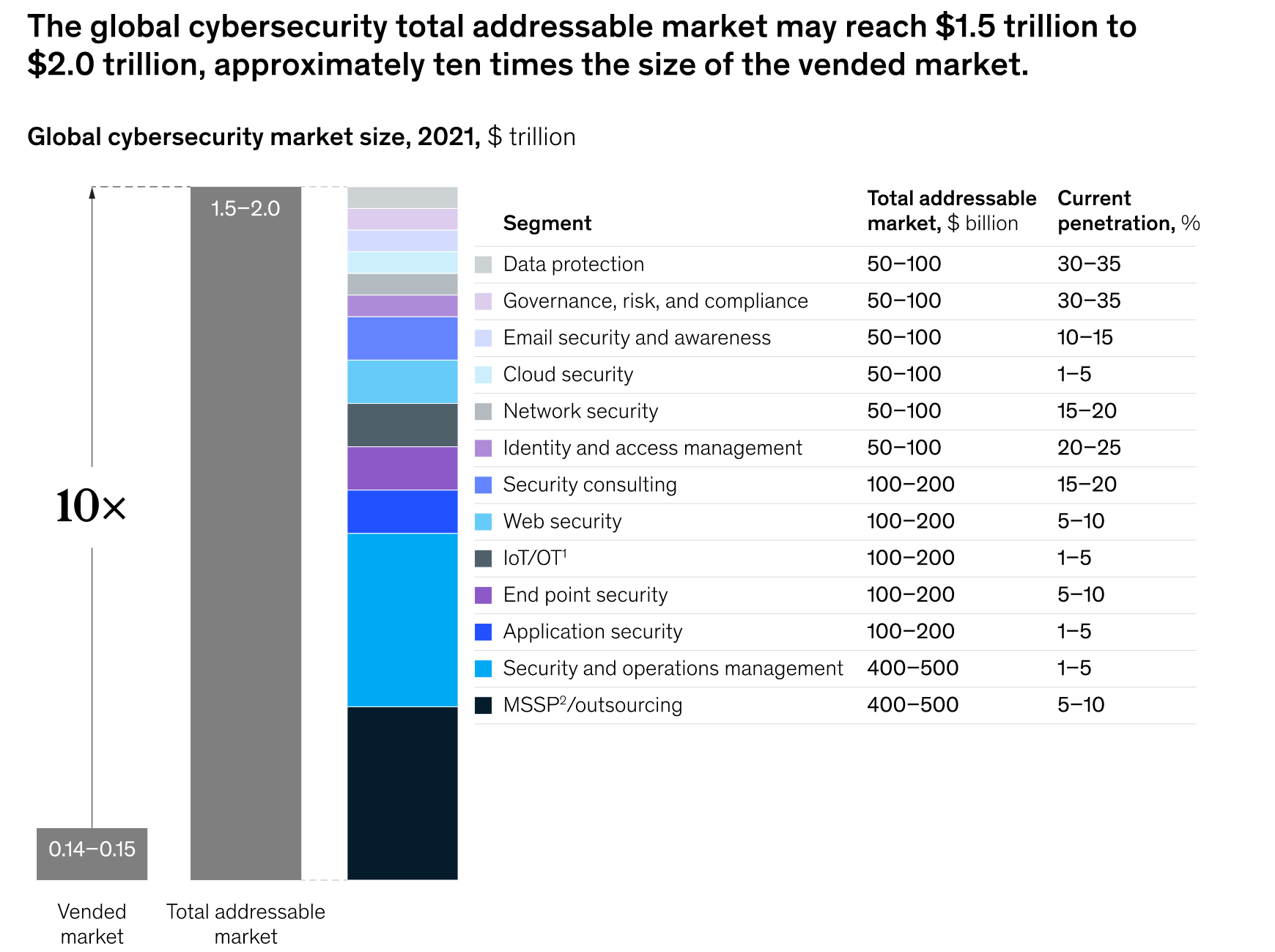

For reference, McKinsey has estimated that the annual dollar-denominated damage caused by cyberattacks could be as high as $10 trillion. In addition, through a survey of 4000 mid-size companies, McKinsey suggested that the global total addressable market for cybersecurity could be between $1.5 and $2 trillion, which is approximately 10 times the size of the current vended market.

