Opendoor’s (NASDAQ:OPEN) stock tanked by ~26% last week after a report (released on Monday, 19th September 2022) revealed that the iBuyer lost money on 42% of its transactions in August 2022. While this headline figure doesn’t express the quantum of losses or take into account Opendoor’s service fees and selling-related expenses, investors seem to be spooked. As of Q2, Opendoor held an inventory of 17K homes ($6.6B), and a drastic drop in house prices has market participants worried about massive transaction losses and inventory markdowns. However, if you have been following my work on Opendoor, this is something we discussed back in early August:

The biggest fears around Opendoor are potential transaction losses and inventory writedowns. While these fears are justified to some extent due to the nascency of the iBuying model, Opendoor’s management guiding for positive contribution margins in the face of a violent contraction in home prices is a conviction booster. Some (mark-to-market) inventory writedowns may happen in Q3, and this figure could be as large as 8-10% of the $6.6B of housing inventory Opendoor is holding on its balance sheet. As a market-maker, Opendoor will continue to buy and sell homes in up or down markets.

Now, I do think that Opendoor could end up missing its Q3 guidance for sales and profitability (loss) if the macroeconomic conditions were to worsen further. However, mortgage rates have been moderating recently, the job numbers are coming in stronger than expected (record low unemployment of 3.5%), wage increases are looking robust, and the housing supply remains constrained.

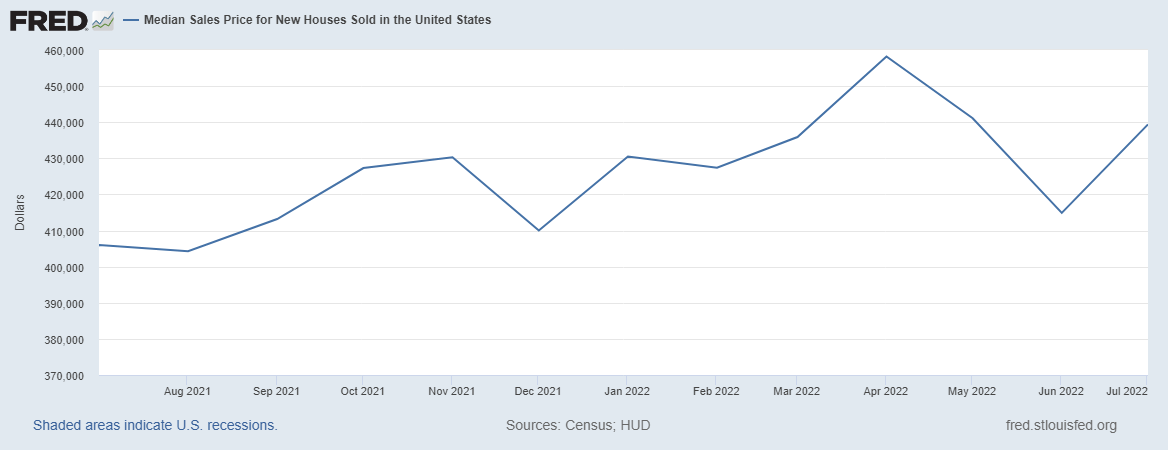

In the note linked above, I shared some macroeconomic data and charts to explain my view on the upcoming business volatility at Opendoor in Q3 and Q4. For brevity, I will not repeat those ideas today, but I do want to share a couple of housing price charts with you.

We know that ‘Existing Home Sales Prices’ are less volatile and lag ‘New Home Sales Prices’ by around 30-60 days. In my last note, I shared that ‘New Home Sales Prices’ had collapsed by 16% between April to June, and now we are seeing a ~6% contraction in ‘Existing Home Sales Prices’ from June to August. If you remember, Opendoor’s management said that they started increasing spreads rapidly in May 2022 during the Q2 earnings call. Hence, the quantum of losses that Opendoor will suffer in Q3 is unlikely to be more than ~5-10%. I am expecting this loss figure to be higher than the median price contraction because Opendoor is significantly concentrated in metro areas, where the price declines are deeper (~10-20%+).

FRED

Well, that’s backward-looking data that will impact Q3 numbers; however, what about Q4 and beyond?

As I see it, the housing market is readjusting prices for the movement in mortgage rates. Here’s what I said in the conclusion of my last note:

Opendoor’s financial performance is set to bear the brunt of a challenging macroeconomic environment. While ultra-low housing affordability (as measured by median home price to income ratio) is leading to widespread fears of a GFC-like housing market crash (2008-12), housing inventory remains near record low levels (unlike 2005-08), and new housing supply is getting constrained further due to rising interest rates (builders pulling back).

