Andrei Akushevich/iStock via Getty Images

The current market correction is presenting some attractive opportunities for value investors who have been waiting patiently for several years for prices to reflect fundamentals. Otis Worldwide Corporation (NYSE:OTIS) is 27% off its 52-week high as of Friday’s close, and the global leader in elevators is starting to look attractive on a free cash flow basis. Before jumping in, investors will want to look at the company’s liabilities and decide if the risk is worth the reward.

Robust Cash Flow

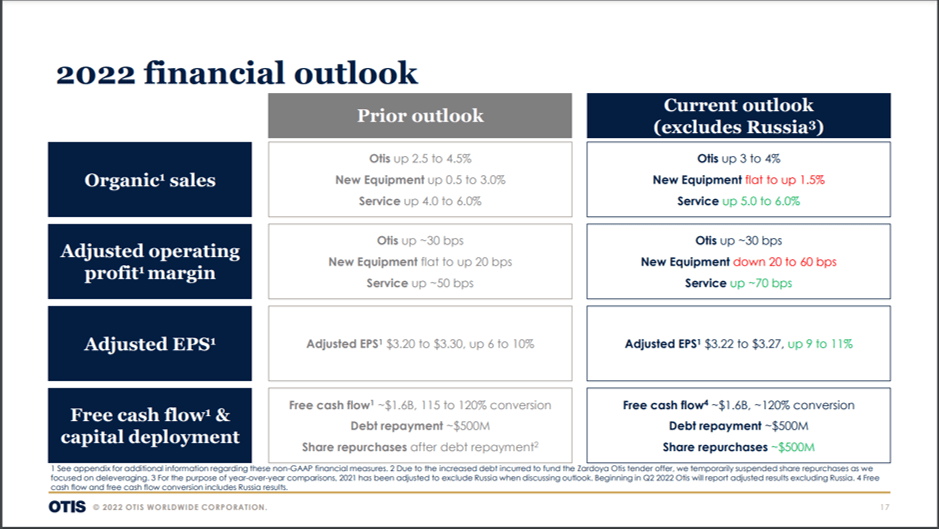

Otis recently reiterated their 2022 guidance for free cash flow of ~$1.6B and an ending diluted share count of 425M. Should the company hit their goals, that would translate to $3.75 of free cash flow per share.

Otis 2022 Guidance Delivered at International Marketing (Otis Worldwide International Marketing Presentation)

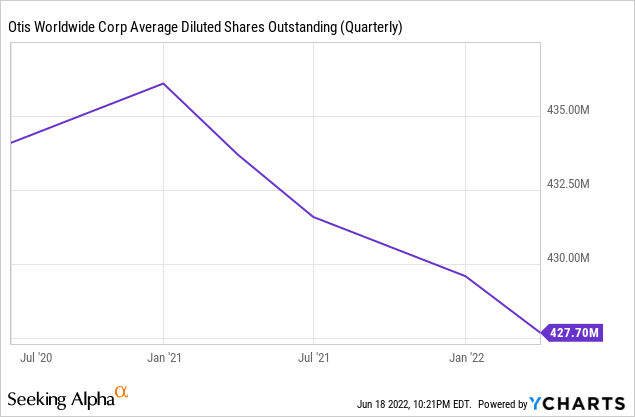

At Friday’s closing price of $67.88, that would equate to a forward price to free cash flow ratio of 18. Otis has established that share repurchases will be a priority for the company, having announced a new $1B share repurchase plan and a 2022 share repurchase target of $500MM. The average diluted share count has been reduced by 1.6% since the end of 2020, from 434.6MM shares to 427.7MM as of Q1.

Otis is also directing cash flow towards dividends, having increased the quarterly dividend by 20.8% to $0.29. The current dividend yield of 1.7% is not enough to be a draw for income investors, but there is plenty of potential for dividend growth in the future given the current dividend would represent only $493MM per year assuming they hit their projected share count at the end of the year.

Otis will also look to direct cash towards acquisitions; the company estimates that 50% of elevators are serviced by independent operators, making the market ripe for consolidation. They recently issued debt to fund the purchase of the 50% stake in Zardoya Otis that they didn’t already own. The added debt load from the acquisition caused the company to temporarily suspend their repurchase plan. A closer look at the balance sheet shows that the debt is a major hurdle that the company will have to address moving forward.

