jonathanfilskov-photography

The Danish wind energy producer Ørsted (OTCPK:DOGEF) saw an almost 4% jump in share price earlier this month when it released its full year results for 2022. Clearly, investors were happy with the numbers considering that its ADRs’ price has largely sustained at around these levels since.

Muted price makes P/E attractive

However, it hasn’t performed well in the stock markets over the past year, with a decline of 10.1%. This is in sharp contrast to the performance of the S&P 500 Global Clean Energy Index, which is up by 10.7% over the year. Interestingly, Ørsted is the eighth largest constituent in this index, which indicates that at least some other stocks have more than made up for the drag from it.

With this price performance, it follows that its price-to-earnings (P/E) at 18.6x isn’t high either. In fact, it’s lower than the 21.9x for the S&P 500 (SP500) at the moment and also lower than that for the utility sector at 20.2x. So what we have here is an ADR in a sector that’s clearly performing and its price is relatively affordable. Its recent results have gone down well with investors too. These three trends alone indicate the potential for it to rise further. The question now is whether it can reach its potential. For this, here I look more closely at its latest numbers.

Improved performance

There’s much to like in its 2022 report. A key one for its long-term future among these is actually a non-financial number. And that is the increase in the proportion of renewable energy in total energy to 91%. Even though this is a rise of just one percentage point from 2021, it is moving closer to its goal of becoming a 100% clean energy supplier by 2025. Further, it underlines how far the company has come from being a fossil fuel producer until a few decades ago.

