Getty Images

On February 1, 2020, I recommended readers to pare equal positions in diversified Marcellus natural gas company National Fuel Gas (NYSE:NFG) with oil and gas royalty firm Dorchester Minerals, L.P. (DMLP). NFG offers both a unique diversified energy profile with a focus on the Marcellus and an advantageous E&P cost profile. DMLP offers a high-yield energy income profile directly tied to the commodity price of oil and gas, with the tax “advantages” of a limited partnership. After 3 years, a revisit of this paring should be in order. Both have done exceptionally well, but one is still considered a “buy” while the other is more of a “hold”, or a “lukewarm buy with elevated risk”, even though they both offer acceptable valuations in a still overvalued market.

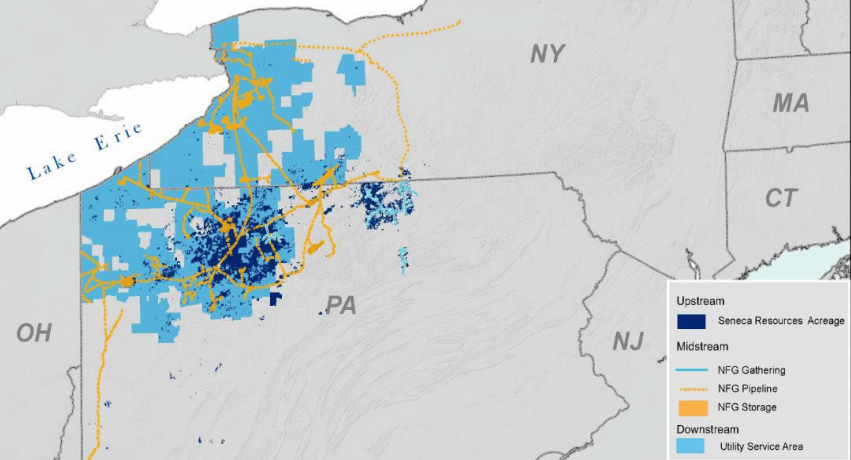

National Fuel Gas operates in three distinct segments of the natural gas supply chain. NFG operates Seneca Resources, an E&P natural gas driller with over 1 million acres in the Marcellus, 700,000 of which are owned by NFG and 300,000 leased with royalty payments due on production. NFG also owns Marcellus gathering pipeline networks and interstate pipelines in NY state. With their pipelines, NFG operates natural gas processing plants. In addition, NFG operates the regulated natural gas LDC utility for Buffalo NY and Eire PA. The graphic from the latest FY 4th quarter investor’s presentation outlines NFG’s major assets and locations.

Map of NFG Assets (National Fuel Gas Presentation)

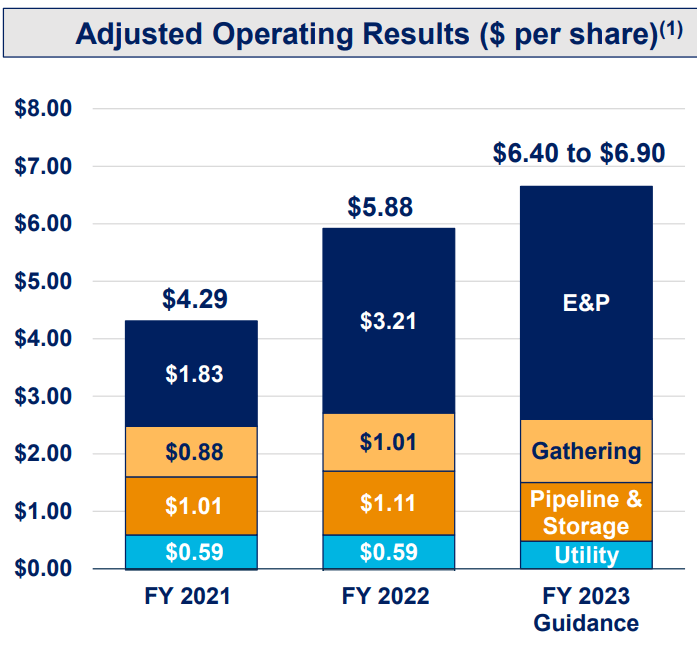

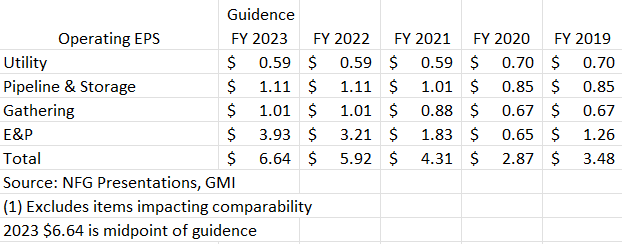

As it should be expected, National Fuel Gas has been a beneficiary of rising natural gas prices. The graphic from the 4th qtr. presentation and table below outline operating earnings per share from FY 2019 to management’s guidance FY 2023 for each segment, excluding items impacting comparability, such as one-time non-cash charges. The table reflects both the presentation graphic and previous results from my earlier SA articles. As shown, the NY Utility segment’s operating EPS has declined by 16%. However, this is more than offset by growth of 31% in the Pipeline and growth in Storage and Gathering of 51%. The E&P segment operating EPS is expected to grow 212% from 2019 to management’s guidance for FY 2023.

