Michael Vi

Palantir Technologies (NYSE: NYSE:PLTR) is a public American software company with a market capitalization of $20 billion. The company has dropped roughly 70% from its 52-week high, joining in on a strong technology sell-off. However, despite that, the company continues to have substantial earnings potential, making it a valuable investment.

Palantir 2Q 2022 Highlights

Palantir had an impressive quarter despite the market’s opinion on it.

Palantir Investor Presentation

The company is still in growth mode and growing rapidly. Revenue grew to almost $500 million in the quarter with a customer count of more than 300. That’s an almost doubling of the company’s customer count. The company’s U.S. business generated more than $1 billion in TTM revenue and the company’s US commercial revenue has grown even faster.

The company, on nearly every metric worth tracking, had an incredibly strong quarter.

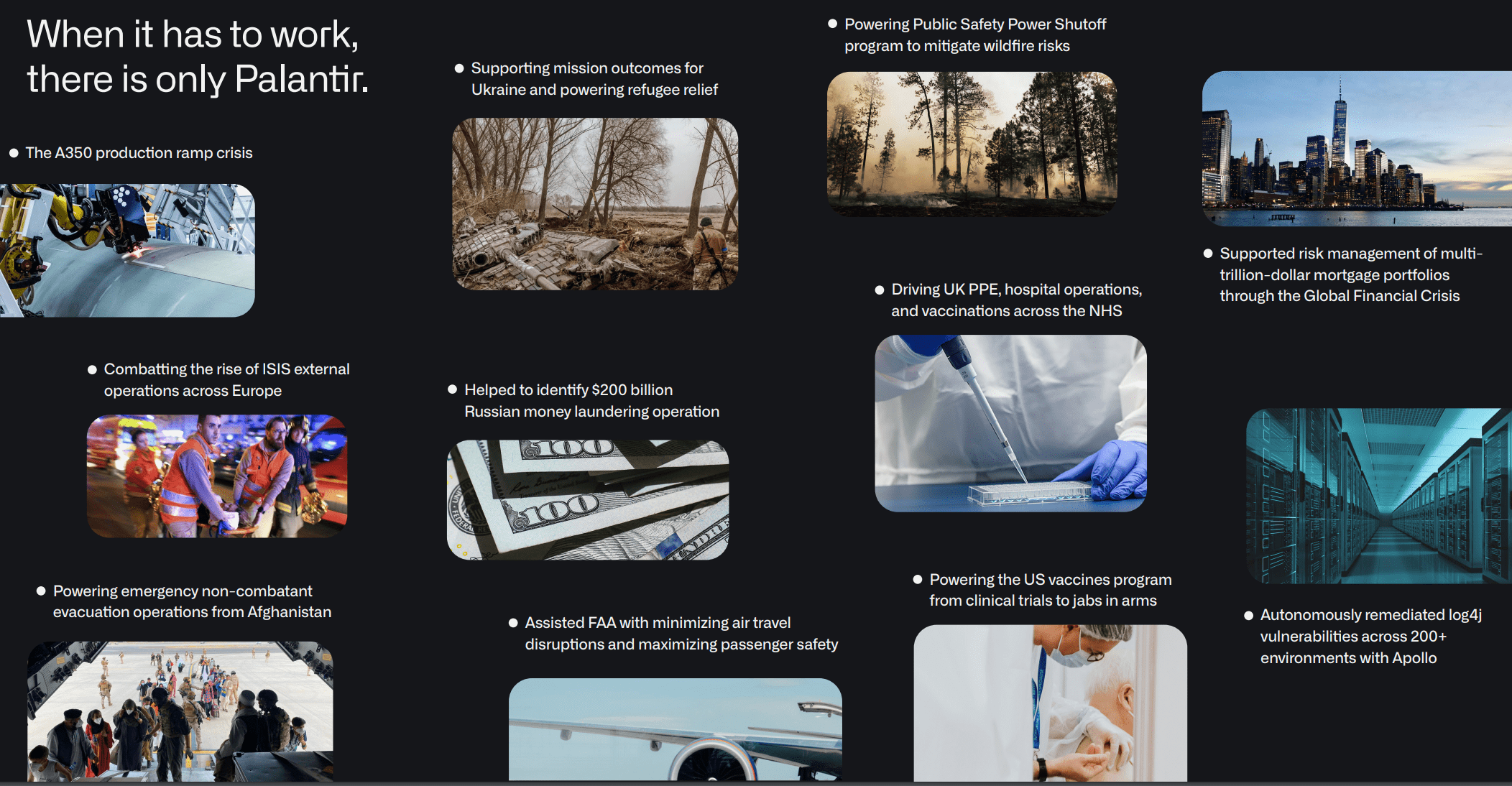

Palantir Asset View

Palantir takes all the latest technology and brings it to new scales to support enterprises without the same technological experience.

Palantir Investor Presentation

The company has helped with numerous corporate problems across the world. The company has helped identify a massive money laundering operation, production ramp crises, and risk management. The company’s unique technology, which has expanded significantly since going public, allows the company to provide peer-leading technology.

