Mohammed Haneefa Nizamudeen/iStock via Getty Images

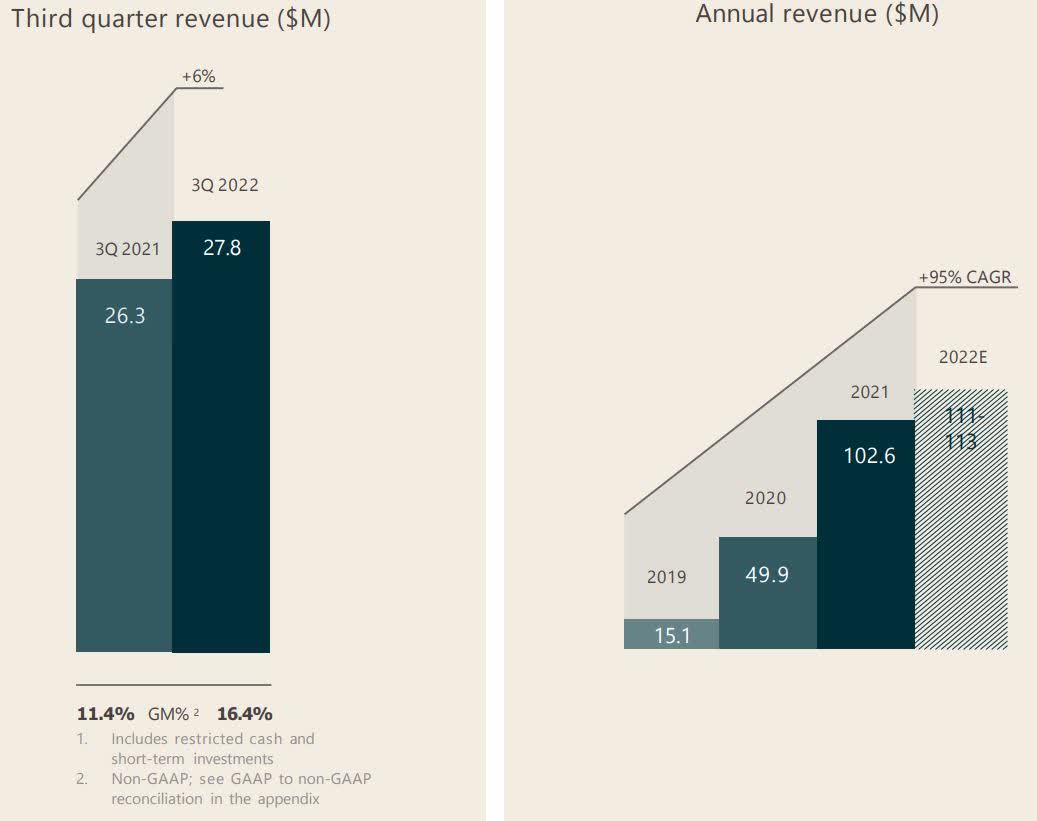

Outset Medical, Inc. (NASDAQ:OM), a company that develops a hemodialysis system for dialysis in the home and the hospital, has generated CAGR for revenue of 95 percent since 2019, and based upon demand and reimbursement, should continue to generate revenue growth.

With the ongoing transition to home care and reimbursement, along with growth in hospital acute care, the company has a nice growth runway ahead of it that should continue on for at least the next several years.

One headwind it faces is a shortage of dialysis nurses, which it is partially mitigating by introducing a bridge program will lead to full-time hiring to help fill the shortage.

While the company reported a net loss of almost $41 million in the latest quarter, it’s not that concerning to me because it’s largely a part of its marketing strategy to scale, which over time, as it brings results, will improve gross margin and earnings.

With plenty of access to capital and a tailwind at its back in regard to preference for easy-to-use and easy-to-understand dialysis treatment, the company is poised for long-term growth that should reward shareholders.

In this article, we’ll look at some of its latest numbers, challenges it faces, and why I’m optimistic about the company’s performance over the next few years.

Some of the numbers

Revenue in the third quarter was $27.8 million, compared to $26.3 million generated in the third quarter of 2021. Breaking it down, revenue from products was $21.7 million, slightly down from the $21.8 million in revenue from products in the same quarter of 2021, and Service revenue was $6.0 million in the reporting period, up 34 percent from the $4.5 million in revenue in third quarter of 2021.