Operating Earnings NFG by Segment (National Fuel Gas presentation) Operating Earnings per share 2019 to 2023 Guidance (Morningstar, NFG, GMI)

Of interest to investors should the integrated nature of National Fuel Gas various energy businesses. Often overlooked is that NFG owns its entire 700,000-acre Western Development Area WDA. This simple fact saves the company about 17% of revenues on production royalty costs, which is the average NFG pays on its 300,000-acre Eastern Development Area EDA production. In addition, NFG operates an extensive Gathering Pipeline network. Management has a stated goal of utilizing in-house gathering pipes for all production additions. According to the company, 90% of Seneca’s 2023 in-field gathering pipeline costs associated with its production lease and operating expenses LOE will be paid to NFG’s Gathering Segment. NFG is the epitome of a company creating multiple layers of profit on the same atom of energy.

A major consideration for Marcellus E&P natural gas firms are its restricted exit profile. Anti-natural gas regulators and judges have repeatedly thwarted pipeline expansion programs to the north (NY) and to the east/south (NJ, VA). National Fuel Gas has been battling the NY environmental lobby since 2014 for its Northern Access Pipeline which is expected to deliver new supplies to Canada, the Midwest, and Western NY. The latest twist with the NY Dept of Environmental Conservation is DEC’s permitting delay tactics past their own decision deadline was ruled by the courts as being sufficient to allow the project to move ahead. The FERC has approved the pipeline with an extension deadline for completion by Dec 31, 2024. 75% of the nameplate capacity is expected to be exported to Canada through NFG’s pipeline connection in Chippawa, Ont. As the political climate east of the Appalachians remains hostile to natural gas development, the State of Ohio is following the 2022 lead by some European nations to retag natural gas as “green”. The Ohio legislature has legally redefined natural gas as a source of “green energy”. With natural gas now a “green” fuel in Ohio, this change could provide an interesting future for additional pipeline exit capacity to the west.

National Fuel Gas has paid an uninterrupted dividend since 1901 and is considered a “Dividend King” for its 52 years of continual dividend growth. While NFG is in an elite group of only 41 companies with 50+ yrs of dividend growth, its natural gas E&P earnings cyclicality and volatility should be acknowledged. NFG guidance for FY 2023 EPS is $6.65 mid-point, with FY 2024 consensus at $7.39. Shares are currently trading at $60.50 and yield 3.07%.

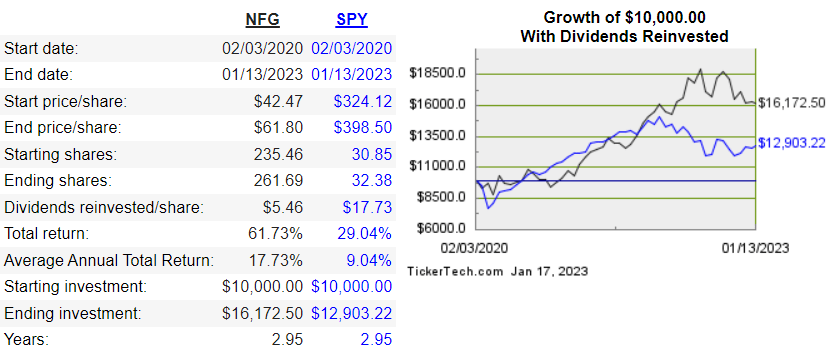

As of 1/17/23, according to dividendchannel.com, since Feb 1, 2020, National Fuel Gas has generated a 17.73% average annual return with dividends reinvested. A $10,000 investment on 2/1/20 would be worth $16,172. The S&P 500 (SPY) has generated an 9.04% average annual return over the same period and a similar investment would be worth $12,903.

This is my 17th article on NFG since Jan 2012 and NFG has been a core energy holding for my portfolios since last century.

NFG Performance vs SPY (dividendchannel.com)

Dorchester Minerals Limited Partners is a diversified, debt-free, oil and gas royalty firm which distributes most of its revenue to unitholders. DMLP operates in many of the major E&P fields, with about 65%+ of reserves in the Permian Basin. From its 2021 annual report presentation, current production is about evenly split 48% oil and 41% natural gas. Similar to other O&G royalty firms, DMLP is paid a royalty based on well production matrix and its revenue and distribution is directly tied to the commodity price of oil and gas. Unlike many of its peers, DMLP has no debt, does not generate MLP UBTI, and has grown by finding more proven reserves on land it already owns. Formed in 2003, DMLP started with 15.7 MMboe. From Feb 2003 to Dec 2022, DMLP produced 40.1 MMboe, found 39.9 MMboe termed “revisions” on its existing land, and added 15.7 MMboe through acquisitions. As of the end of 2022, DMLP had proven reserves of 15.5 MMboe.