In my view, the housing market needs some normalization, but that may not result in a big peak to trough crash in US home prices. A multi-year stagnation is a more likely outcome under current circumstances, but if we were to see a correction in home prices, it will be a slow burn lower from here. After the initial shock is navigated, Opendoor should be able to deliver solid unit economics and sales growth even during a buyers’ market in residential real estate. Opendoor’s partnership with Zillow is truly a game changer and a clear indication of Opendoor’s potential to be a generational company. While I think we are in for a couple of bumpy quarters, Opendoor has ample liquidity to get through this turbulent period (most of its rivals won’t). Opendoor is already the undisputed leader in iBuying, and a few quarters from now, it could be the only scaled player left standing. Hence, I am holding tight onto my Opendoor shares, and I will continue to add opportunistically in the near future.

After this initial price shock is digested, the decline in existing home sales prices is likely to be a slow burn lower due to continued supply shortages, increased rents, and rising wages. Interestingly, ‘New Home Sales Prices’ rebounded sharply in July despite higher mortgage rates.

FRED

If the relationship holds up, ‘Existing Home Sales Prices’ could rebound higher in September or October. And that’s good news (more minor losses) for Opendoor’s Q4 results! While the concerns around Opendoor’s transactional losses and inventory markdowns are warranted, the panic selling in Opendoor’s stock is outright stupid. At $3 per share ($1.9B market cap), Opendoor is trading below its net cash balance of $2.2B. Mr. Market is acting like a depressed maniac in selling Opendoor as if it is a worthless entity set to go bankrupt. However, my analysis suggests that Opendoor has ample liquidity to survive this downturn and emerge as a monopoly on the other side of this market cycle.

In the rest of this note, we will analyze Opendoor’s business fundamentals, balance sheet (in the context of potential cash burn & inventory markdowns), and technicals.

