SergeyZavalnyuk

Since January 2022, I have written several bearish takes on the steel making leaders in America, including Cleveland-Cliffs (CLF) and United States Steel (X). The two have horrible track records for shareholder performance during past recessions. If we can avoid a recession this year, I would expect performance ranging from slight gains to minor declines from them. However, assuming a serious recession is next, both could crater as last year’s earnings morph into sizable operating losses. I know many investors and analysts believe late 2021’s U.S. infrastructure deal, plus rebounding demand from the auto manufacturing industry, alongside China’s reopening from COVID will keep steel/iron ore prices elevated.

I tend to disagree. Housing starts and construction outside of government-directed projects are entering a steep decline from sharply higher interest rates. A big drop in demand for new products from all types of transportation businesses usually follows a recession. And, spreading recessionary forces globally could more than offset new orders for road, dam, utility, airport, etc. projects in America.

Another problem child in the steel industry during a recession will likely be Mesabi Trust (NYSE:MSB). The trust collects royalties from iron ore commodity production in Minnesota. I remember holding a bunch of it during the 1987 stock market crash, when iron prices were low, the trust was depressed with almost no revenue, and the unit price was $1.50.

Today’s setup is kind of the opposite of 1987. Iron prices are relatively high with plenty of room to decline in recession. More importantly, the trust price is ignoring an implosion in revenue. It’s main customer, the Northshore Mining division of Cleveland-Cliffs has stopped production since the middle of 2022.

Adding insult to injury, the trust is disputing past payments through arbitration, and no concrete date has been set for the resumption of operations and royalty payments. As a consequence, next to zero royalty payments are expected for the time being, and Mesabi may have to find a way out of the current agreement to resume some sort of revenue flow.

Below is a link to Mesabi’s January 12th, 2023 press release describing the operating mess,

The Trustees of Mesabi Trust have determined that no distribution will be declared this January 2023 with respect to Units of Beneficial Interest. This compares to a distribution of One Dollar and seventy-five cents ($1.75) per Unit for the same period last year.

The Trustees’ announcement today of declaring no distribution this quarter primarily reflects the Trustees’ caution about uncertainties arising from the July 22, 2022 announcement by Cleveland-Cliffs Inc. (“Cliffs”), the parent company of Northshore Mining Company (“Northshore”), to extend the ongoing idling of Northshore operations until at least April 2023 and maybe beyond. With Northshore’s operations currently in idle mode, and no additional information being made available to the Trustees regarding the length of the idling, the Trustees’ decision reflects their determination to maintain an appropriate level of reserves in order to make adequate provision to meet current and future expenses and present and future liabilities (whether fixed or contingent) that may arise in the future.

The Trustees have received no specific updates on Cliffs’ plans concerning Northshore operations. The Trustees’ determination of no distribution this quarter also takes into account numerous other factors, including uncertainties resulting from Cliffs’ prior announcements to make Northshore a swing operation as Cliffs’ Minorca operation becomes increasingly utilized, Cliffs’ increased use of scrap iron in its vertical supply chain planning, potential volatility in the iron ore and steel industries generally, national and global economic uncertainties, the cost and expense related to the Trust’s initiation of arbitration against Northshore and its parent, Cliffs, possible further disturbances from global unrest and the potential impacts from further outbreaks of the coronavirus (COVID-19) pandemic.

Quarterly royalty payments from Northshore for iron ore production and shipments during the fourth calendar quarter, which are payable to Mesabi Trust under the royalty agreement, are due January 30, 2023, together with the quarterly royalty report. After receiving the quarterly royalty report, Mesabi Trust plans to file a summary of the quarterly royalty report with the Securities and Exchange Commission in a Current Report on Form 8-K.

Commencement of Arbitration

As previously disclosed by Mesabi Trust, on October 14, 2022, the Trust initiated arbitration against Northshore and its parent, Cliffs (jointly, the “Operator”), the lessee/operator of the leased lands. The arbitration proceeding was commenced with the American Arbitration Association. The Trust seeks an award of damages relating to the Operator’s underpayment of royalties in 2020, 2021, and 2022 by virtue of the Operator’s failure to use the highest price arm’s length iron ore pellet sale from the preceding four quarters in pricing internal production during the fourth quarter of 2020 through 2022. The Trust also seeks declaratory relief related to the Trust’s entitlement to certain documentation and to the time the Operator’s royalty obligation accrues on internal production.

