Nikita Burdenkov/iStock via Getty Images

A Quick Take On Pactiv Evergreen

Pactiv Evergreen (NASDAQ:PTVE) went public on September 16, 2020, raising approximately $574 million in gross proceeds in an IPO that priced at $14.00 per share.

The firm provides food service packaging to customers with worldwide operations.

While PTVE has experienced volatility in the past year, management’s divestment and deleveraging actions, combined with a modest increase in forward revenue expectations, indicate that the worst may be over for the stock.

Accordingly, my outlook on PTVE is a Buy at around $11.00 per share.

Pactiv Evergreen Overview

Lake Forest, Illinois-based Pactiv was founded to produce food and beverage packaging solutions for a wide range of product types.

Management is headed by Director and Chief Executive Officer Michael King, who has held leadership positions at TI Automotive Fuel Systems, Lear Corporation and Huhtamaki.

The company counts major global companies as customers, including McDonald’s, Starbucks, Tyson, Kraft Heinz, Conagra, Coca-Cola and Danone.

The firm offers more than 13,000 products produced by 900 production lines and is the largest producer of free food and beverage packaging in North America, according to management.

Pactiv’s Market & Competition

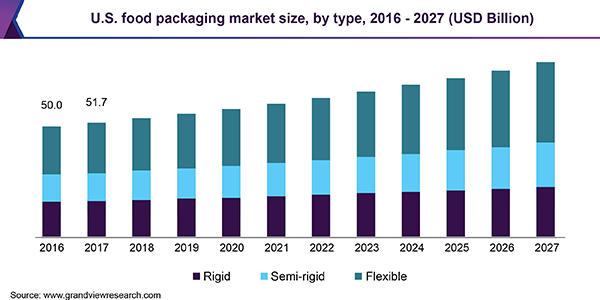

According to a 2020 market research report by Grand View Research, the global market for food packaging was an estimated $303 billion in 2019.

The market is expected to grow at a CAGR of 5.2% from 2020 to 2027, reaching a forecast amount of $455 billion.

The main drivers for this expected growth are an increasing desire for food and beverage convenience, greater performance, improved shelf life and a reduced environmental footprint.

Also, the U.S. market is expected to grow via an increased urban population desiring packaged food and single-serve packaging.

Below is a chart indicating the historical and projected U.S. market size growth by type of package:

U.S Food Packaging Market (Grand View Research)

Major competitive or other industry participants include:

-

Dart Container

-

Berry Global Group (BERY)

