Andreas Rentz

Investment Thesis

Palantir Technologies (NYSE:PLTR) reported Q4 earnings that took investors by surprise. A positive surprise that PLTR’s guidance for the year ahead will end with positive GAAP income.

That being said, PLTR’s pace of growth has subdued. But given that the stock has largely been a disappointment to anyone that’s held it for the past year, anything that wasn’t bad news was always going to be taken as good news.

Palantir’s Prospects

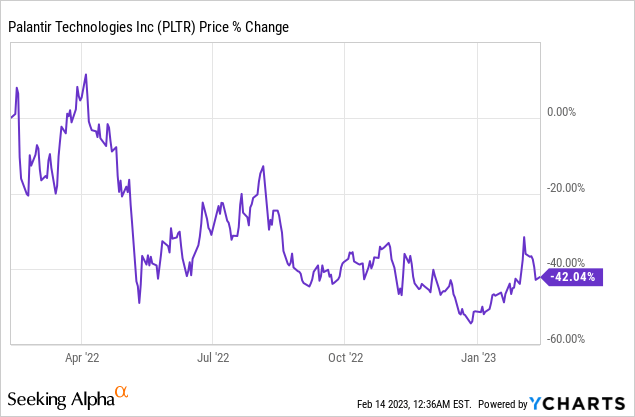

Palantir was amongst the bubble stocks that first started selling off two years ago.

The implosion in this group of stocks was quick at first. But now PLTR stock had time to re-steady its footing and a lot of the glamor of Palantir has gone the risk-reward is slightly more attractive.

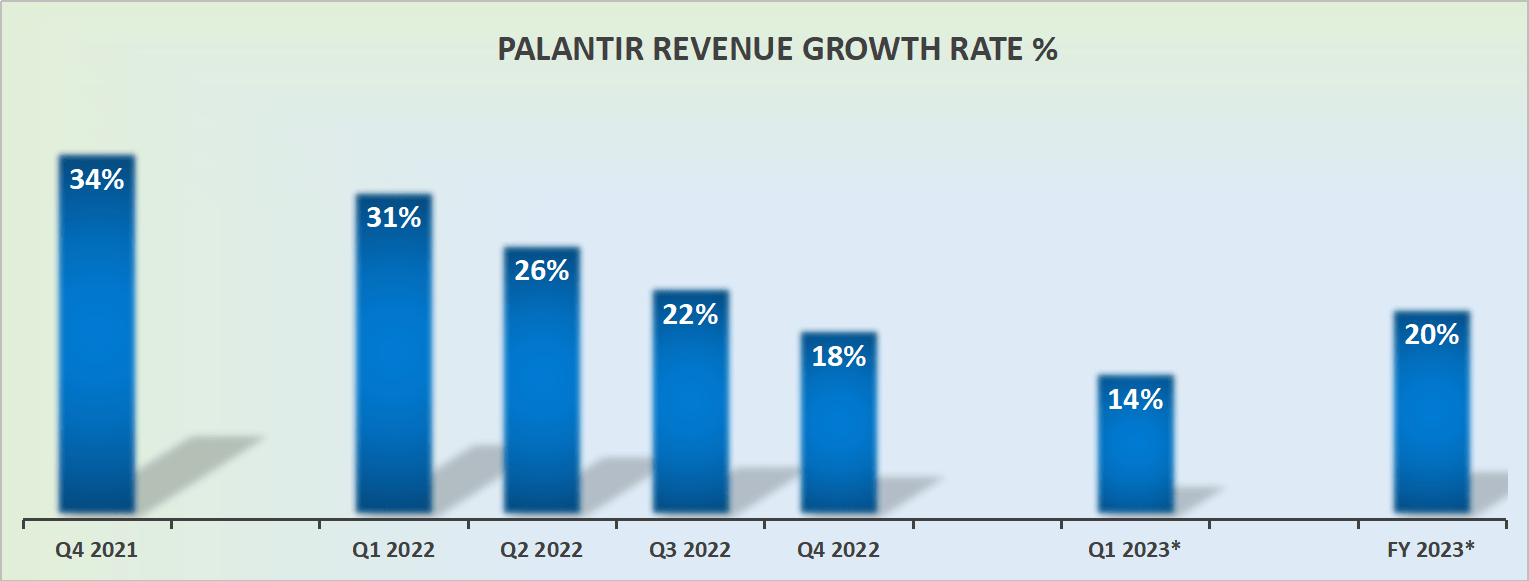

Revenue Growth Rates Expected to Slow

PLTR revenue growth rates

PLTR’s growth rates for the year ahead point to 20% CAGR. Even if the macro environment appears to be highly conducive toward PLTR’s prospects gaining significant traction, this guidance does not appear to back that thesis.

Furthermore, PLTR does not have a history of dramatically lowballing its guidance to allow for strong beats further into the year. Thus, I’m inclined to believe that what we see is here largely what we’ll get from PLTR.

Moving on, when discussing Palantir’s results on the earnings call PLTR’s CEO said,

The weakness in our business is just non-U.S. commercial that grew around 12% last year. I think outside the U.S., they’re a lot less friendly to new innovations. It’s not clear how they’ll react to AI, although we can do AI in the context of data protection.

In the past several weeks Wall Street has been taken by AI technology. Any company with AI technology has seen its multiples rerate higher.