For a lengthy explanation of the frayed relationship between Cleveland-Cliffs and Mesabi Trust, I recommend reading the August 2022 article here posted by Seeking Alpha contributor Nat Stewart, around the time Northshore ceased mining the Peter Mitchell resource.

Financial Review

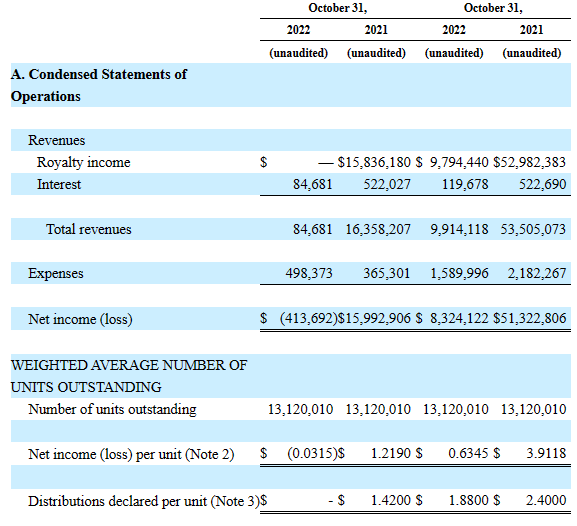

With an equity market capitalization of $313 million at $24 per trust unit, there’s not much backing up your purchase over the short run, until royalty revenue reappears. Below is a table taken from the October 10-Q filing, which is the new normal. Not much for revenue, operating losses, and no dividends paid.

Mesabi Trust 10-Q for October 2022 Period

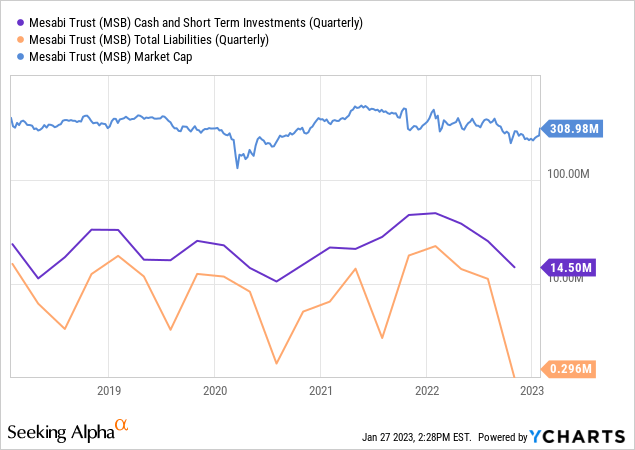

Below is a review of total trust market cap to cash holdings and total liabilities. Sure, the trust has enough net cash to stay in business for years, with dividends cut to zero. However, what is Mesabi worth in its current condition?

YCharts – Mesabi Trust, Cash vs. Total Liabilities, 5 Years

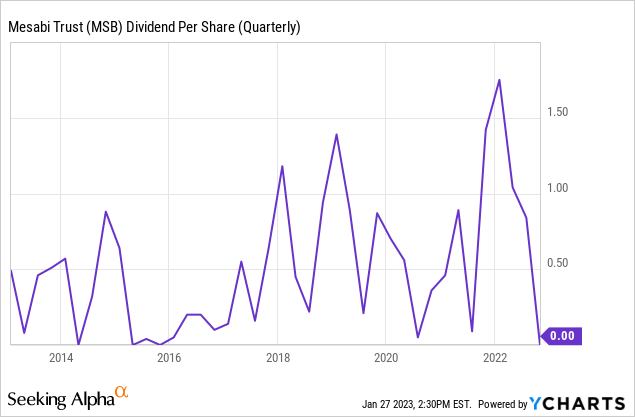

2015 was the last time no or limited dividends were paid, drawn below.

YCharts – Mesabi Trust, Quarterly Dividends, 10 Years

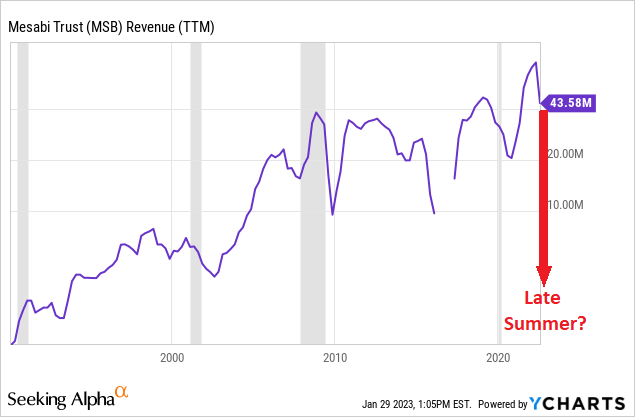

And, if royalty revenue approaches zero another few quarters, it will be the weakest trailing annual showing since 2002, twenty years ago.

YCharts – Mesabi Trust, Trailing Annual Revenues, Since 1990

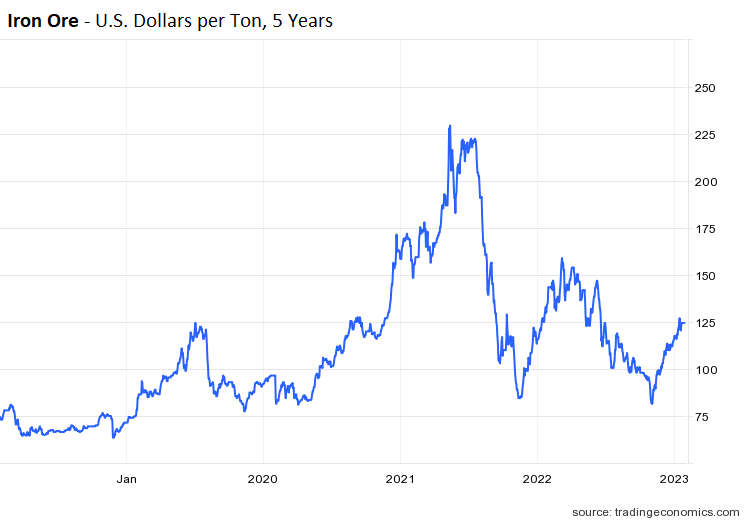

Iron Ore Prices – Mesabi Recession Returns

So, Mesabi owners have limited cash on hand, no revenues, no dividends, and an uncertain outlook. But that’s not all the bad news. Iron prices could decline swiftly in a deep recession, pushing the odds of new royalty revenue far into 2024 or 2025 if Cleveland-Cliffs is unmotivated to resume mining.

Current iron ore prices are -45% lower than the May 2021 peak and could fall under October’s 2-year low in a serious recession. At that point, even if royalty dollars are reestablished, revenue totals will be far weaker than early 2022 or all of 2021. I am estimating a best-case earnings rate of $1.50 per trust unit in a recession, with Northshore operating again, and iron ore around $75 per ton.

TradingEconomics.com – Iron Ore Prices, US Dollars per Ton, 5 Years

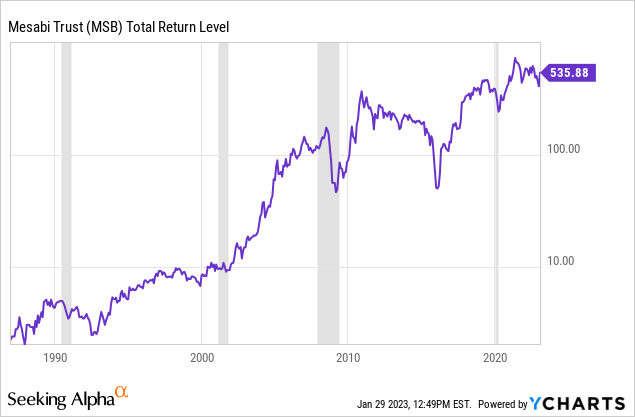

I want to bring your attention to two things on the long-term total return chart below for Mesabi since 1987. The first is performance stinks during recessions. I have shaded 4 recessions in grey over the last 35 years, 1990-91, 2001-02, 2008-09, and 2020. Each time MSB’s price has declined, measured from the beginning to the end of official contractions in real GDP output.