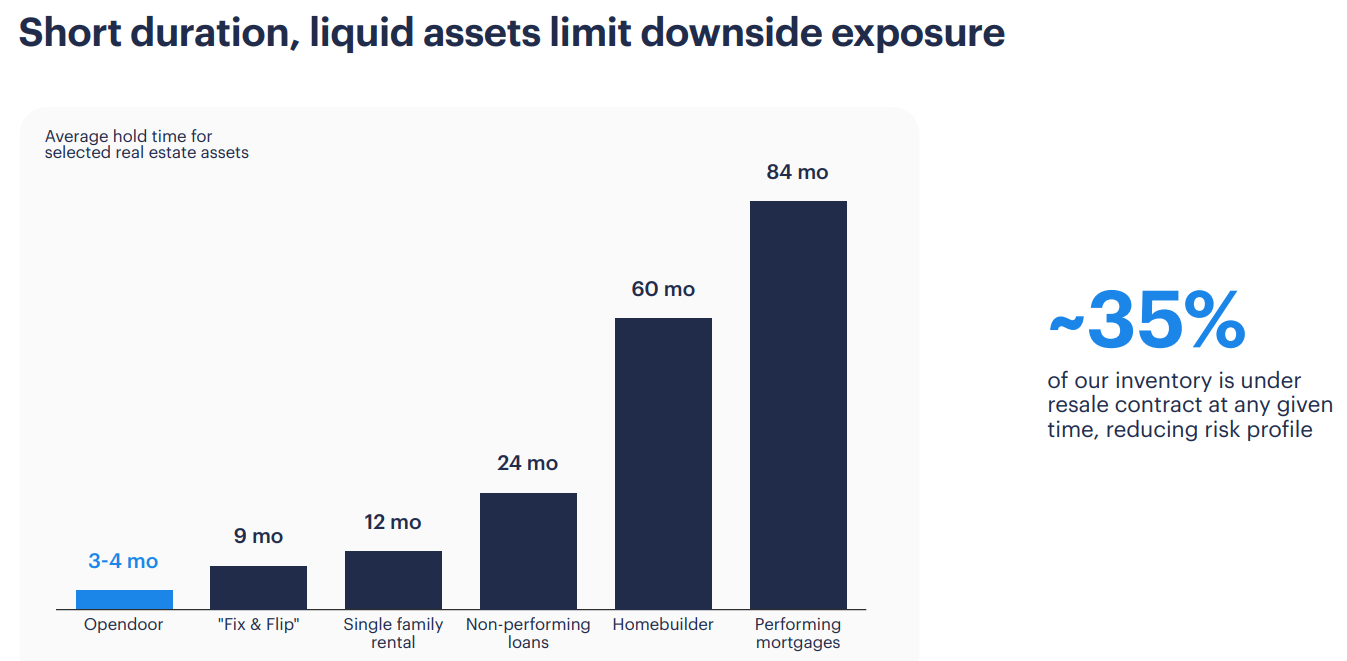

Opendoor Is A Market-Maker, Not A Home Flipper

On a rudimentary level, Opendoor buys and sells homes, which is also what a home-flipper does; however, unlike flippers, Opendoor is disrupting real estate through its consumer-centric, tech-enabled home buying, selling, and trading marketplace that provides fully-digital, superior consumer experiences at lower costs. The traditional real estate transaction is expensive, time-consuming, and complicated. By creating a two-sided marketplace for homesellers and homebuyers, Opendoor is streamlining the process of selling and buying homes for consumers through digitization. On the seller side of its platform, Opendoor gives consumers ease, speed, and certainty when selling their homes in exchange for a 5% service fee and a ~5-15% variable spread (dependent on factors such as HPA environment, holding periods, and interest rates) that’s built into the offer price. On the buyer side of its platform, Opendoor sells homes at fair market value (after making light repairs or none at all [unlike flippers]) and offers homebuyers a smooth digital transaction process with ancillary services such as Opendoor-Backed Offers (financing), home loans, and title & escrow [future ancillary services: home warranty, upgrade & remodel, home insurance, and moving]. In addition to disparate solutions for selling and buying homes, Opendoor Complete combines the entire selling and buying process in a single transaction, yielding cost savings and increased flexibility.

While the transactional nature of its business makes Opendoor look like a home-flipper, the central idea of Opendoor’s operations is to provide consumers with digital services and financial solutions (liquidity) in exchange for fees. Despite Opendoor’s balance sheet structure and inventory of 17K homes making it look like a levered, directional bet on the real estate market, Opendoor is a real estate market-maker, not a home-flipper.