Consequently, PLTR has now also made some mentions of its AI technology on its earnings call. For some investors, this could be something attractive, particularly in the context that PLTR is now expected to be GAAP profitable.

Profits Are Set to Improve

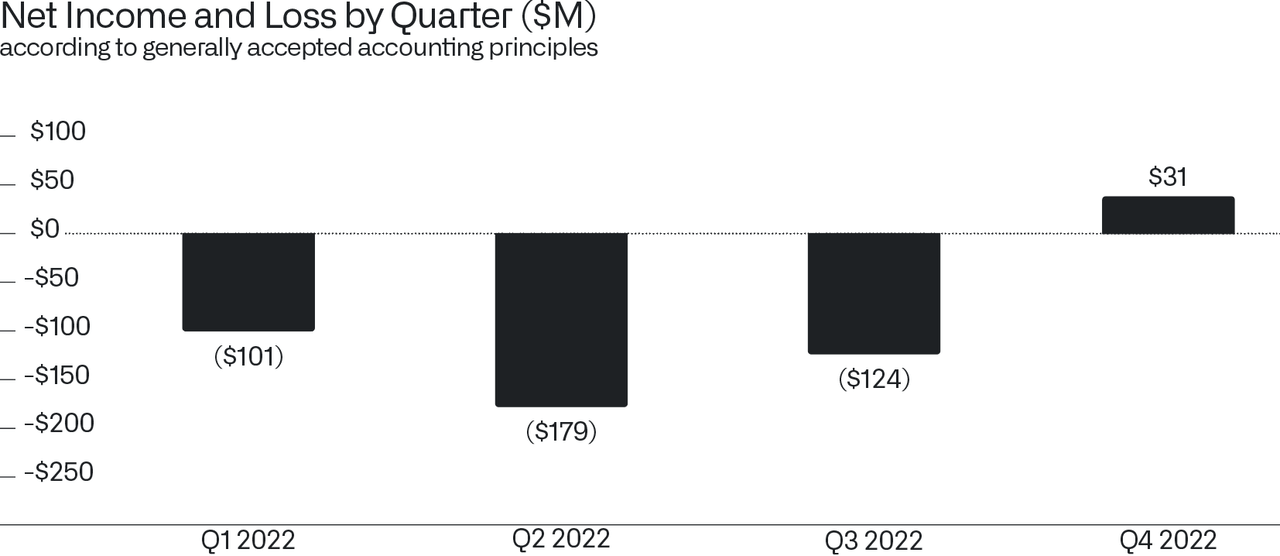

Palantir’s GAAP profitability this quarter did not come from its operations.

Even though Palantir displays this image and explains how this marks the company’s first GAAP profit.

PLTR Q4 2022

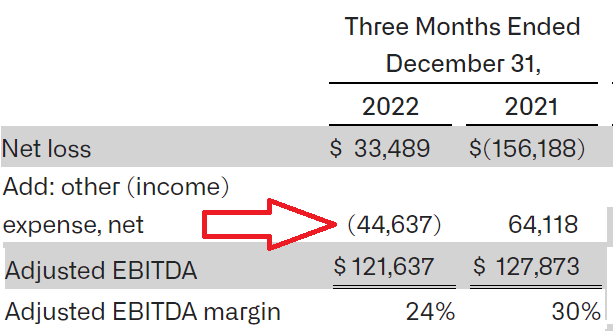

In fact, $45 million out of the $31 million GAAP profit came from the outside normal course of business, which Palantir calls other income.

That being said, to be clear, this figure is normalized on PLTR’s adjusted EBITDA line.

PLTR Q4 2022

And what we see here is PLTR’s adjusted EBITDA line does not appear to be growing alongside its revenues. In fact, PLTR’s EBITDA margins compressed 600 basis points y/y.

On the other hand, looking ahead to 2023, PLTR’s guidance points to an adjusted operating income margin figure of 23% at the midpoint, which is a slight improvement from the 22% it reported for 2022.

In sum, it’s not so much that Palantir’s profitability profile is set to be all that impressive. It’s more the case that Palantir has now reached a point in its operations where more of its topline revenues can percolate through to its bottom line.

Put simply, there starts to be some operating leverage with Palantir’s business.

PLTR Stock Valuation — 36x Forward Operating Income

Palantir typically offers its management approximately $500 million worth of stock-based compensation.

Given that the midpoint of its guidance points to just slightly over $500 million of adjusted operating income, this means that for the year ahead, it doesn’t appear to be the case that PLTR’s stock-based compensation will increase further.

Consequently, this appears to infer that Palantir’s management is now more aligned with its shareholders. And unless PLTR can increase the intrinsic value of the company and together rise its share price, its stock-based compensation will not be as attractive as it could be.

In sum, PLTR is being priced at 36x forward adjusted non-GAAP operating income. A figure that on the surface does not strike me as particularly cheap.

The Bottom Line

PLTR’s CEO Alex Karp stated on the call,

And while many of us watching this are obviously highly attenuate to share price, the people whose lives depend on our product have been very dependent on us and want to know that our financial stability now and in the future is guaranteed.

So this has been much more of a priority to get us to this place.

Essentially echoing what many of its shareholders want to hear. Investors believe in PLTR’s mission. And now that the business is going to be GAAP profitable and financially stable, investors feel more compelled to invest in the company.

However, for me, this stock remains too richly priced. Whatever you decide, all the best.

Be the first to comment