-

Genpak

-

Sonoco

-

Paper Excellence Group

-

Amcor

-

Sealed Air Corporation

-

Silgan holdings

-

SIG Combibloc

-

Elopak

-

Huhtamaki Oyj

-

Stora Enso Oyj

Pactiv Evergreen’s Recent Financial Performance

-

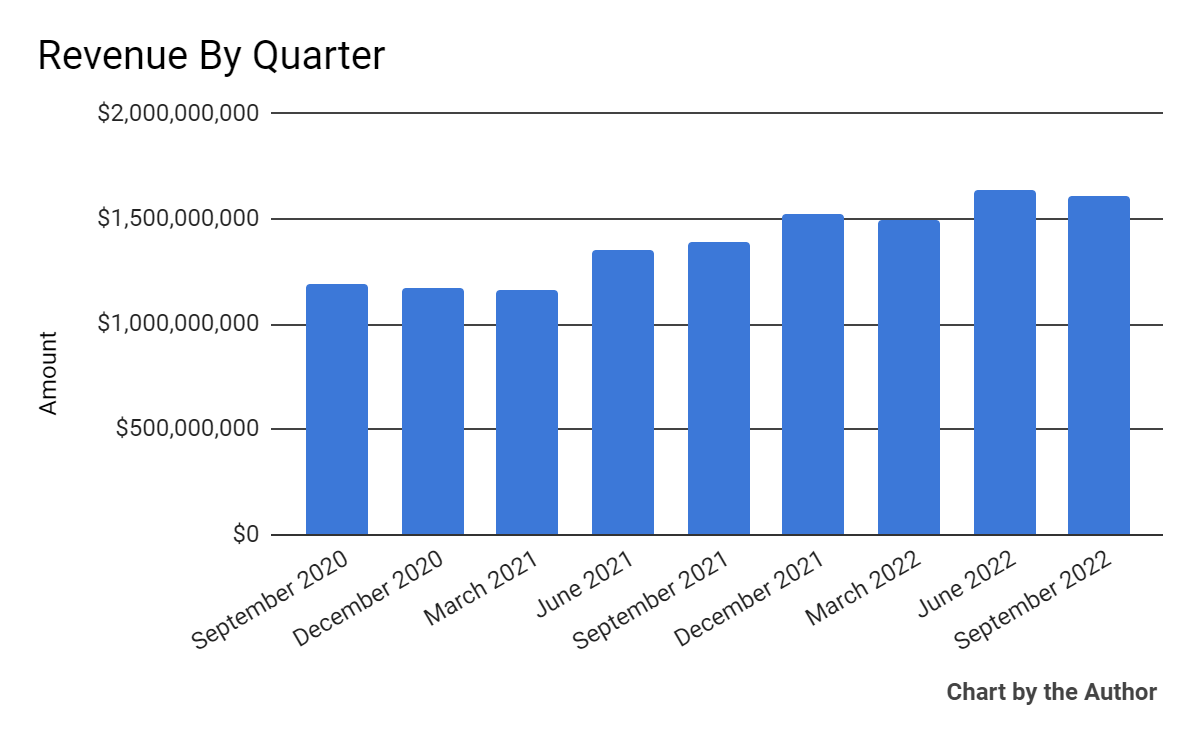

Total revenue by quarter has grown per the following chart:

Total Revenue (Seeking Alpha)