YCharts – Mesabi Trust, Total Return Level Since 1987, Starting Value of 1

The second point is my small personal 1987 position (which I sold in 1988 for a minor gain) would have generated a total return (including dividends) of 535x my money. That’s not a typo. Buying a hard asset shunned for years and valued as if things would never change for the better (1987’s background story) is a great way to bargain-hunt your portfolio to riches. $1000 invested in 1987 would have netted $535,000 (excluding taxes) 35 years later, good for +19.5% compounded annually! So, if you want to buy Mesabi, waiting for a recession dip could prove a productive pursuit.

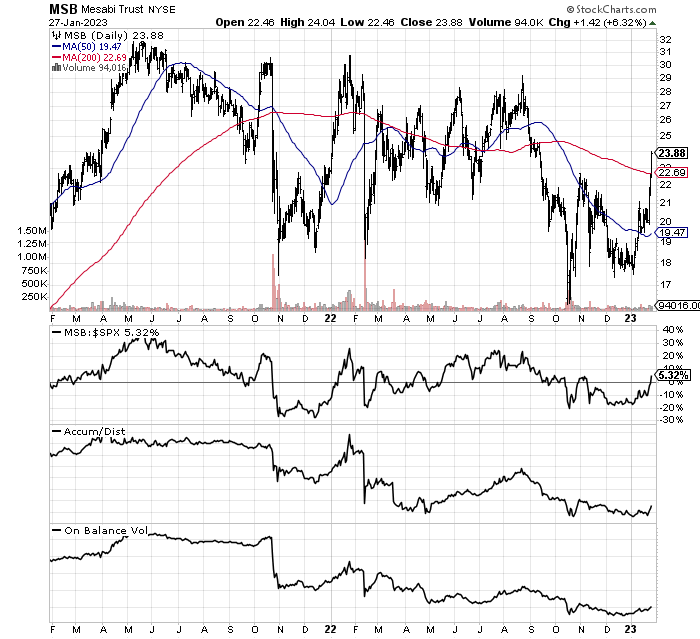

Technical Trading Chart

The chart pattern and momentum indicators I follow are neutral to bearish across the board, as you would expect. Below I have drawn an 18-month chart of daily price and volume changes. The chart is dividend-adjusted to show a true picture of total returns, both price changes and dividends received. The unadjusted trust quote peaked around $38 ($32 on the chart) in May of 2021 with iron ore prices.

Today, iron commodity prices are down -45% from May 2021, and Mesabi has been a significant “underperformer” vs. the S&P 500 from that point. The Accumulation/Distribution Line and On Balance Volume readings have been in rotten downtrends, not recovering at all during the January bounce in price.

My read of the situation is this rally should be sold, and Mesabi avoided until more clarity appears in the chart and business outlook.

StockCharts.com – Mesabi Trust, 2 Years of Daily Price & Volume Changes

Final Thoughts

Is Mesabi worth the same price as January 1st 2022, when iron prices were higher, royalty revenue was streaming in the door, and a strong dividend payout was being made to trust owners? My answer is NO. To me, until all the operating uncertainties are successfully resolved and an economic recovery appears AFTER a recession (it’s coming according to the massively inverted Treasury yield curve), I am willing to pay only half of the current market quote of $24.

I would use the January 2023 strength in price to sell any position, and wait patiently for lower prices, perhaps under $15. I sincerely believe upside is very limited. Outside of a take private acquisition or merger offer, price gains above $30 have very weak odds of playing out this year.

My risk/reward analysis review is downside potential during a deep recession could be at least $12 per unit or -50%. The upside argument is Northshore will resume production this summer, and Mesabi’s price will return to $30, of course also assuming no recession appears this year to drag down iron ore quotes. This optimistic scenario would bring a +25% gain.

Given all the pros and cons, I rate the trust a Sell or Avoid selection in January around $24. My view could change at far lower trust prices, but not until then. If you want to purchase or add to your position, waiting for a better entry is suggested.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Be the first to comment