One issue with Dorchester Minerals is its lack of investor information. Management usually issues a very short 8-k quarterly filings with barebones reporting of revenues, net income, and net income per common unit. More insight into DMLP’s operation and finances can be found in the Sept 30,2022 10-Q.

Over the past 10 years, Dorchester Minerals has paid a total of $16.26 per unit in distributions, issued an annual average of 2.0% more shares for acquisitions, and has maintained approximately the same level of reserves for future production. Of importance to unitholders is the composition of DMLP reserves. According to the 2013 Annual Report, oil reserves comprised 25% of total with natural gas comprising 65%. Over the past 10 years, DMLP has expanded its oil reserves to a more balance 48% oil and 41% gas of the total MMboe.

The table below outlines the distribution, revenues per share, and the percent of revenues paid to unitholders through the variable distribution by year from 2013 to TTM 9/2022. As shown, Dorchester Minerals pays out a high percentage of its revenues to unitholders.

DMLP Distribution per unit, Revenues per unit, % of Distribution to Revenues 2013 – 2022and (Morningstar, NFG, GMI)

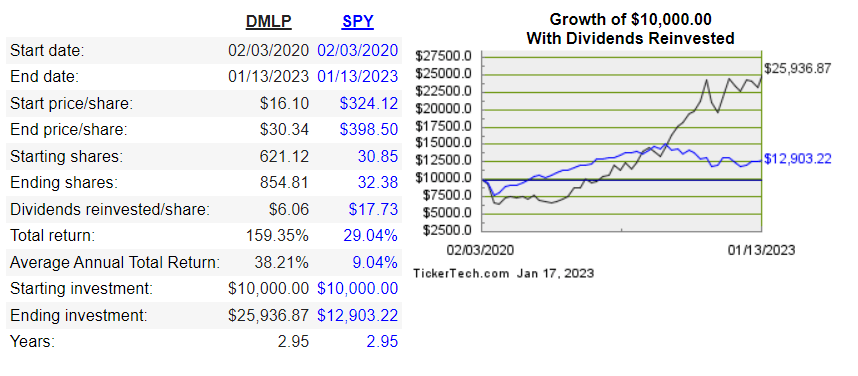

Dorchester Minerals is current trading at $30.20 with a 11.66% yield, based on annual distributions of $3.50 per unit. As of 1/17/23, according to dividendchannel.com, since Feb 1, 2020, Dorchester Minerals has generated a 38.21% average annual return with dividends reinvested. A $10,000 investment on 2/1/20 would be worth $25,936. The S&P 500 has generated an 9.04% average annual return over the same period and a similar investment would be worth $12,903.

DMLP Performance vs SPY (dividendchannel.com)

This is my 14th article on Dorchester Minerals since Feb. 11, 2010. I have been a very pleased unitholder since 2006 and DMLP is another core energy holdings in my portfolios. Since it generates a K-1 and offers tax advantaged income, I always recommend holding DMLP in taxable accounts to take full benefit of its MLP-related delayed tax provisions.

It is a bit unfair to compare energy stock performance to the S&P 500, except as an example of their outperformance to large cap, more blue-chip investments. Early 2020 was a tough time for most energy stocks, with many oil and gas selections outperforming the SPY over the past 3 years. When compared to the S&P Energy ETF (XLE), NFG underperformed and DMLP outperformed. Since Feb 1, 2020, XLE has generated a 26.29% average annual return and a similar $10,000 investment would be worth $19,886. This beats NFG at 17.73% and $16,172 but falls short of DMLP at 38.21% and $25,936, respectfully.

Both stocks are very susceptible to changes in commodity energy prices. However, I believe Dorchester Minerals is more exposed to the oil and gas commodity price cycle than National Fuel Gas. While DMLP offers a variable and currently large distribution, as shown by the table above, both revenues and distributions are subject to dramatic changes – both up and down. I rate NFG as a “Buy” for longer term energy investors looking for a quality management team benefitting from unparalleled Marcellus assets, and I plan on adding more with further price declines below the $57 range. If I didn’t own NFG, I would not be afraid to begin a position at current levels.

Since Dorchester Minerals is connected at the hip to commodity prices, I currently rate DMLP as a “Hold” or a “Lukewarm Buy at Best, with Elevated Risk”. I have found with investments directly tied to commodity prices, such as O&G royalty and timber firms, it is best to buy and add when prices are under duress – which is not the current situation. Looking back in history, DMLP has traded above its $30 current price only twice before, in 2008 and 2014. Both peaks were followed by a collapse in commodity prices, and DMLP bottomed at under $12 in 2016 and 2020. I would feel more comfortable to review DMLP prices when crude declines to the $65 range and lower. While the units provide a great current yield for income, the risks to a decline in unit price commensurate with a drop in energy prices currently pushes me to the sideline. With the difficulty in forecasting oil prices with any accuracy, DMLP is best viewed as an income selection best accumulated during times of weak oil prices.

Be the first to comment