-

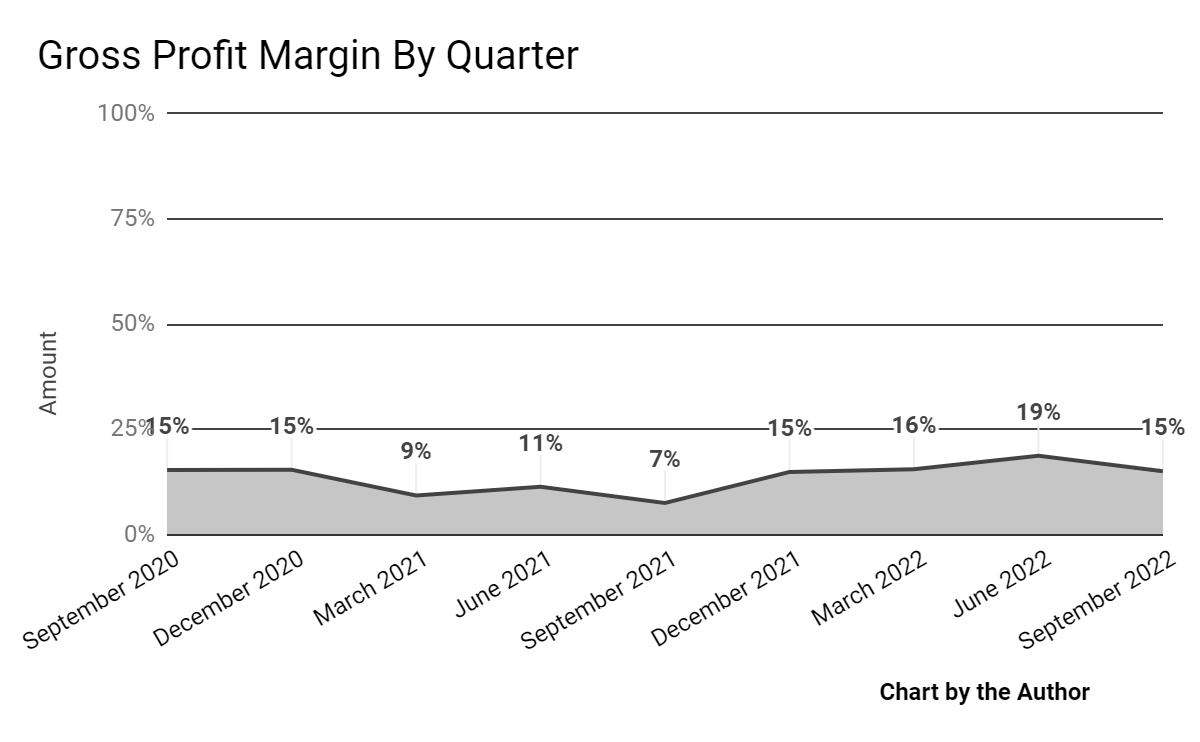

Gross profit margin by quarter has risen markedly in recent quarters:

Gross Profit Margin (Seeking Alpha)

-

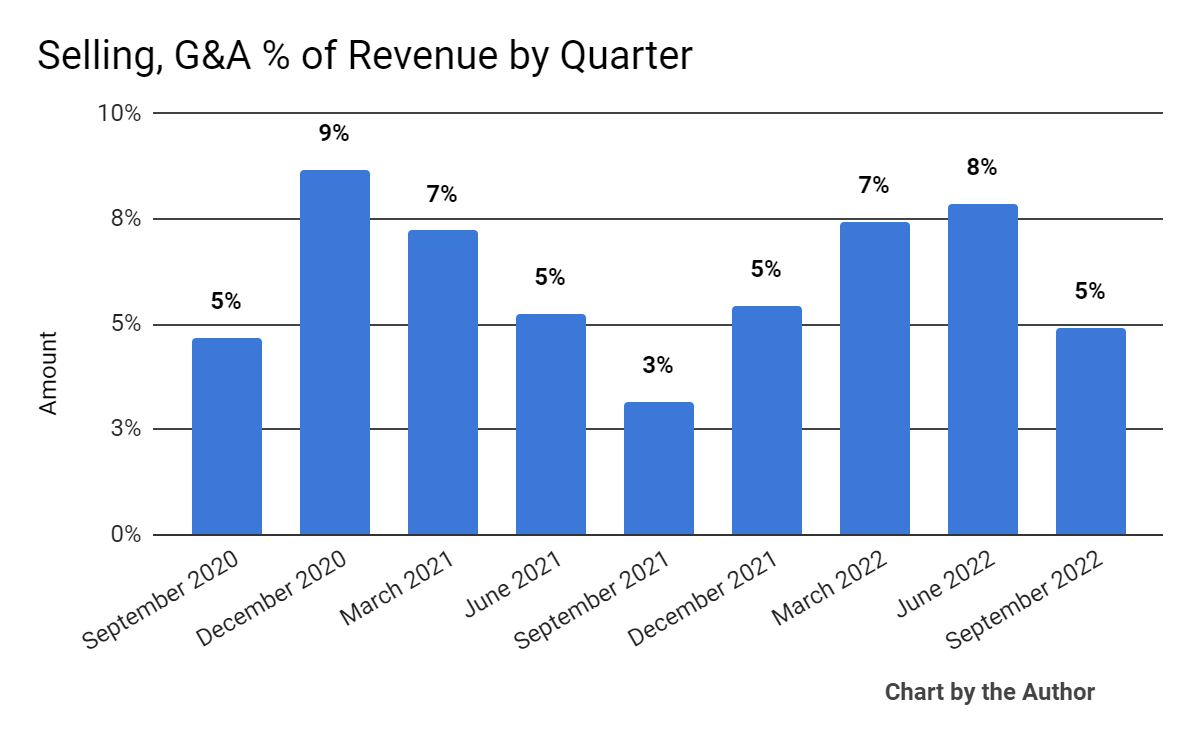

Selling, G&A expenses as a percentage of total revenue by quarter have varied within a narrow range:

Selling, G&A % Of Revenue (Seeking Alpha)

-

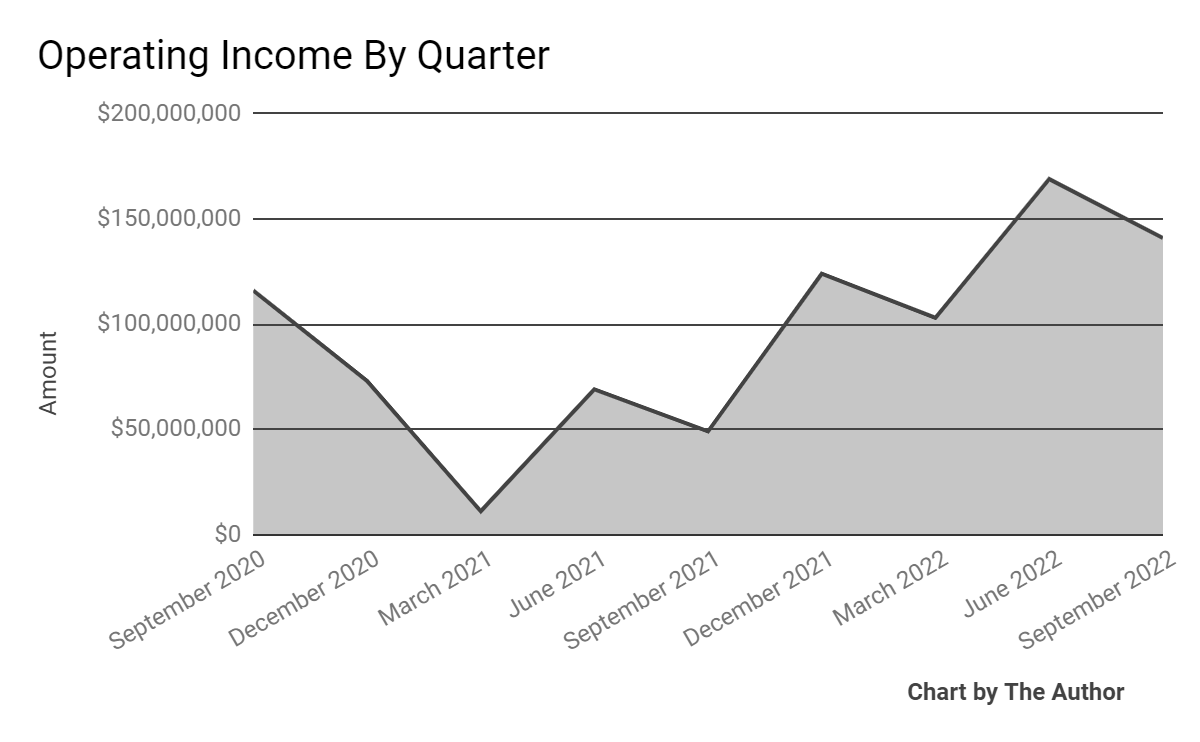

Operating income by quarter has risen substantially in recent quarters:

Operating Income (Seeking Alpha)

-

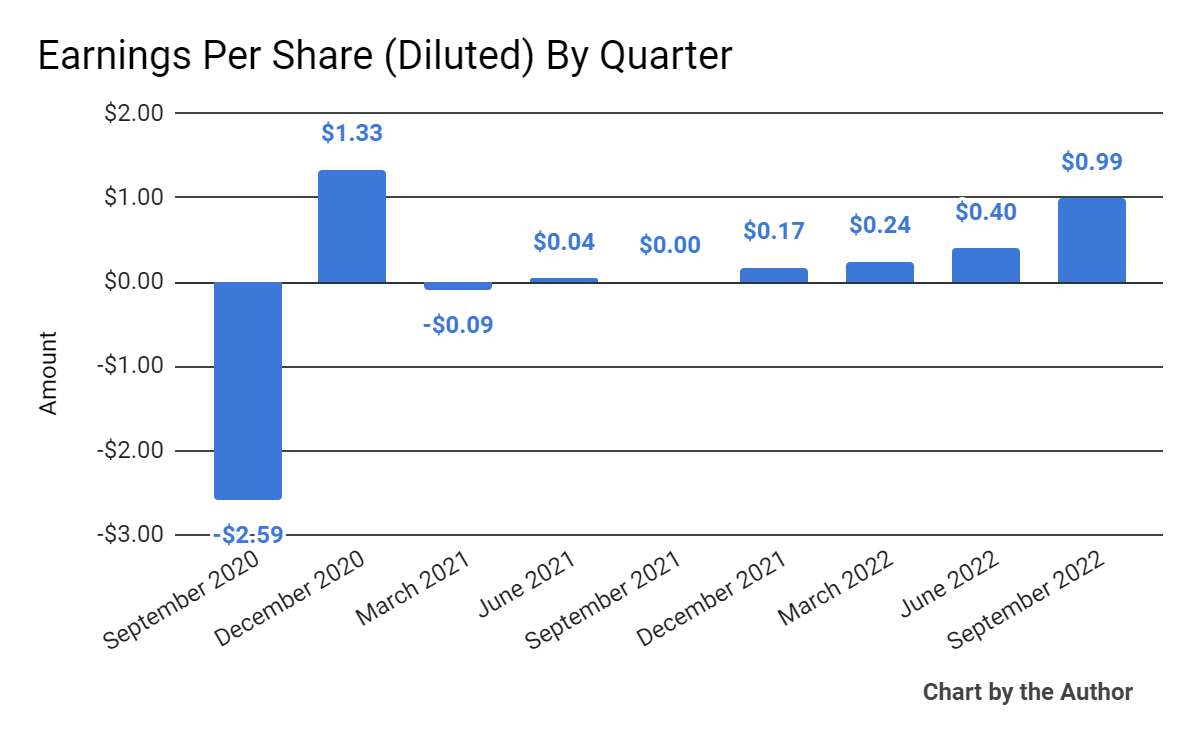

Earnings per share (Diluted) have also risen significantly more recently, as the chart shows here:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