Company Presentation

Gross margin in the third quarter was 15.6 percent, compared to 11.2 percent year-over-year. Gross margin for product was 9.7 percent, up from the 5.9 percent for product gross margin in the third quarter of 2021. Service and other gross margin was 37 percent, up slightly from the 36.7 percent gross margin in the segment for the same reporting period in 2021.

Operating expenses in the third quarter were $38.1 million, with sales and marketing accounting for the bulk of that.

Net loss in the reporting period was ($40.8 million), or ($0.85) per share, compared to the net loss of ($30.5 million), or ($0.65) per share in the third quarter of 2021.

I’m actually not too concerned about the numbers here because the company should be able to continue to sustainably increase revenue over the next several years, and with about half of its operating expenses in sales & marketing and based upon its revenue growth over the last several years, it is highly probable that expenditure will pay off in the long run.

As the company scales, it’ll reduce costs, widen margins, and move it toward positive cash flow.

With OM gaining share on product and expanding its higher-margin service segment, that’ll improve the numbers going forward.

With cash and cash equivalents and short-term investments of $260.8 million, and a new 5-year loan arrangement with SLR Capital Partners of up to $300 million, the company has more than enough liquidity to execute on its growth strategy in the years ahead.

Share price movement and entry point

After recently falling to its 52-week low of $11.41 per share on November 8, 2022, OM has made a big move to the upside, more than doubling to $22.41 per share at the end of trading December 5, 2022.The company is trading near a double top at where it traded on August 15, 2022, so it’s probable prudent to wait to see if it will be able to break through that mark and continue on its upward trajectory or fall back once again before it potentially breaks out.

TradingView

Where the company stands today, I do think it has some upside left, but after the recent doubling in price after its 52-week low, the risk-reward has been significantly reduced, so in my opinion it would be better to wait for a lower entry point before taking a position.

The reason why is I think the short-term catalysts are already priced in, and investors will have to wait until the next quarters to see how the company is increasing revenue and how its gross profit and margin respond to that.

With the opportunity in front of it I think the company will have to continue to spend on sales and marketing. If it proves that it can improve gross margin and move toward positive cash flow while doing so, I think it’s going to rebound nicely over the next several years.

Tailwinds and Challenges

A couple of tailwinds the company had in the third quarter and which are likely to continue are in regard to building its home device business back up, and its ongoing expansion in acute care in hospitals.

Concerning its home order book, management noted the progress it was making in rebuilding that part of its business, acknowledging it’s still in the early stages of the process and expecting momentum to build going forward. With a significant backlog the fourth quarter should be a good one for home placement and consulting. For the full year management expects home placement to represent approximately 15 percent of total revenue.

Home orders for the device have more than doubled since the same quarter of 2021.

Concerning increasing its footprint in hospitals, in the third quarter it expanded to “one of the largest regional healthcare systems in the country with 50 hospitals in nine states.” Now that it has increased its installed base, the challenge is to boost utilization in order to leverage the growing expansion. That will add to its recurring revenue business. One of the major headwinds the company continues to face is the ongoing shortage of dialysis nurses in the U.S., which management sees remaining throughout 2023.

In response to the shortage and to partially mitigate it, OM launched a program that will help bridge the shortage.

What the “bridge” program entails is providing short-term dialysis nurses at hospitals to meet the needs of patients, including in ICU units and at bedside in the hospitals. As the hospitals hire permanent dialysis nurses OM nurses will assist in training and onboarding. It’s still in the early stages, but the company says it’s seeing good results so far.

Since hospital care is still the majority of OM’s business at this time, it’s important for them to mitigate this issue in order to take advantage of the demand for its in-hospital treatment.

Conclusion

Outset Medical appears to have found it bottom and based upon increasing its home dialysis placement and expanding its acute in-hospital care, it is positioned to meet ongoing demand for its products in the years ahead.

It has plenty of liquidity to invest in sales, marketing, and R&D, and as it scales it should be able to improve gross profit, margin, earnings, and cash flow.

With expectations it’s going to continue to significantly increase revenue over the next few years, I think the future of OM is strong, but in the near term it looks like it’s close to being closed at full value and investors should wait for a better entry point.

That said, I think that over time the stock will reward patient investors in a market segment that will continue to grow in the years ahead.

Be the first to comment