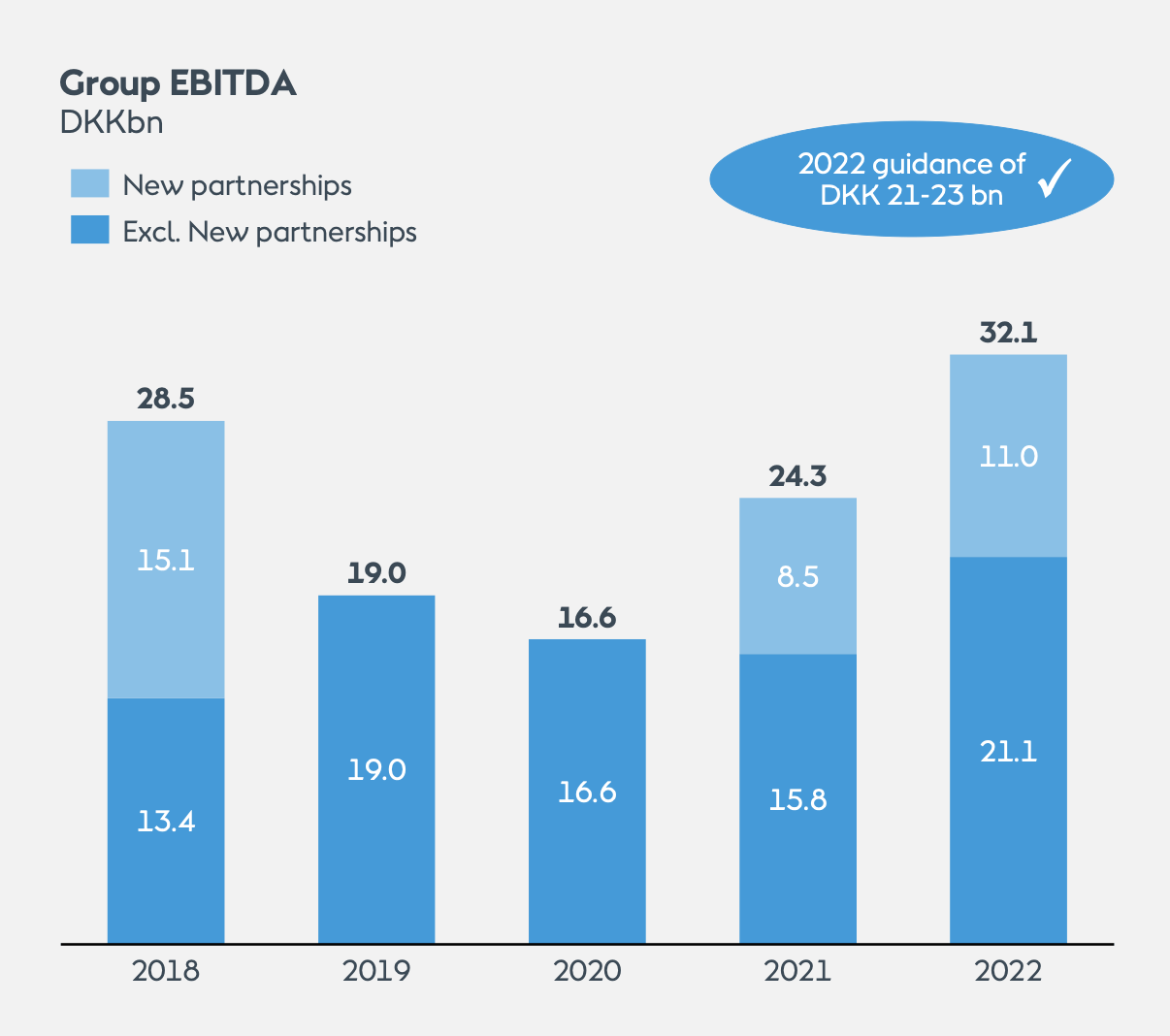

Coming to its financials, Ørsted’s EBITDA, which the company tracks closely and provides an outlook on, has come in at the highest level ever of DKK 32.1 billion in 2022, an increase of 32% year-on-year (YoY). This includes earnings from new partnerships, which it excludes from its guidance. It had an EBITDA guidance of DKK 21-23 billion for 2022, and the number ex-new partnerships has come within the range at DKK 21.1 billion. This figure too has seen a strong 33% growth.

Source: Ørsted

Efficient investing, debt in check

The other figure Ørsted provides guidance on is gross investments. The number came in at DKK 37.4 billion for the year, which is actually lower than the guidance of DKK 43-47 billion. There doesn’t seem to be an immediate explanation for why this is the case in the documents I have gone over. Nice as it would have been to know why, it’s heartening to see the progress in related numbers. It’s evident that the company is using its capital effectively as seen from a 2 percentage point improvement in the return on capital employed [ROCE] at 17% from 2021.

There has undoubtedly been a near doubling in its long-term debt in 2022 to over DKK 60 billion, which stands out when looking at its numbers. But in no way is it a red flag for the company either. The long-term debt to assets ratio is at sub-0.2x and the long-term debt to equity ratio is also at a very manageable 0.6x. Its interest coverage ratio too, is at almost 4x, indicating sufficient liquidity to pay off its interest obligations despite the increased debt.

What the guidance says

The company’s EBITDA guidance for 2023 is similar to that for 2022 at DKK 20-23 billion. This does suggest that the actual figure could come out a bit lower than what it was in the past year. But then again, 2022 was an exceptional year for energy producers as energy prices were high. Keeping that in mind, the guidance doesn’t sound bad.

It expects gross investments to rise further too, to DKK 50-54 billion in 2023. Going by its debt levels, any increase in borrowings because of this might still be reasonable considering both its assets and equity. But I am interested in seeing what it means for its ROCE, considering that its debt has already risen in the past year.