Liability Headwinds

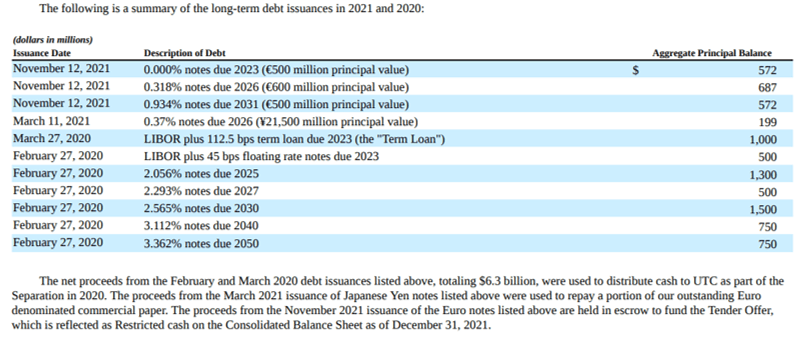

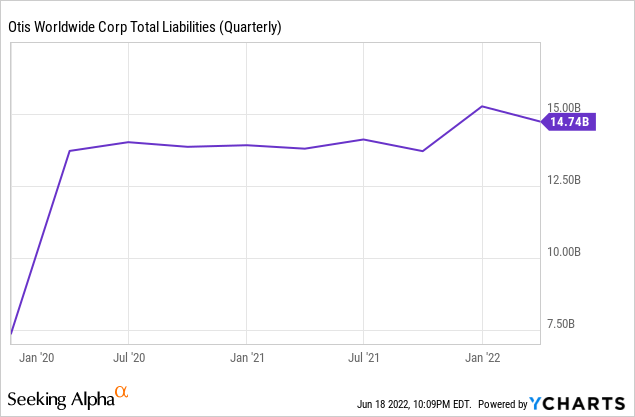

Otis was spun off From United Technologies on April 3, 2020 with a large amount of debt; the company had $14B in total liabilities at the end of 2020 Q2. After the Zardoya Otis acquisition, total liabilities stood at $14.7B at the end of Q1 versus $7.8B in current assets. The company will clearly have some work to do in the next year, as they have $2.07B in notes coming due in 2023. Rolling the debt over will be significantly more expensive, as $572MM of the liability is 0.0% yield, Euro-denominated notes.

Otis Worldwide 2021 10-K

The company generated $1.75B in operating cash flow in 2021 and they have $1.5B in revolving credit facilities to draw upon through March of 2025, making the maturing debt manageable under ordinary market conditions. Otis generated 74% of 2021 revenues from international markets, so any strengthening of the dollar could hurt their ability to pay their dollar denominated debt. Fortunately for Otis, most of their cash is generated from services that tend to be more stable during tough economic times relative to new equipment installation.

Service Business Is A Strength

Otis had $6.4B in revenue from new equipment installations in 2021 that accounted for $459MM in operating cash flow in 2021. Margins on new installations have been steadily falling in part due to the large number of units going into China, with that market representing over half of new equipment installations in 2021. Competition for new installations is fierce, with companies dropping bids to low levels in hopes of making a profit on service contracts over time.

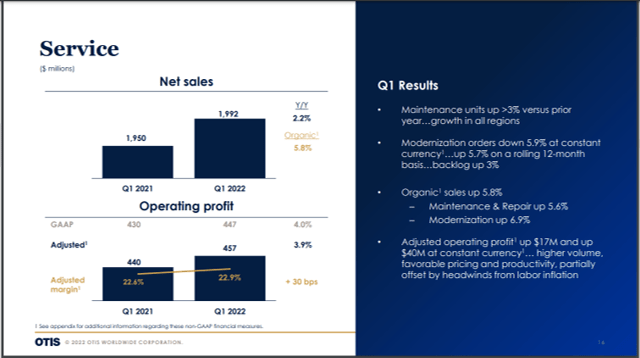

The service business generated $1.8B in operating profit on net sales of $7.9B in 2021, making it a much more appealing business than the new equipment. Otis had over 2.1 million units in their service portfolio at the end of 2021, covering a range of services from maintenance to inspections that are required by regulations. Online monitoring and analytics have reduced both customer downtime by 15% and service response time by 20% since 2019, which has helped the company to increase retention rates to 94%. With improved service, Otis hopes to increase the service portfolio to 2.6 million units by 2026. In addition to improving customer retention, the digitization push has driven margin expansion in the service segment, with the adjusted profit margin for Q1 increasing to 22.9% from 22.6% in 2021.

Otis service business update (Otis Worldwide International Marketing presentation)

A new collective bargaining agreement covering employees in the U.S. was ratified in April and will run from 2023 through 2027, adding another element of stability to the company’s short-term prospects. Overall, the company appears to be in decent shape to handle the high debt load despite unfavorable macroeconomic conditions.

Options Strategy

I like the long-term prospects of Otis and have recently sold several puts on the company. The September 16 $60 puts recently traded at $1.7, which would equate to an annualized yield of 11.7% if the options expire. Should the options be exercised, I will receive the shares at a cost basis of $58.3, which would translate to ~15.5x free cash flow based on the 2022 guidance of $1.6B. Even a 15% miss on the free cash flow guidance would still leave the valuation at a reasonable ~18.3x.

Overall, this strategy gives a good return potential, regardless of whether the option is exercised or not. Even if new installation orders dry up for a couple of years, Otis should be able to survive on the strength of their service business and continue to grow as they look to gain market share in the service business and expand margins through digitization efforts.

Be the first to comment