The company likes to say it’ll be to the next decade as AWS was to the last. We believe it. AWS replaced the need for homegrown datacenters, which were tough to scale and expensive. We believe Palantir. Palantir will replace the need for homegrown software solutions which are expensive and tough and slow to customize.

Will the company ever replace Facebook’s engineers. No, Facebook has the scale to do it itself. That’s why Facebook has its own data centers instead of AWS. But we do expect it to replace complex SW engineering tasks for a multitude of governments and companies.

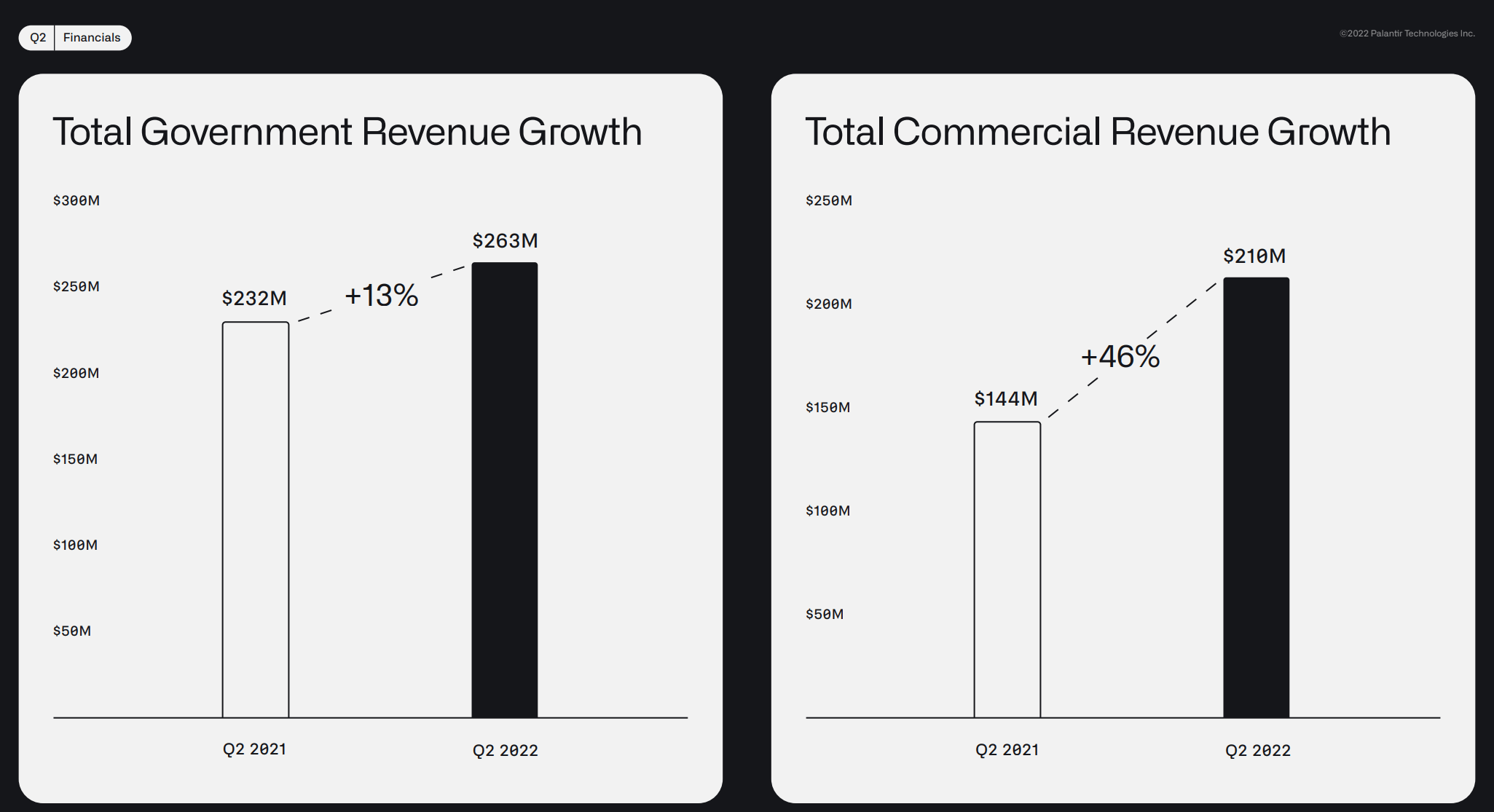

Palantir Financial Performance

Financially, Palantir performed well.

Palantir Investor Presentation

The company ended the quarter with 119% in net dollar retention and more than $1 billion in TTM commercial revenue growth. The company’s government revenue growth slowed down, although, to be fair, it was a tough time for governments around the world to operate and perform. The company did manage to grow customers by 10% QoQ.

