Kedek Creative/iStock via Getty Images

Introduction

As it has been more than four years since I last discussed OTC Markets (OTCQX:OTCM) here on Seeking Alpha, I felt an update was long overdue. Whereas the OTC and pink sheet markets had a horrible reputation earlier in the millennium, the higher tiers of the OTC markets are held in pretty high regard.

A stable performance from the existing business

For a better understanding of the company’s business model, I’d like to refer you to my old article as the bread and butter of the company used to be the “OTC Link” division which generates revenue through subscription fees and transaction-based fees payable by the brokers using the OTC Link Alternative Trading System. Additionally, the Market Data Licensing divisions also play an important role as brokers (and traders) pay monthly fees to access certain information.

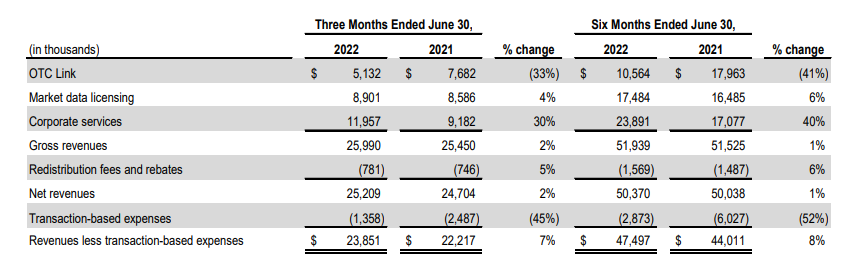

As you notice, a substantial portion of OTC’s revenues are subscription-based and thus rather sticky. The combination of OTC Link and Market Data Licensing revenue makes up just over half of the consolidated revenue, and as you can see below, the Corporate Services division made up the remaining 46%.

OTC Markets Investor Relations

As you can see above, the company’s consolidated revenue remained virtually unchanged in Q2 and in H1 in general mainly thanks to the strong revenue growth in the Corporate Services division which cancelled out the hefty revenue decrease in the OTC Link division. Expect the OTC Link revenue contribution versus the total revenue to decrease further as the recently acquired Blue Sky Data service will be included in the Market Data Licensing segment.

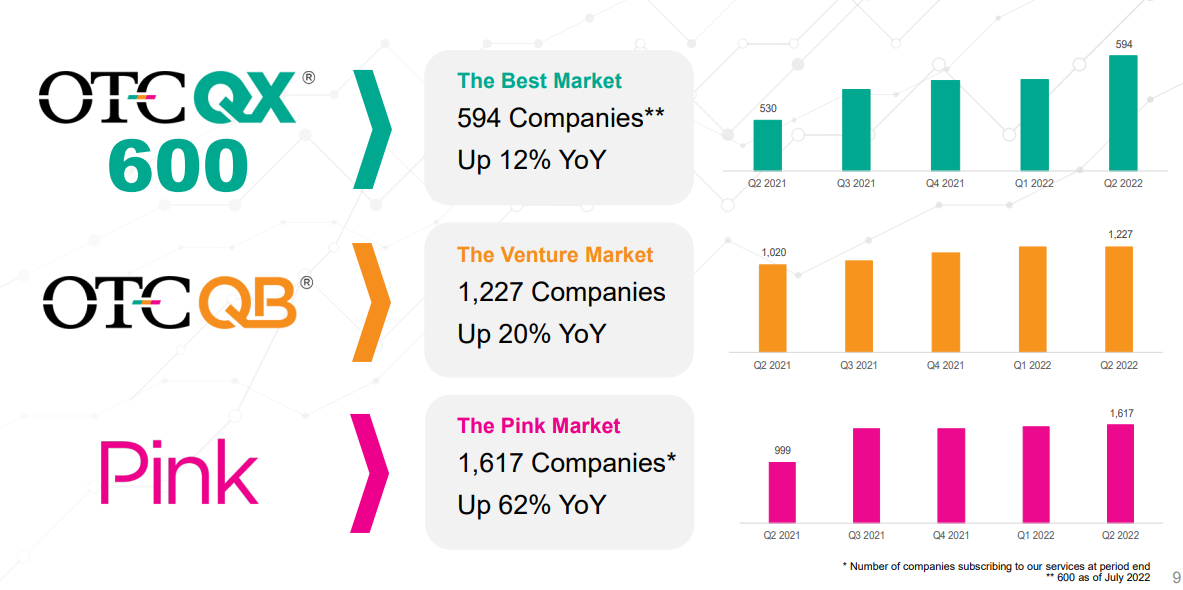

The Corporate Services growth was mainly thanks to the OTCQB and OTCQX strength thanks to very strong renewal rates and a much higher revenue generated from Disclosure and News Services.

OTC Markets Investor Relations

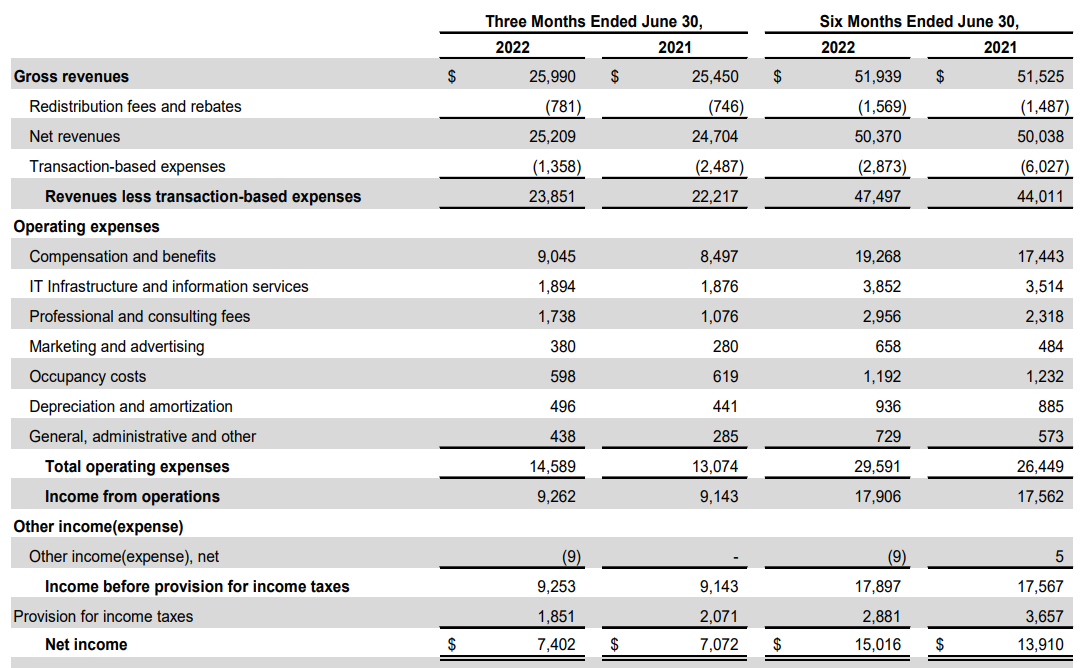

In the first half of the year, the total revenue generated by OTC Markets came in just below $52M, and after taking the redistribution fees and rebates into account and after deducting the $2.9M in transaction-based expenses, the net revenue generated by OTC Markets in the first half of this year was approximately $47.5M.

OTC Markets Investor Relations

The total operating expenses increased slightly due to higher staff and consulting expenses while the IT expenses increased by about 10% as well. The operating income came in at $17.9M which is a 2% increase compared to the first half of last year. The net income was $15M, resulting in an EPS of $1.27 per share. The 8% EPS increase was mainly caused by a lower average tax rate of just 16%. According to the company, the low average tax rate was caused by a higher excess tax benefit on stock-based compensation and we will likely see the average tax rate increase again in the next few quarters.