Continued growth expected

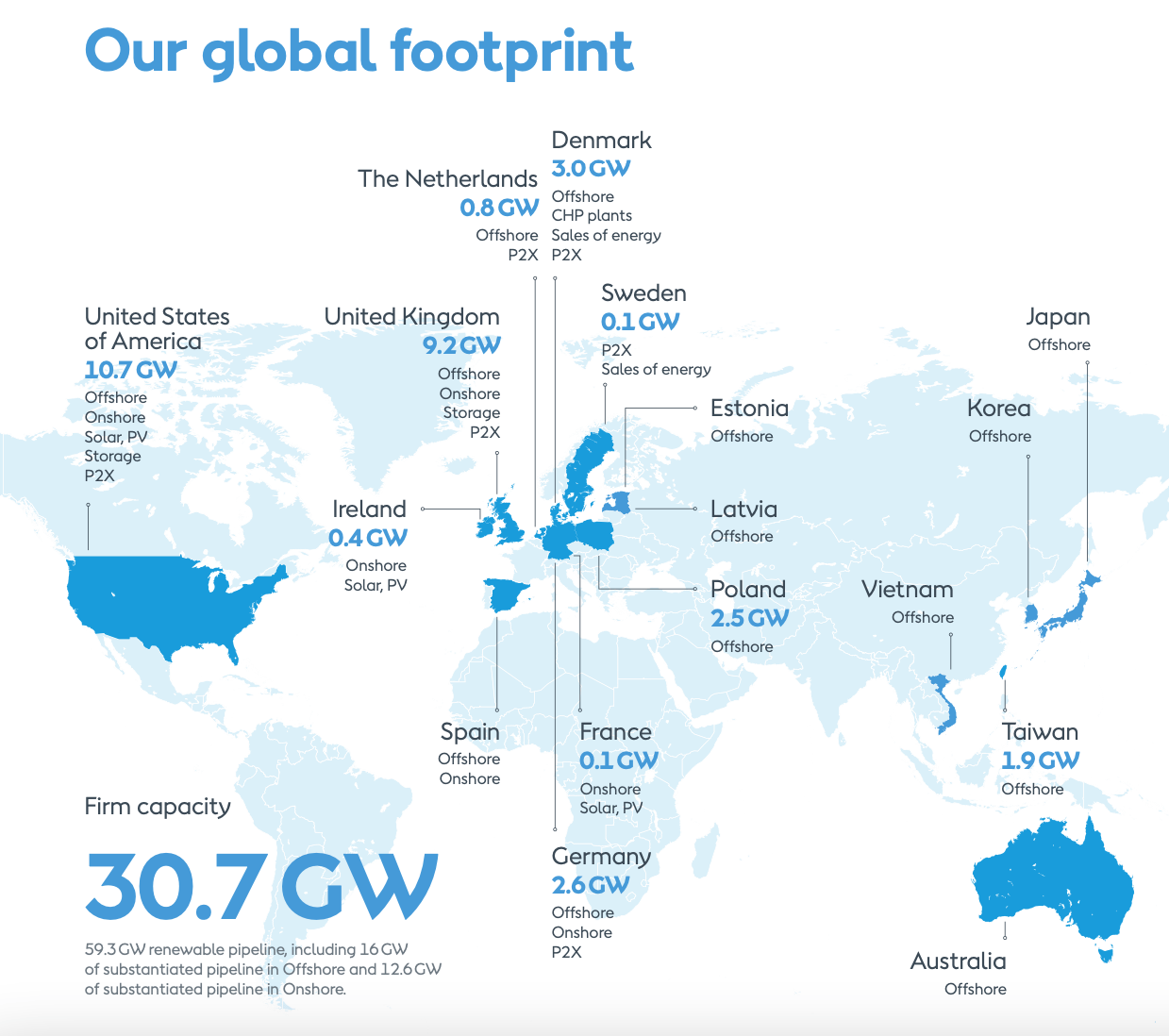

The company also has an impressive array of projects in the pipeline spanning continents and energy sources. Besides wind energy, it’s working on solar and hydrogen projects too. It’s also supported by positive policy moves. The Inflation Reduction Act in the US, for instance, can be a boost for it considering that the largest share of its energy production is in the country. It also produces a sizeable amount in the UK, where it can benefit from the government’s target to produce 50GW of offshore wind power by 2030 and decarbonise electricity by 2035.

Source: Ørsted

What next?

The Ørsted story looks good to me. It’s among the biggest wind energy producers globally, with a pipeline of projects across the world. It stands to benefit from the worldwide drive towards clean energy as the need for energy independence has become clearer than ever. And the clock is ticking on the net-zero deadline. The company’s financial performance is also encouraging in the past year.

Coming to returns on its ADRs, while it’s true that it hasn’t performed in the past year, over the past five years, its price returns still stand at almost 62% as I write. On average, roughly speaking this is more than 12% return in a year, which isn’t too bad.

It also pays a dividend. While its dividend yield at 1.96% isn’t the most lucrative ever, it has paid them consistently since 2017 which counts for something. Besides this, keeping in mind that its share price has risen over time, if I hold the investment for long enough, it’s likely that the dividend yield on my investment will rise as well, irrespective of where the current dividend yield is at.

With a relatively favourable P/E ratio, this looks like a good time to buy it from a long-term investment perspective.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment