Claudio Rampinini/iStock via Getty Images

Investment thesis

I continue to reiterate my view on Origin (NASDAQ:ORGN) as the management team has executed well on growing customer demand, construction timeline and capital budgeting thus far. The company continues to be compelling in my view as it has a long runway and is well positioned to be a solid player in the space as the global demand for clean and green substitutes grow. My investment thesis for Origin is as follows:

- The value add that Origin brings is that it has a superior proprietary platform technology that provides its customers with products that are able to maintain their performance and cost profile while meeting the net zero targets.

- The company is well ahead of competitors looking to compete in the market as Origin has developed strong barriers to entry with its patent portfolio.

- As a company that’s relatively early stage, Origin continues to see momentum in customer growth as its value proposition attracts large customers wanting to substitute their products for cleaner and greener alternatives.

- Both Origin 1 and 2 are on track and budget seems to be in line with expectations. With Origin 1 beginning operations in 2023 and Origin 2 beginning operations in 2025, Origin is progressing well toward its targets.

I have written an initial article explaining more about the technology, barriers to entry and customer list while the subsequent article provides an update about Origin’s progress in construction, commercialization and competitive analysis on the company.

Continued stellar customer demand

I think the part that I like about Origin continues to be the strong customer demand that we see today at this rather early stage of the company. Origin continues to deliver customer demand growth as the customer demand in the form of capacity reservations and off-take agreements grew 11% sequentially and 114% year on year, to $9 billion.

With this increase in the capacity reservation off-take agreements and with a sizable $9 billion in customer demand in the form of off-take agreements and capacity reservations, this does imply that Origin 1, 2 and 3 are filling up nicely.

I liked that in the earnings call, Origin management was rather transparent about which plants the recent new orders were for. In particular, management said that they were taking on orders for all three plants and the recent orders were mostly for Origin 3. Origin 2 also is almost fully booked as of the recent quarter for para-xylene and PET. In addition, the company’s sales efforts are now more focused on carbon black, advanced CMF derivatives and other high-margin products.

Additionally, in the recent quarter, Origin announced that it went into new strategic relationships with a major Japanese chemical company and a major Asian chemical company. Although details on the partnership are not released, this does seem like a material partnership given the scale of these companies.

Increasing incentives and improving regulations

While the market environment is difficult today, Origin is enjoying a strong tailwind from businesses and governments alike with their strong push toward reducing emissions and moving swiftly toward their zero carbon targets. As a result, Origin is enjoying incentives and regulations that have been put in place to accelerate the green transition and fight against climate change.

As the Inflation Reduction Act is expected to significantly expand the Section 48C Tax Credit available for investments in manufacturing facilities for clean energy technologies. The company is looking to explore possible paths of eligibility to quality for the discretionary tax credit for a large portion of Origin 2’s capital expenditures. This will definitely help with the ultimate financing for the plant if the company is able to be eligible for the tax credit.

Apart from that, Origin also stands to benefit from another of the Inflation Reduction Act’s program, and that’s the Advanced Industrial Facilities Deployment Program. This program is still being evaluated by the team at Origin but the team does seem confident about their chances of qualifying for this funding for their pilot facility in West Sacramento, for Origin 2 and other future plants in the United States. This program is under the Office of Clean Energy Demonstration that will provide $5.8 billion in competitive funding like grants, rebates, direct loans, amongst others, and it’s aimed at promoting industrial facilities that will be used to help reduce greenhouse gas emissions from traditionally energy intensive industries.

Lastly, Origin also is looking for other sources of funding from other sources other than the Inflation Reduction Act, which includes the Infrastructure Investment and Jobs Act from last year. There are more than a dozen of the Act’s initiatives that Origin has identified that could potentially help with the financing of Origin’s capital investments, particularly for Origin 2.

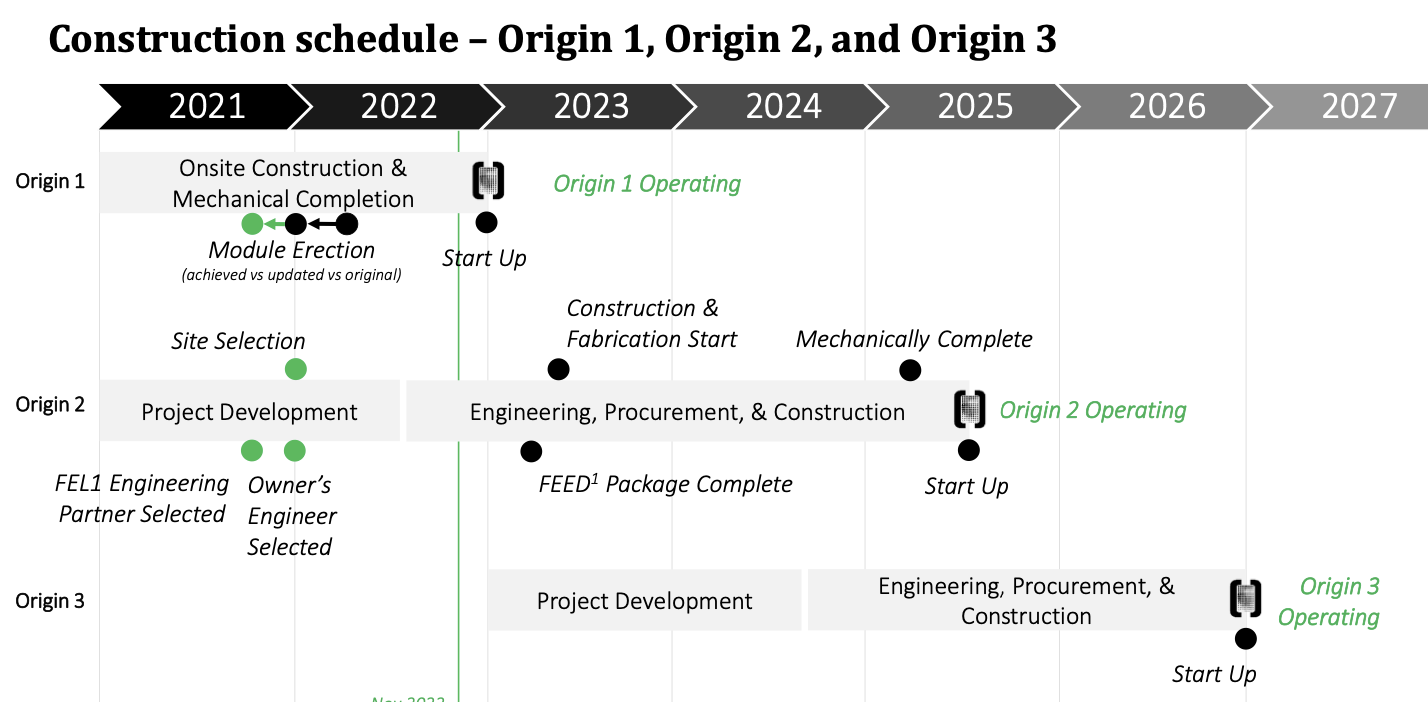

Timeline and budget for Origin 1 and 2 remain intact

Origin 1 remains on track to be completed by the end of 2022, which is going well according to the original schedule. As a result, mechanical completion will be done by then and the plant will be commissioning by the end of 1Q23 and start up shortly after. The capital budget for Origin 1 remains to be $125 million to $130 million and the plant’s major equipment has already been delivered. The piping and electrical systems are currently being assembled, most of the HTC building has been constructed and the biomass building has been completed. The HTC building is where the equipment used to separate HTC, while the biomass building is used to store sustainable wood residues.

Along similar lines, Origin 2’s budget and timeline remain intact as the company continues to progress well on the project. Currently, front end design is progressing well and detailed engineering will start soon in 2023. At the end of the day, the company continues to expect that Origin 2 will be operational by the middle of 2025.

Origin Materials construction timeline (Origin Materials IR)

Technical, operational and commercial leadership additions

The company has been in growth mode since listing and there are significant additions to the leadership team. This includes Dr. Zan Liu, who joins Origin as a Technical Manager, who invented an award-winning technology C5 CDALky. This technology won the 2019 Hydrocarbon Casting Award, which goes to show how accomplished a research scientist Dr. Zan Liu is. He will likely add value to the technical expertise of the team.