McKinsey

However, reflecting on the potential market size, investors should consider that the market is highly competitive – with CrowdStrike (CRWD), Cisco Systems (CSCO), Fortinet (FTNT), SentinelOne (S), McAfee and more all competing for a similar customer profile.

In the context of competition, it is also worth noting that the cybersecurity industry is subject to rapid technological change, and PANW may face challenges in keeping up with new developments and maintaining its competitive edge. This could impact the company’s ability to attract and retain customers, and could also impact its financial performance.

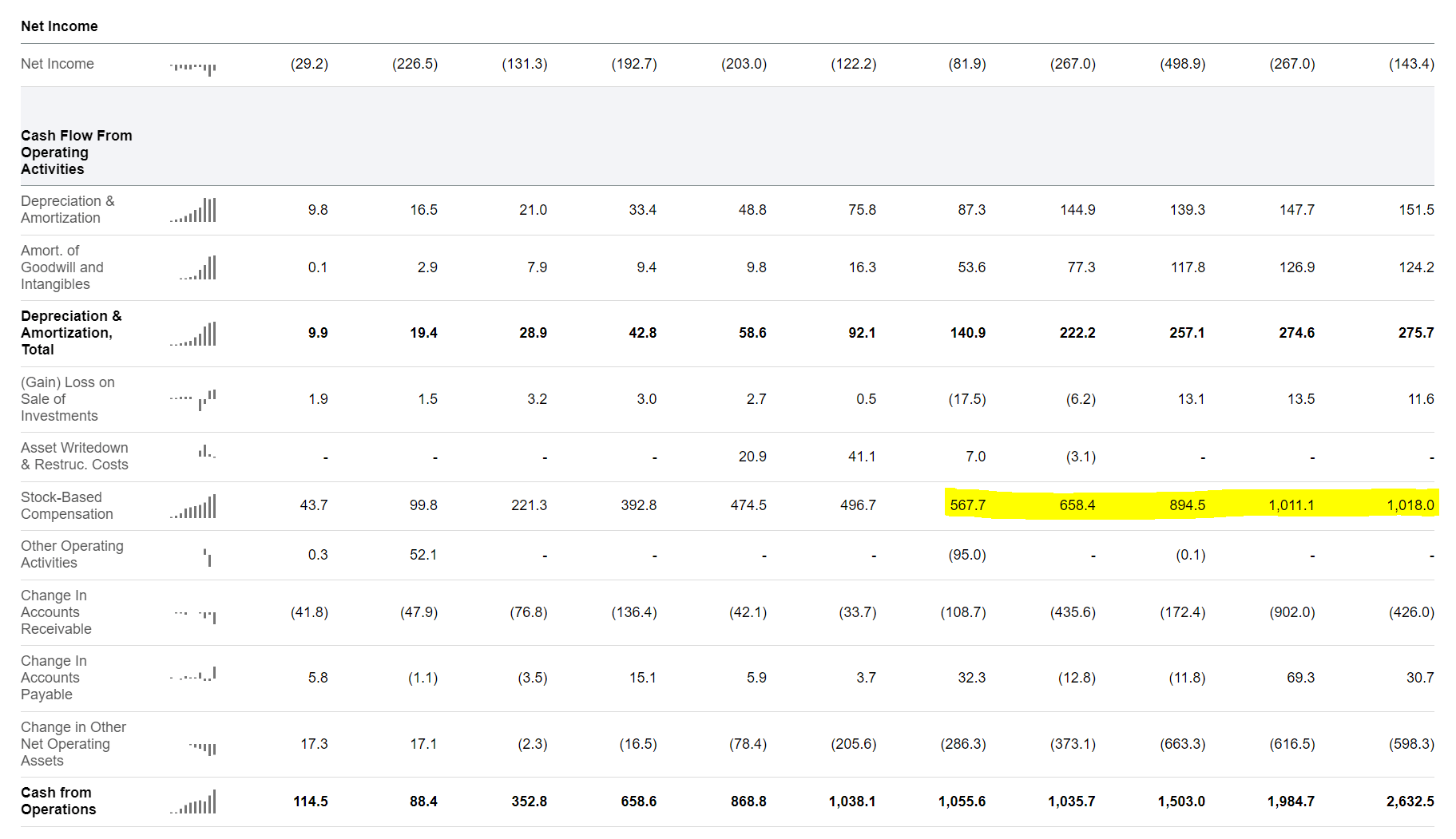

PANW Is Not Yet Profitable

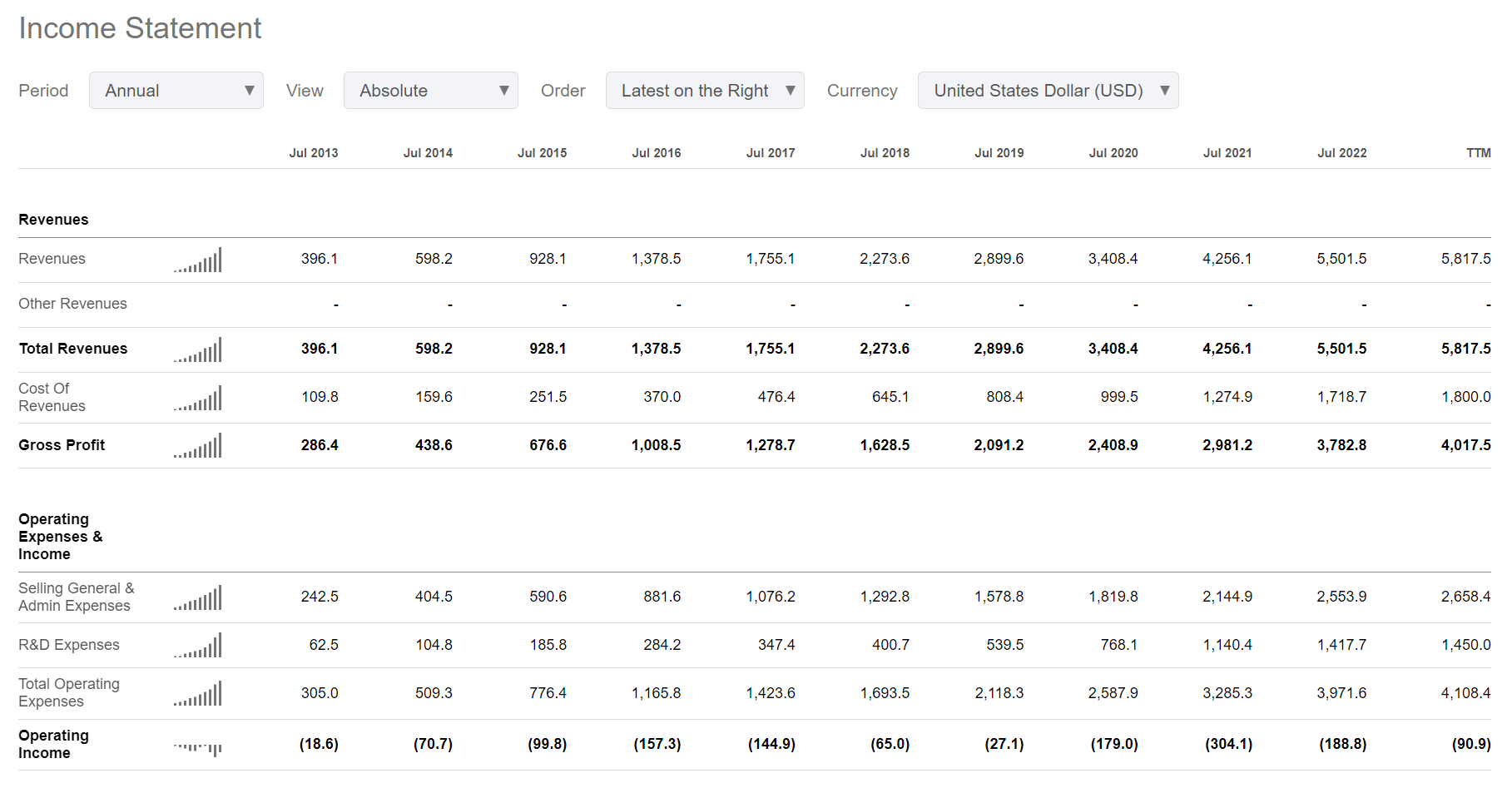

Although it has been argued by some analysts (for example see here) that Palo Alto is profitable, my analysis disagrees with the statement. In fact, quickly analysing PANW’s income statement, I note that the company reported negative operating income throughout the last decade. And for the trailing twelve months, the operating loss was $91 million.