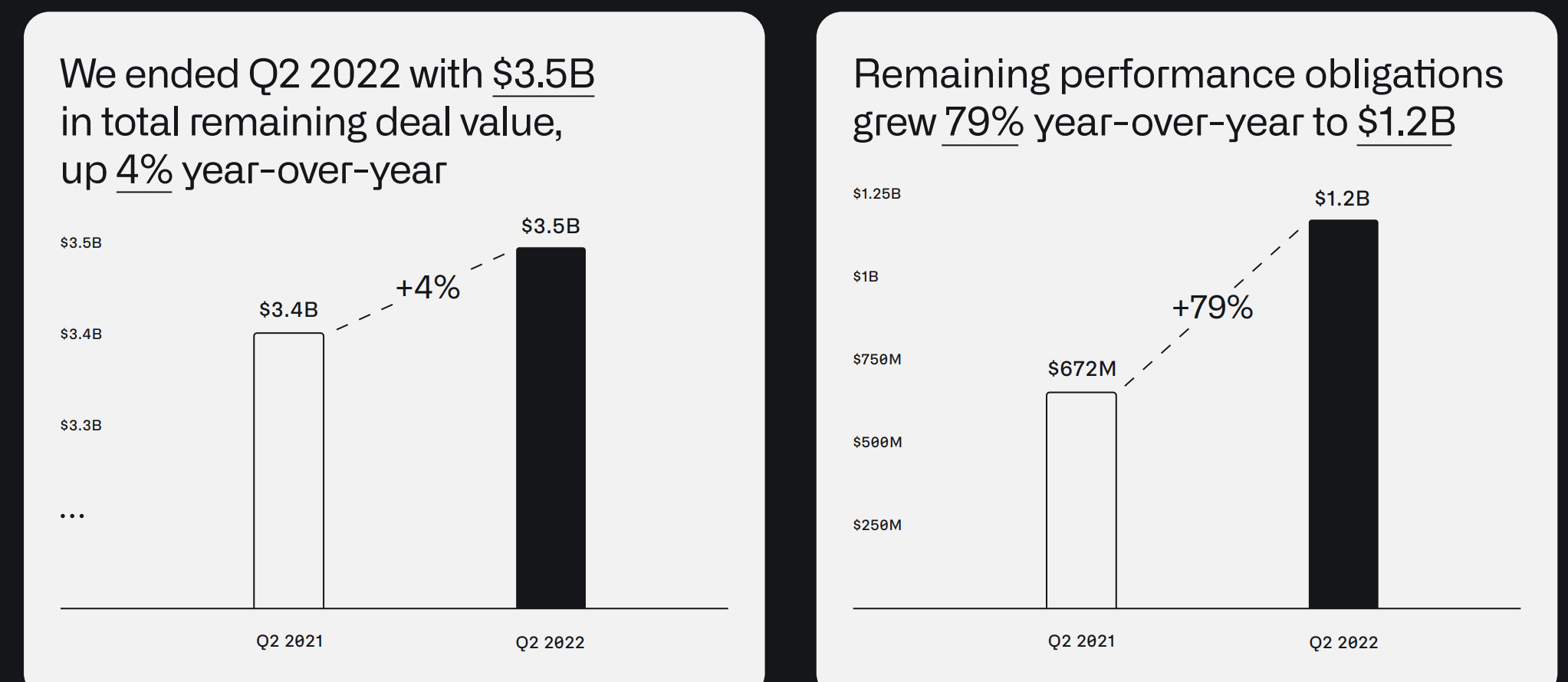

Palantir Investor Presentation

The company managed to achieve a more than 80% gross margin. The company ended the quarter with $3.5 billion in remaining deal value, up by the mid-single digits YoY, which represents <2 years of revenue but still a reasonable backlog. The company also managed to substantially grow its performance obligations YoY to $1.2 billion.

From a valuation perspective, the company has $2.4 billion in cash and no debt, representing a 12% net cash position on its market capitalization. The company’s annualized FCF is $250 million, which represents a ~1.5% FCF yield, low, but also impressive for a company that has been growing rapidly by double-to-triple digits.

The company’s revenue forecast for the next quarter is $475 million representing roughly constant revenue with the most recent quarter. Annualized revenue is expected to stay in line with that.

Palantir Expansion Model

We expect Palantir’s expansion model to cause substantial shareholder returns.

The company has 3 phases. Acquiring new customers. Increasing revenue per customer. Growing the scope of business it handles for each customer. The company has proven the success of this model with its gross margins of more than 80% and the double strength of new customers and revenue growth per customer shows the company’s overall financial strength.

The company’s expansion model here is why we believe the company will be able to rapidly accelerate its FCF yield. Selling too other companies is tough, expensive, and slow work. However, the company does have a strong and successful history of growth and we expect that to continue growing going forward.

Palantir Thesis Risk

The largest risk to the company’s thesis is that its future is based on continued growth. The company has reasonable FCF, but it needs that growth to continue to justify its valuation. With rumors of a recession, customers will be reluctant to start new contracts and deals which could work to significantly slowdown the pace of the company’s growth.

Conclusion

Palantir has a unique portfolio of assets that we expect the company to be able to use to grow. The company says it’ll be to the next decade what AWS was to the last, and we agree. The strength of the company’s offerings portfolio means the ability to replace work and provide companies with better results and margins.

The company has an incredibly strong net cash position. The company is profitable in its growth phase, something that most tech companies don’t manage to do. While the company needs growth in order to justify its valuation, it has continued to grow well, and we see that making the company a valuable long-term assets.

Be the first to comment