An addition that will likely help with operational expertise of the team is Matt Perkins, who was hired as Origin’s Engineering Director for Capital Projects. He has experience working for more than 20 years in project execution and is experienced in designing, procuring and constructing industrial assets.

Another addition was Dr. Bill Williams, who was hired as Origin’s Director of Process Development for Carbon products. As an expert in applications for Caron black and chemical process engineering, he has developed technologies that has helped to improve carbon efficiency, reduce carbon dioxide, and capture carbon emissions, amongst others.

Another two new additions that will add to Origin’s technical expertise includes Dr. Jay Hanan and Dr. Ron Moffit, hired as Origin’s Technical Director and Polymer Principal Scientist respectively. Jay has almost 300 patents and more than 300 publications while Ron has more than 38 years of experience in polymer research.

These new additions signal a growth in the human capital and talent needed to ensure that Origin is able to continue to execute well and also shows the strong brand recognition that enables talent to be joining Origin.

Other key updates

With the current cash on hand of $362 million, management reiterates that this is more than sufficient to fully fund Origin 1 and 2 based on their current estimates.

In addition, Origin continues to show strength in research and development as it recently increased its patent count to 23 and continues to be focused on patent development. This is an example of how its new technical talent has been value adding to the research and development efforts of the firm.

Valuation

I continue to use DCF to derive my one-year target for Origin. Given that current news and earnings information suggest that Origin is progressing well in its construction and operational schedule, I maintain my 2025 revenues at $440 million. As my financial projections incorporate only estimates for Origin 1, 2 and 3, my forecasts go beyond 2025 until 2030. Based on the expected 80% CAGR from 2025 to 2030, I made an assumption of 3x EV/Sales multiple for Origin. I applied a slightly higher discount rate, increasing it by 1 percentage point due to the rising rates environment.

As a result, my target price for Origin is $10.94, implying an upside of 137% from current levels.

Risks

Execution risks

While I think that Origin’s team has been executing well, the challenge remains to be the actual operations and production ramp as Origin 1 starts operations. There’s the risk that while the construction of Origin 2 and 3 may be delayed or the budget exceeded. The key challenge will be the production yield and productivity as the plants go live and ramp up. Investors will need to see that Origin is able to not just construct well but also produce and ramp up well.

Risk of delays

With more moving parts as Origin 1 goes live and Origin 2 construction begins, there are risks that the timeline of projects may be delayed. Given that the contracts with their key customers for all the Origin plants are subject to Origin actually meeting construction deadlines and commencing operations at the plants, the company needs to make sure that its meeting deadlines and target to ensure that the company continues to give customers the confidence in Origin’s abilities to execute.

Risks from concentration

At the beginning, a small number of large customers will dominate Origin’s reservations and off-take agreements. However, over time, the concentration risk will be reduced as the company brings in more customers. These early large customers are crucial in helping fill up Origin’s initial plants and bring the needed confidence from other potential customers.

Competitive pressures

Origin continues to execute well by bringing an innovative product to a world in need of a sustainable alternative. However, there are many other competitors, large chemical companies and new startups alike, that look to bring sustainable alternatives that may challenge Origin’s competitive positioning.

Conclusion

Origin continues to execute well in a difficult market today. Even with an inflationary environment, Origin has been able to maintain its construction timeline and budgets, demonstrating the quality of the team managing the construction of Origin 1 and 2. In addition, the strong customer demand is something that I continue to admire as customers continue to fill up Origin 1, 2 and 3 as this brings further prove that Origin’s offerings are able to bring to customers an alternative that helps them achieve their net zero targets while bringing similar performance and cost profiles. Lastly, regulation and incentives continue to provide tailwinds for Origin while the company continues to add new talent to accelerate growth. My target price for Origin is $10.94, implying an upside of 137% from current levels.

Author’s note: I am starting a marketplace service, Outperforming the Market, which will be launching on 10 Jan 2023. Outperforming the Market aims to help investors identify high conviction growth and value stocks to form a barbell portfolio that outperforms the market.

Mark your calendars, because early subscribers can reserve a spot as a Legacy Discount Member, which gives you generous introductory prices. Thank you for reading and following my work. See you there!

Be the first to comment