Seeking Alpha

The confusion regarding profitability may be anchored on the fact that Palo Alto adjusts its Non-GAAP income for stock-based compensation, an expense bucket that accounted for as much as $1.02 billion for the trailing twelve months. However, share-based compensation is a very real expense and investors are well advised to include this expense in their profitability calculation.

Seeking Alpha

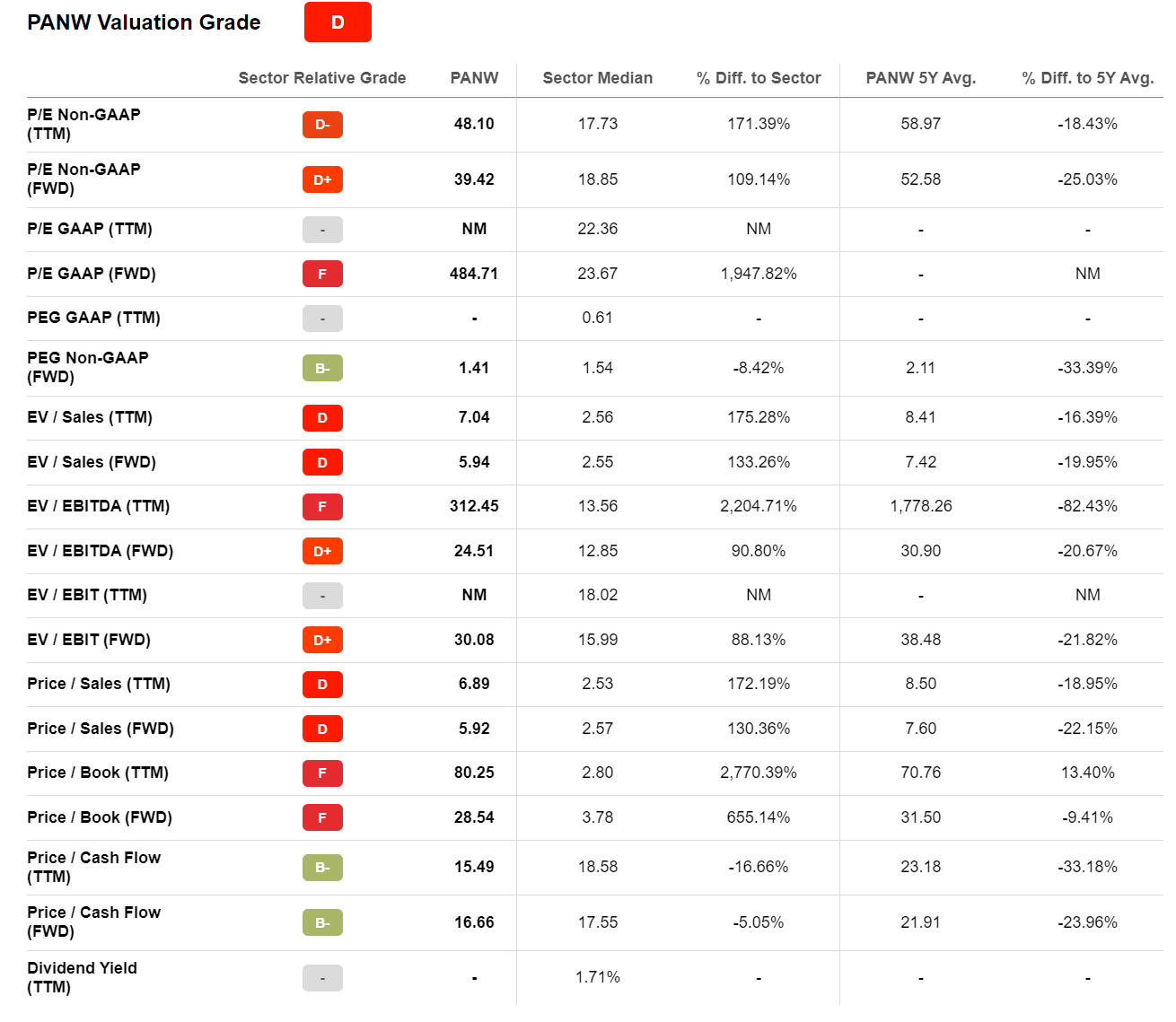

Valuation Simply Too Expensive

Although I acknowledge the secular tailwind coming from an accelerating demand for cybersecurity software, at FWD x5.9 EV/Sales and x30 EV/EBIT, Palo Alto Networks is trading too expensive to warrant an investment, in my opinion. (I would accept such a multiple, a 133% premium to the sector median, for a very young growth company. But not for an industry leader with more than $5 billion of revenues already).

Seeking Alpha

Residual Earnings Model

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my PANW stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor PANW’s cost of equity at 10%.

- For the terminal growth rate after 2025, I apply a proud 4.5%, which is approximately double the estimated long-term nominal GDP growth (to reflect a strong growth tailwind until at least 2030).

Given these assumptions, I calculate a base-case target price for PANW of about $76.18/share, which implies that PANW could be overvalued by as much as 43.6%.

Analyst Consensus EPS; Author’s Calculation

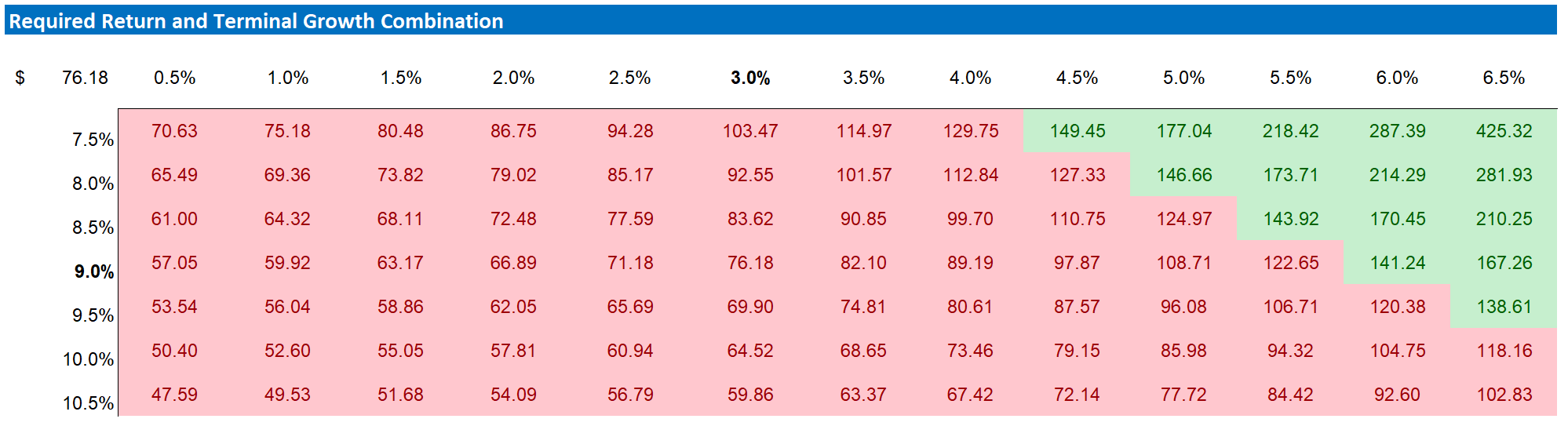

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of PANW’s cost of equity and terminal growth rate, I have constructed a sensitivity table. Note that the matrix looks very favorable from a risk/reward perspective.

Analyst Consensus EPS; Author’s Calculation

Upside Catalysts

Given the speculative nature of ‘short selling’, I do not recommend betting against PANW – despite the considerable valuation premium. And in any case, an investor could consider that the long-term demand for cybersecurity solutions could offer enough of a tailwind to justify investing in PANW even though the company’s valuation is arguably out of touch with fundamentals.

Moreover, investors could consider that industry consolidation – Palo Alto merging with or acquiring competitors – could support increased pricing power and profitability.

Conclusion

Although I acknowledge strong secular growth tailwinds for cybersecurity companies, at FWD x5.9 EV/Sales PANW stock is trading too expensive to warrant an investment, in my opinion. Personally, I value PANW stock based on a residual earnings model anchored on analyst consensus EPS and a 10% cost of capital. My calculation indicates that the fair value for PANW stock is likely somewhere around $76.18/share.

Be the first to comment