Opendoor Investor Presentation

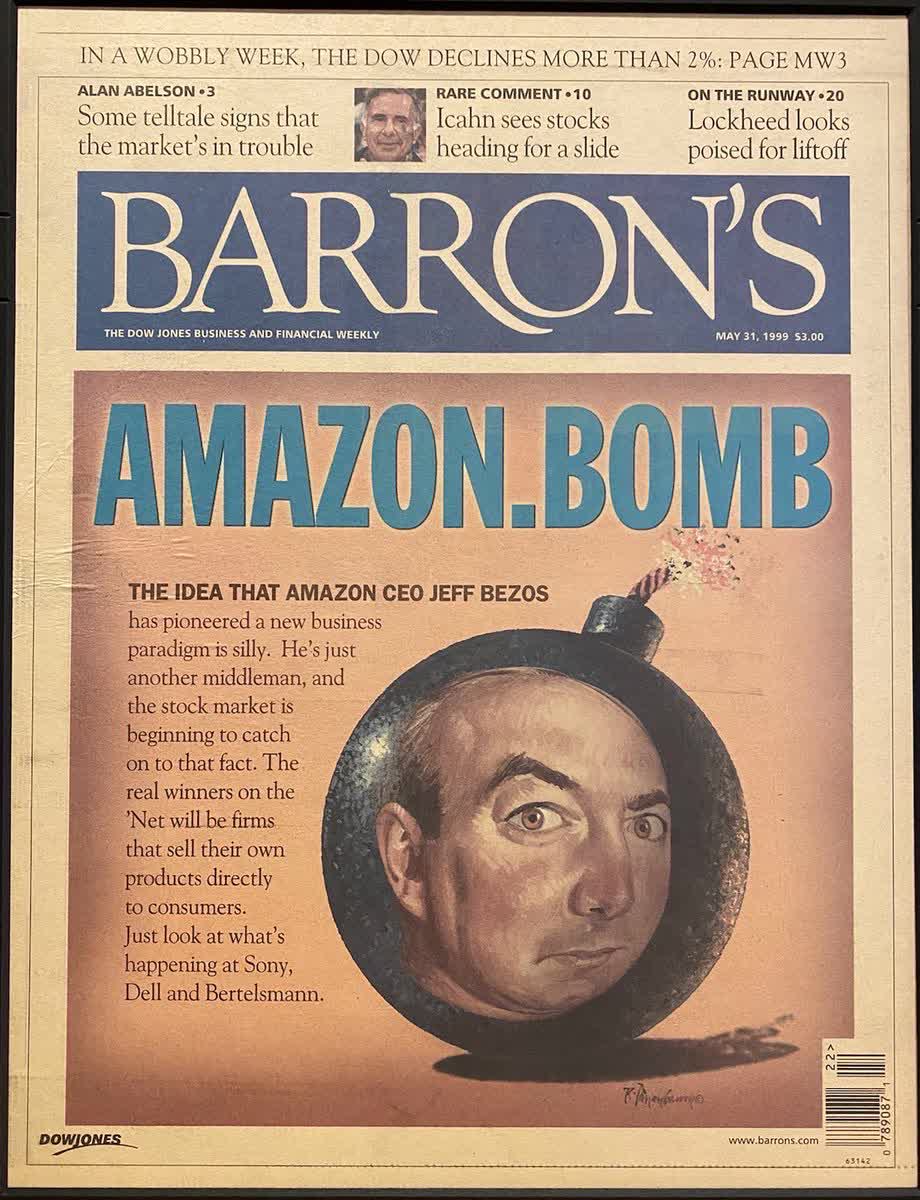

Opendoor is still in the early stages of its journey of transforming real estate; however, critics and bears (primarily real estate agents and home-flippers) are dismissing the iBuyer as an impending bankruptcy. History shows that disruption often faces resistance from incumbents and laws of inertia. And I strongly believe that Opendoor is building the way future generations will transact real estate 10, 20, and 50 years from now. In a bear market, investors are surrounded by fear, uncertainty, and doubt spread by news media. For example, Amazon (AMZN) was called a dot bomb in 1999, and you know the history.

Barron’s

All great disruptive companies [be it Amazon or Apple (AAPL) or Tesla (TSLA) or Google (GOOG) (GOOGL)] have faced criticism during their formative years, and it is only with time that these companies have won over Wall Street and Main Street investors. Remember, Tesla was priced for bankruptcy for years before 2019. Now, I am not saying Opendoor is the next Amazon or Tesla; I am just trying to highlight that as an emerging disruptive force in an archaic industry, Opendoor will get a lot of negative press coverage and bearish views in a period of temporary weakness.

Today, Opendoor is holding an inventory of ~17K homes, and with a rapid decline in home prices during the last two months, it is probably underwater on thousands of homes. As a market-maker, Opendoor will continue to sell homes in this market (adjusting prices lower and taking losses), but it is important to understand that it will acquire more homes too. In coming months, we will likely see a lot of FUD around Opendoor’s operations in the news media; however, as investors (and believers in Opendoor’s mission and vision), all we need to focus on during these uncertain times are unit-level economics and operational efficiency. Over the long run, I see Opendoor evolving from a 1P marketplace to a 3P marketplace akin to Amazon, and such a shift will lead to higher margins and lower balance sheet risk. However, this vision is probably 5-10+ years away from materializing.

For Q3 2022, Opendoor’s management guided for revenues of $2.2-2.6B (much lower than Street estimates of ~$4.2B) and contribution margins of +1.9%. Since the decline in home prices during July-August has been worse than the worst quarter in the Great Financial Crisis period, I think Opendoor will end up missing on its CM guide. However, after digesting this initial shock over the next few quarters, Opendoor should be able to resume operating at management’s guardrails of 4-6% contribution margins by H2-2023.

Opendoor’s Q2 Shareholder Letter

Over the last five years, Opendoor’s unit economics, as expressed by contribution margins, have been positive and trending higher. During the first half of 2022, Opendoor was operating close to breakeven on a net income basis (positive operational cash flow). In the near term, Opendoor’s contribution margin is likely to turn negative, but this inflection would be temporary, and post-normalization of housing markets, Opendoor will likely operate at positive contribution margins (even during a slow burn lower in the housing market).

While most bears believe that Opendoor’s positive contribution margins are solely driven by home price appreciation, I believe that the value proposition of Opendoor’s seller product is greater during a bear market (declining price environment) in the housing market, which means the company can charge a higher spread to offset increased operating expenses.

For the last 15 years, the Fed’s low-interest rate policy (ZIRP) and low housing supply have propelled a massive bull market in real estate. Housing is an absolute necessity for humans, but current affordability (as measured by median home price to median annual income) is worse than in 2007 (the peak of the housing bubble). While housing supply remains tight, Fed’s ongoing quantitative tightening program is set to drive a moderation [reset in Jerome Powell’s words] in housing prices. The big question is – “Can Opendoor survive a GFC-like bear market in housing?”

Assessing Opendoor’s liquidity situation

Opendoor’s business model is built to survive and thrive across market cycles, and this notion is being put to the test as we speak due to an unprecedented decline in the housing market. Now, I understand and agree with the bearish argument/premise – “Opendoor is set to record big transactional losses in the upcoming quarter[s] accompanied with inventory markdowns”.

Well, I knew (and shared) this would happen back in early August; however, I am investing in Opendoor with an ultra-long time horizon, and I think Opendoor has ample liquidity to survive this downturn in housing.

