imagedepotpro

Data is analyzed and can become information. Information is power, especially in the current world. Artificial Intelligence, or AI, is built on highly complex data systems and algorithms. Well, data systems, analysis, information, and algorithms are exactly what Palantir Technologies Inc. (NYSE:PLTR) does as a business. It is in the business of data, of information, and intelligence. And folks, this a battleground stock.

We still view Palantir as a long-term investment despite having initiated a number of trades in the name in the last two years. While we have concerns with shareholders being diluted, we still believe PLTR stock will provide returns from the single-digit levels. We also believe that the AI craze that seemingly has exploded onto the scene in recent months is actually something Palantir will excel in. We follow the company closely. The company just reported Q4 earnings, and while we see Palantir being an AI winner, the company was profitable in the quarter, and is forecasting more profits. In this column, we discuss Palantir’s Q4 performance, and discuss the forward view that was provided by management.

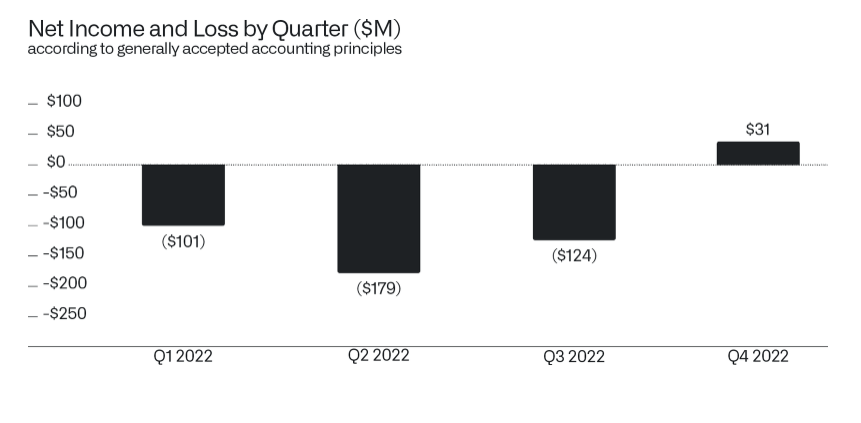

Swinging to profit

Palantir Technologies Inc. has long been a high revenue growth, innovative tech stock that loses money. It has flirted with breakeven and a few quarters of positive net income, but now it seems the company may be able to sustain profit. We have had concern over profit on a per share basis, given the massive dilution problem, which means consistent positive EPS gets kicked further down the road. And when the company is growing net income, EPS growth can be muted if we have more shares available.

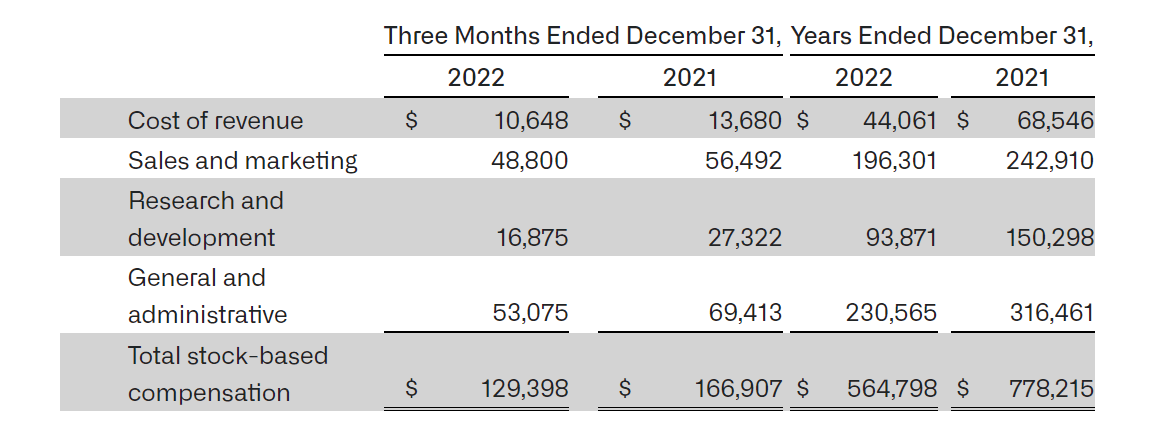

However, stock-based compensation (“SBC”) is recognized as an issue that management wants to address, though it is a strong way to attract talent in the tech sector. So, a bit of a catch-22, if you will. That said, Palantir Technologies Inc. did issue a lot of shares once again:

Palantir Q1 Release

The ongoing stock-based compensation makes increasing EPS more difficult. However, as you can see, the company slowed its compensation in Q4 versus a year ago, and also slowed in 2022 versus 2021.

What about AI?

We have argued many times that the company uses complex algorithmic data analysis to translate pieces of data into information, and to be predictive and to help with decision-making. Folks, that is AI at its heart. On the conference call, AI was cited a number of times by CEO Alex Karp.

In regards to Gotham:

Gotham is today the AI-driven operating system for defense. Recent events have already proven the superiority of Gotham and AI-driven target detection and development. In 2023, we are focused on the continued development of Gotham against both targeting and fires across all domains from space to mud.

In regards to war and decision-making, Palantir’s software has helped with decision-making:

In the war context, how do you know if the AI made the decision? Under what conditions does AI make the decision? Under who is responsible? What is the chain of authority? How do you do it while maintaining security, because some of the people using the product may actually be working for the other side?

There’s just thousands and thousands of issues here that required years and years of software build, which we are now going to continue to supply to our allies across the world and to our consumer customers.

And in regards to weapon systems data:

This is a world that is dangerous that needs AI-driven and, in general, software-driven weaponry. And no other company in the world has been focused on this for the last 20 years than we are. And we are also on these programs.

The point? Palantir is a real AI company, in that its software to help decision-making is at its core, intelligence in the artificial sense.

So, strides are being made. Now what about sales?

Palantir’s commercial segment strong

In Q4, performance was strong on the top line and the revenues were ahead of consensus estimates. Total revenue grew 17.5% year-over-year to $508 million, beating estimates by $3.6 million. However, its profitability was also a beat, coming in at $0.04 per share, better than expected by $0.01. It was a profitable quarter, and the first in the company’s history:

Palantir Q4 investor letter

Drilling down into the Government and Commercial segments, both performed well. The commercial revenue stream continues to grow rapidly, while government contracts have grown more moderately. Commercial growth was impressive for the year, though it slowed some in Q4 year-over-year.

Palantir Q4 Investor Letter

Commercial revenue grew 11% year-over-year to $215 million, but U.S. commercial revenue grew 12% year-over-year to $77 million. Customer count continues to grow. The U.S. commercial customer count increased 79% year-over-year, from 80 customers in Q4 2021 to 143 customers in Q4 2022, which is solid growth.

Government segment also growing

In past quarters, the Government segment revenues had slowed their growth somewhat. In Q4, Government segment revenue grew 23% year-over-year to $293 million. Revenue per customer is up as well, but compared to years past we do have to acknowledge that the revenue growth has clearly decelerated. While it is still strong, it is not lights-out growth anymore. Now, that said, with more and more war games going on in the world, we do believe that the government segment will see increased demand as global risks increase.

Margin power

Palantir Technologies Inc. has enjoyed strong margins. For those of you who are following software companies, you know how important margins are in a software company. Well, adjusted income from operations came in at $114 million, representing a margin of 22%, while cash from operations were $79 million, representing a 15% margin. We will also point out that adjusted free cash flow was $76 million, representing a 15% margin.

Now, we will say that these are decent margins, but margins were lower than a year ago on these measures. However, overall sales adjusted gross margins, which excludes stock-based compensation expense, was 81% for the year and 82% for the quarter, and that is quite strong. This helped lead to positive earnings.

Looking ahead

We stand by our call that Palantir Technologies Inc. is an AI company at its heart, and the company is benefiting from war games and ongoing chaos globally. The company is also helping companies crunch data and create information to help decision making.

Palantir is forecasting being profitable all year in 2023, and this is sending shares surging. While margins are strong, the company is committed to being disciplined on its spending across the company. Palantir will be slowing hiring while being tactical in investments made to product offerings. The company expects operating income margins over the course of the year to improve.

Keep in mind that Palantir has a pristine balance sheet of $2.6 billion in cash and cash equivalents, and no debt at all. For all of 2023, the company is forecasting revenue to be between $2.18 billion and $2.23 billion, while adjusted income from operations should be between $481 million to $531 million. The company will also be “GAAP profitable this year.” While AI dominates the headlines, Palantir is a true AI winner.

Final thoughts

War games seem to be a real catalyst for Palantir Technologies Inc., while recession could be either a negative or positive catalyst, that is unclear to us. Customer growth continues. AI is a hot topic, but Palantir Technologies is a real AI play. That is what it does. Sure, Palantir Technologies Inc. stock remains expensive on most valuation metrics, but having strong margins and being profitable in 2023 changes the outlook here. We think PLTR shares are a strong buy in the single-digits.

Be the first to comment