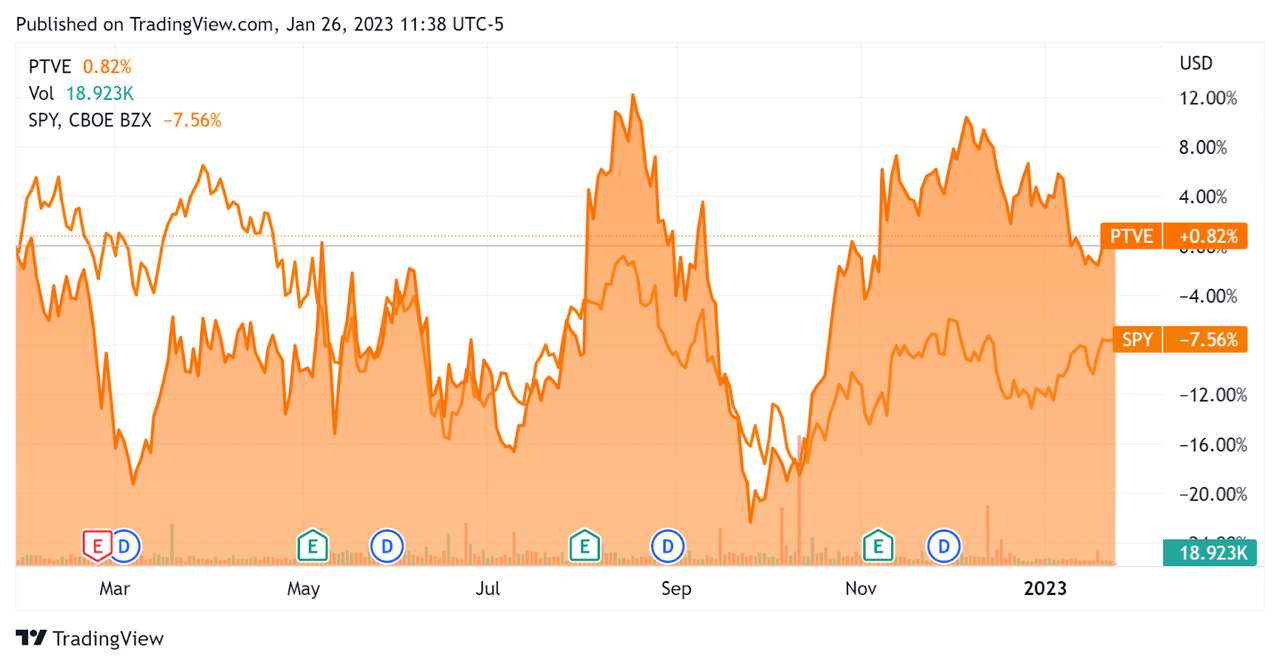

In the past 12 months, PTVE’s stock price has risen 0.8% vs. the U.S. S&P 500 index’s drop of around 7.6%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Pactiv Evergreen

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.0 |

|

Enterprise Value / EBITDA |

6.8 |

|

Revenue Growth Rate |

23.3% |

|

Net Income Margin |

5.2% |

|

GAAP EBITDA % |

14.0% |

|

Market Capitalization |

$1,977,170,050 |

|

Enterprise Value |

$5,942,170,100 |

|

Operating Cash Flow |

$312,000,000 |

|

Earnings Per Share (Fully Diluted) |

$1.80 |

(Source – Seeking Alpha)