Here’s what I said back in August when describing Opendoor’s balance sheet:

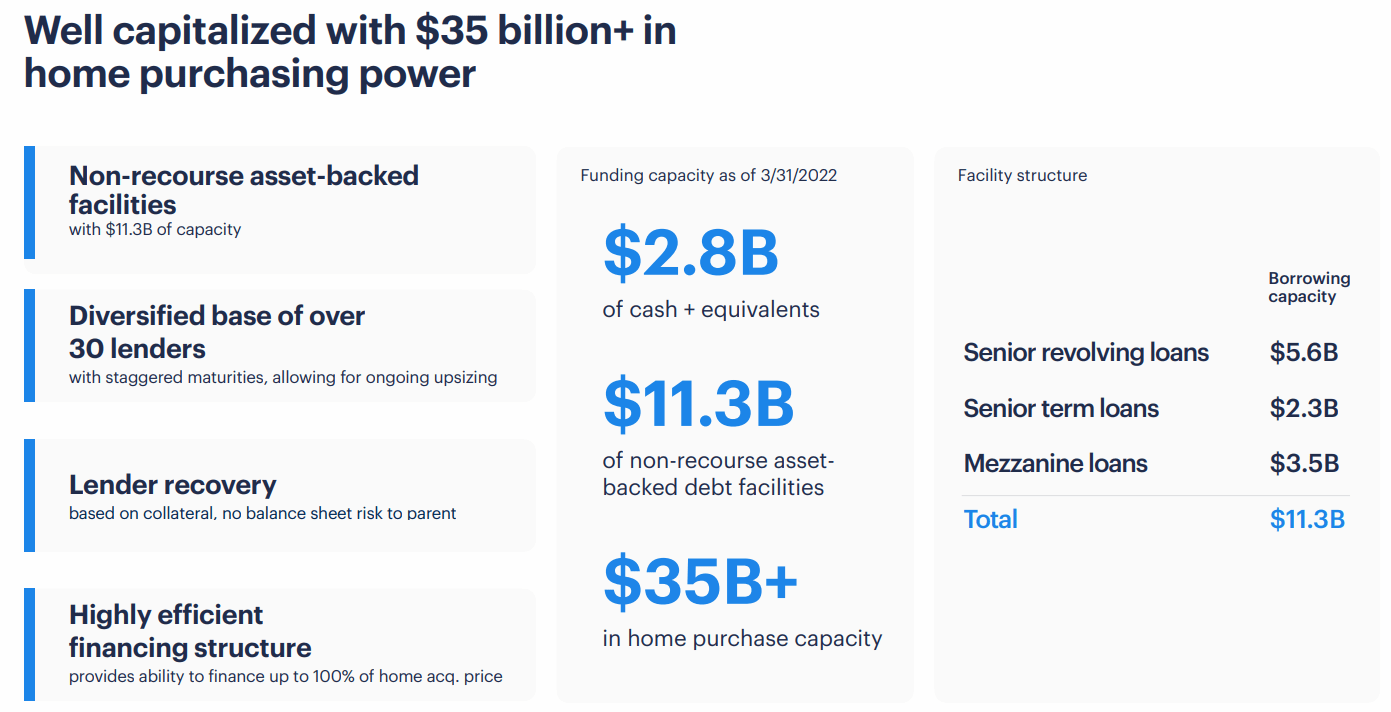

While I expect the next couple of quarters to bring massive business volatility at Opendoor, I think the company is well capitalized ($2.5B cash) to see it through any downturn in the housing market. As a market maker with the ability to raise transaction spreads during a bear market, Opendoor can continue to meet the financial goals set forward by its management team (even in these turbulent times). Most of Opendoor’s iBuying rivals are not as well capitalized, and this is why I see Opendoor emerging as a monopoly business on the other side of this downturn.

Opendoor Q2 2022 Shareholder Letter

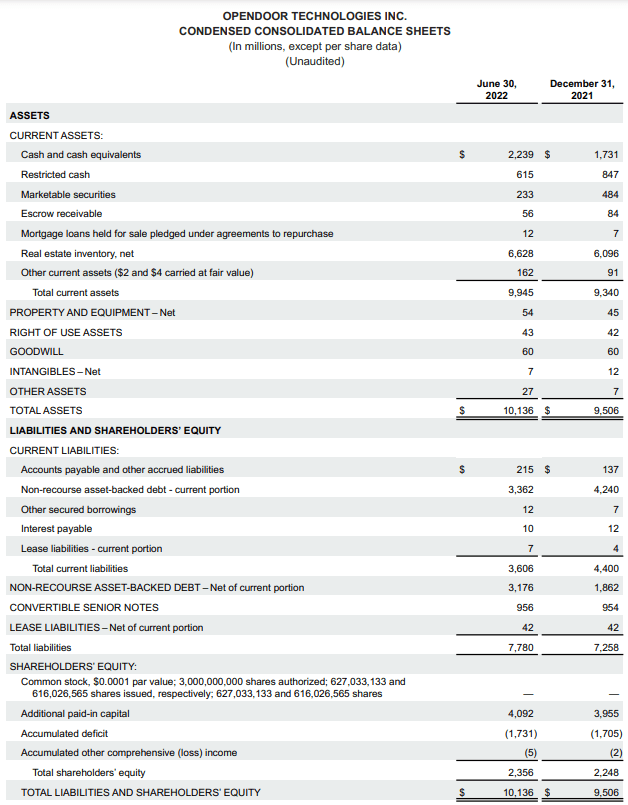

With “median existing home sales prices in the US” declining by ~6% in the last two months (~10-20%+ declines in metros), Opendoor is set to face inventory markdowns, and I think this figure could be as high as 8-10% ( ~$500-650M) of inventory ($6.6B). Such a loss will effectively wipe out Opendoor’s restricted cash (held as collateral for its asset-backed loans in addition to housing inventory). Due to impending transactional losses on homes bought in Q2 and rising holding costs, Opendoor is set to experience a significant cash burn in Q3. To limit losses, Opendoor’s management is cutting marketing expenses & third-party contractors, whilst focusing on inventory & risk management (getting rid of inventory quickly and slowing the pace of new acquisitions). Opendoor’s management utilized this playbook in 2020 and came out with flying colors (of course, the Fed was a friend at the time). Furthermore, Opendoor has a net cash balance of $2.2B (and a total cash balance of $2.8B).

Now, I can’t say with certainty that this playbook will work equally well during the current downturn; however, Opendoor’s control over acquisition volumes and a massive war chest ($2.2B net cash) means Eric Wu and Co. have all the necessary tools to navigate through this difficult environment and avoid bankruptcy. Once transactional volumes normalize, I would expect Opendoor to start making money again even if the prices continue to decline in a slow burn lower.

Opendoor Investor Presentation May 2022

While I expect the next couple of quarters to bring massive business volatility at Opendoor, I think the company is well capitalized ($2.5B cash) to see it through any downturn in the housing market. As a market-maker with the ability to raise transaction spreads during a bear market, Opendoor can survive and thrive during a bear market. Beyond Q4 2022, I think Opendoor will meet the financial goals (CM: 4-6%) set forward by its management team (even if the bear market in housing turns into a slow burn like what we saw after the great financial crisis). Most of Opendoor’s iBuying rivals are not as well capitalized, and this is why I see Opendoor emerging as a monopoly business on the other side of this downturn.

Where Is OPEN Stock Headed? Let’s Look At Some Technical Charts For Guidance

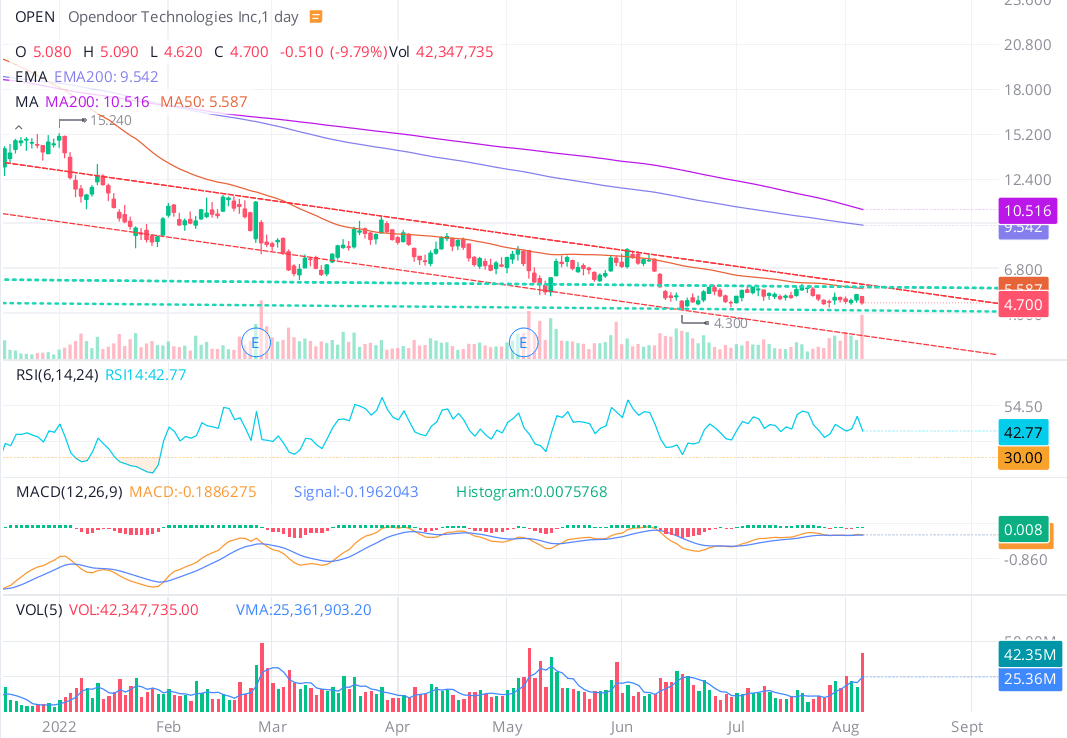

Opendoor’s stock had been trading in a base range of $4.3 to $5.7 per share since June 2022 until it broke down from the base last week. Here’s how we viewed the chart in August:

Technically, Opendoor’s chart is a dumpster fire, with the stock stuck in a downward wedge pattern for the last several months. Recent price-volume action is indicative of a base formation in the $4.3-$5.7 range, and the stock is sitting right at the top of this range after a +22% post-ER move on last Friday.

WeBull Desktop

Opendoor’s technical setup is getting interesting – a breakout from the base here could take the stock up to $8-10 in a jiffy. While Opendoor’s Q2 results were good, the bounce is likely a result of the announcement of the Zillow partnership, and a news-based rally can fade off fast.

Twitter

Since Opendoor failed to get past resistance at $5.7-5.8 during Friday’s session, the breakout is not confirmed, and we may well break back into the base over the coming days. Hence, I am not convinced about a short-term trade here. However, I think the long-term risk/reward is simply fantastic, and investors should use the ongoing volatility in Opendoor to take/build long positions at these depressed levels.

In hindsight, my buy rating for Opendoor at $5.7 looks silly, but the idea is to build a long position over time. A breakdown from its base is causing a technical selloff in Opendoor’s stock amid widespread FUD on the company.

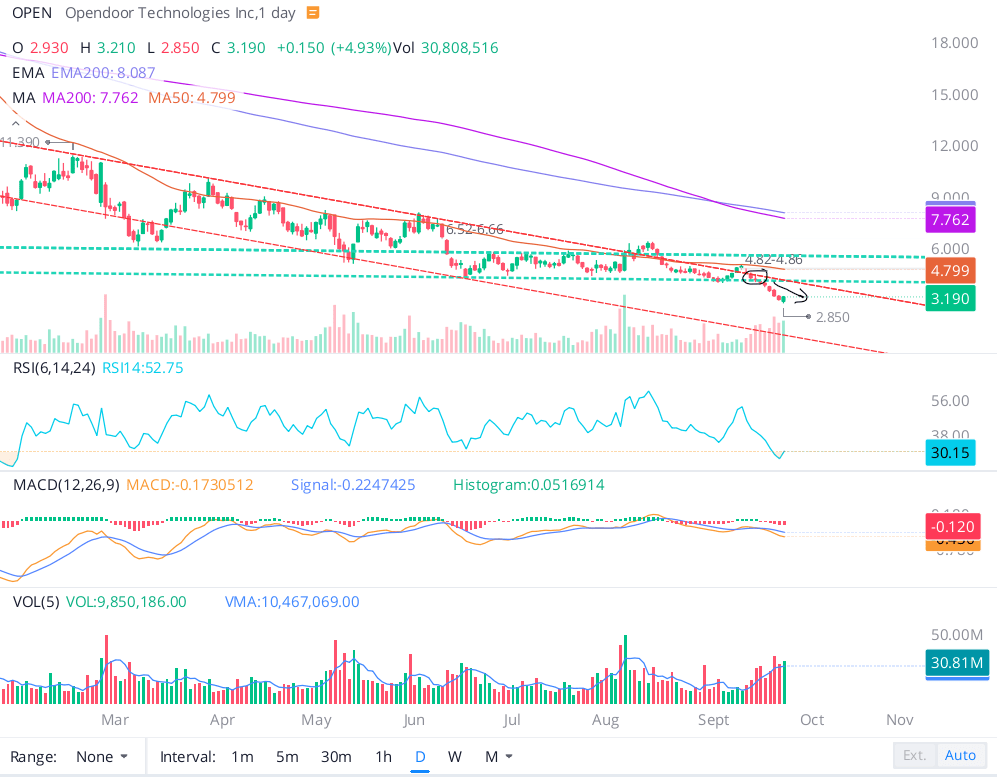

WeBull Desktop

While there’s no support zone on the chart, Opendoor is now trading below its net cash levels, and the stock looks oversold with the 14-Day RSI at ~30. A bounce to retest the $4.1 level (lower end of the base formation [marked in green dotted lines on the chart above] and upper end of the falling wedge pattern [observed in red dotted lines on the chart above]) could materialize soon. However, if we see rejection at that level or if Opendoor’s stock just continues to slide lower towards the lower end of its falling wedge pattern, then Opendoor could hit $1 (or lower) in the near to medium term (3-6 months).