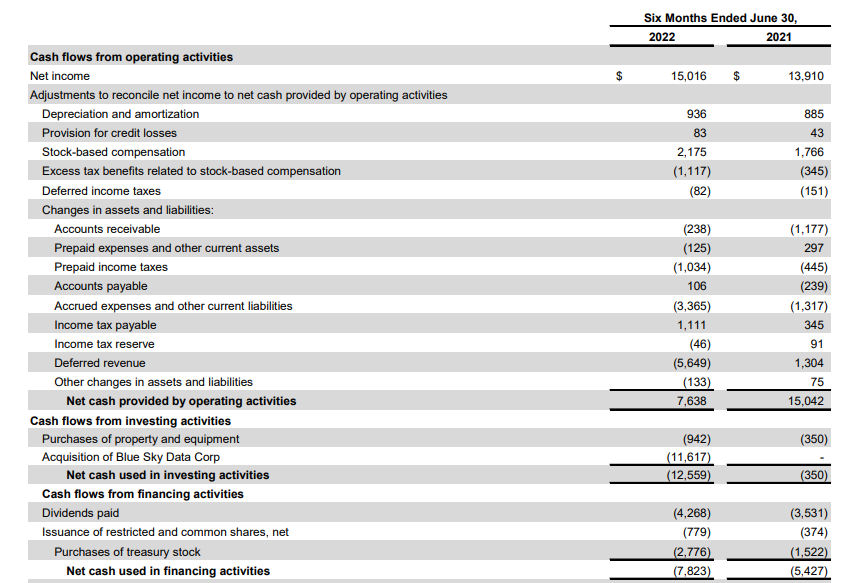

The reported cash flow result decreased compared to the first half of last year, but that was almost entirely due to a $7M shift in the deferred revenue as you can see below. Adjusting for working capital changes (excluding the deferred revenue fluctuation), OTC Markets would have reported an $11.4M operating cash flow on an adjusted basis. Adjusting this result for the deferred revenue, it would have come in at approximately $17M, a few percent higher than in the first half of last year.

OTC Markets Investor Relations

OTC Markets has always had a low-capex business model and that hasn’t changed. Its H1 capex of just under a million was almost exactly in line with the $936,000 in depreciation and amortization expenses during the first half of the year.

The acquisition of Blue Sky Data

During the second quarter, OTC Markets closed the previously-announced acquisition of Blue Sky Data, a provider of equity and debt compliance data regarding the Blue Sky rules and regulations. An interesting sidestep from “just” operating a market, but an acquisition that makes sense as it helps OTC Markets to become a one-stop shop and making life easier for its customers and clients and to avoid any regulatory issues.

On the conference call where the Q2 results were discussed, the CEO of OTC Markets also provided more background on the rationale behind the Blue Sky acquisition.

And there, there’s more compliance around being able to solicit orders. Because if you don’t comply with Blue Sky when an order is solicited, there’s this idea under securities law called “right of revocation,” which means the client can cancel the trade. And so working with Blue Sky compliance there makes it easier for these great global companies, emerging ones, to be accessible into the advisory networks of the U.S. And that leads to the debt market. And bonds have less risk of sales practice problems, but Blue Sky compliance applies to bonds as well. And the bond market, unlike the equities market, has a lot higher level of solicited order flow.

While OTC Markets, unfortunately, didn’t provide any details on the acquisition metrics and the anticipated synergy benefits, I’m looking forward to seeing a nice revenue bump in the Market Data License segment and, hopefully, that will make this $12M+ acquisition somewhat more tangible.

Investment thesis

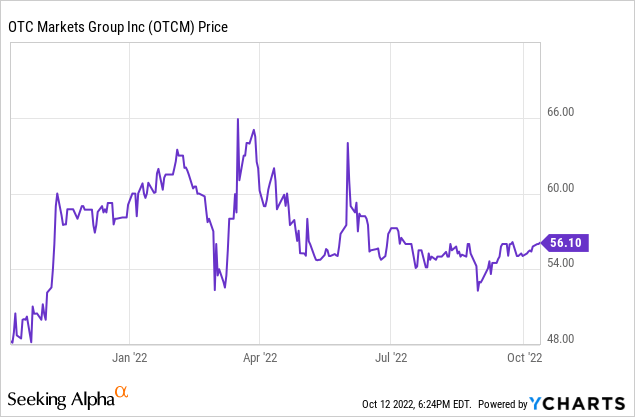

As OTC Markets is currently trading at in excess of 20 times its annualized earnings, the stock isn’t cheap anymore. The quarterly dividend has been established at $0.18 and on an annual basis, the $0.72 dividend now represents a dividend yield of less than 1.5% so OTCM likely won’t even appeal to income investors.

I’m on the sidelines.

Be the first to comment