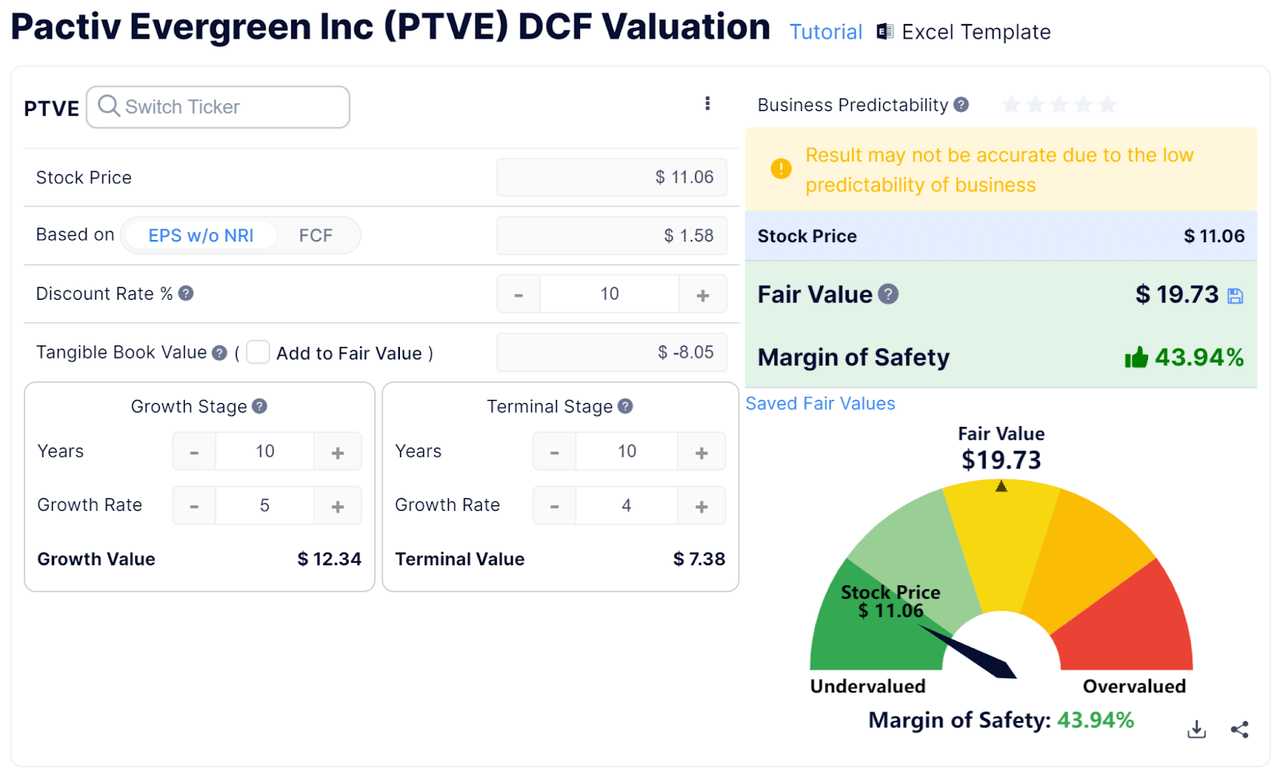

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

Discounted Cash Flow Calculation (GuruFocus)

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $19.73 versus the current price of $11.06, indicating they are potentially currently substantially undervalued, with the given earnings, growth, and discount rate assumptions of the DCF.

Commentary On Pactiv Evergreen

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted closing the sale of its Evergreen Asia business and reducing its net leverage as part of an overall plan to get to sub-4 times net debt-to-EBITDA.

Obviously, the rise in interest rates has hurt the heavily indebted company, so management has sought to reduce its effects by deleveraging as quickly as possible.

Notably, the firm has made progress in alleviating the staffing shortages and is now ‘at target staffing levels in almost every area of the business.’

Also, the company has ‘restored’ its inventory levels to target and ‘improved our overall service and delivery with our customers to pre-2019 levels.’

As to its financial results, total revenue rose 15% year-over-year, to a record for the company since it went public.

However, PTVE has been negatively impacted by inflationary pressures, impacting margins.

In response, management has sought to pass through higher input costs, which have been abating in months after the end of Q3.

For the balance sheet, the firm ended the quarter with $559 million in cash and equivalents and $4.18 billion in total debt.

Over the trailing twelve months, free cash flow was $60 million, of which capital expenditures accounted for $252 million. The company paid $18.0 million in stock-based compensation.

Looking ahead, management increased its full year 2022 revenue guidance from $760 million at the midpoint of the range to $770 million, which management characterized as a ‘modest increase.’

However, leadership currently has ‘less visibility into end market demand due to varying factors, including inflationary pressures, along with actions by the Fed to reduce inflation and the impact these actions will have on the broader economy.’

Regarding valuation, my discounted cash flow calculation, which assumes low growth, indicates the stock may be significantly undervalued at its present price level.

The primary risk to the company’s outlook is that interest rates will stay higher for longer, keeping its interest expense elevated and potentially negatively impacting end-user demand.

A potential upside catalyst to the stock could include a ‘short and shallow’ economic downturn, which would buoy end-user demand and support further revenue growth.

Also, the company closed its acquisition of Fabri-Kal which will broaden its sustainable packaging offerings in the foodservice and consumer brand packaging industries.

While PTVE has experienced volatility in the past year, management’s divestment and deleveraging actions, combined with a modest increase in forward revenue expectations, indicate that the worst may be over for the stock.

Accordingly, my outlook for PTVE is a Buy at around $11.00 per share.

Be the first to comment