Technically, Opendoor’s stock chart is broken, and I wouldn’t buy it for a short-term trade. While a stock’s price can trade based on sentiment for short periods of time, it will retrace to fair value over the long run. Let’s analyze Opendoor’s fair value and expected return using TQI’s Valuation Model.

Opendoor Stock Fair Value And Expected Return

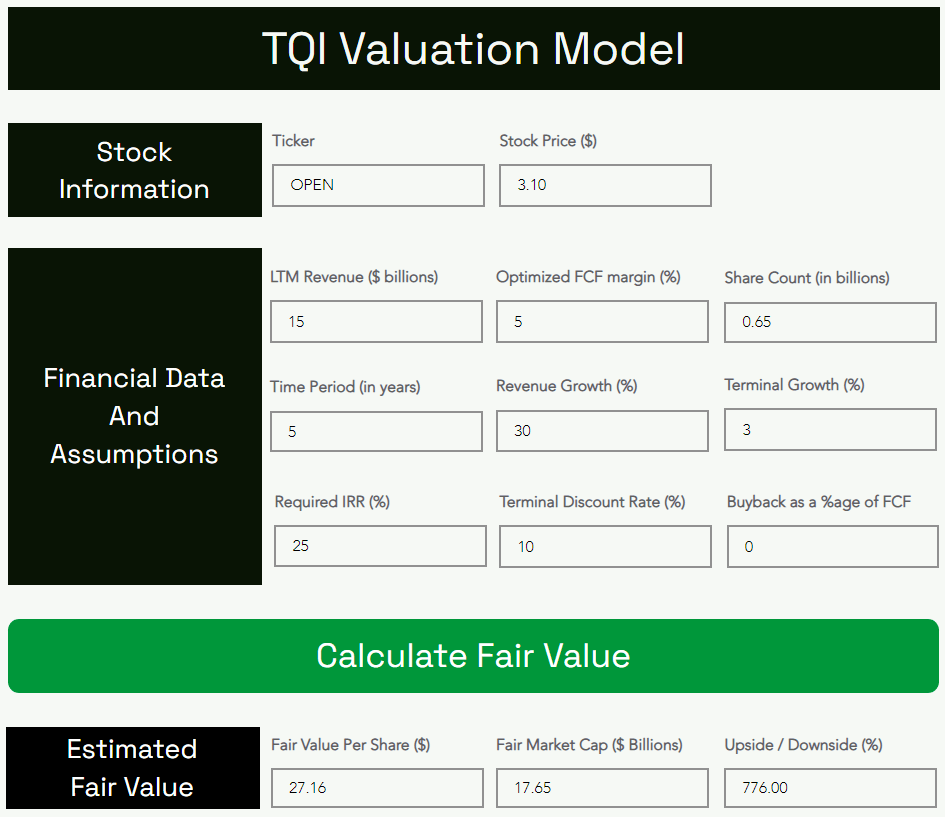

For 2022, I am now projecting Opendoor to achieve ~$15B in revenue, with housing demand normalizing in Q4 as consumers adjust to elevated mortgage rates and reduced home prices. With housing supply still well below demand, buyers will step in at some point. According to Datadoor, Opendoor sales figures rebounded sharply in August. Although Opendoor’s margins are likely to stay under pressure in the near to medium term as the iBuyer refreshes its inventory, I expect the cash burn to peak in Q3 at ~$400-500M. In a bear market, Opendoor’s value proposition improves significantly for sellers, and Opendoor could realistically charge a higher spread in a buyer’s market (bear market). We will see evidence of this business model feature in Opendoor’s Q3 results.

Over the long run, Opendoor’s transaction spread (difference between buy and sell price) should stabilize in the ~3-5% range in the long run. As we know, Opendoor charges a service fee of 5% to sellers. Furthermore, I believe that Opendoor could generate another ~5% margins from the sale of ancillary services (financing, moving, insurance, warranty, renovations, etc.) to buyers. Overall, Opendoor can end up generating ~15% in margins at the unit level. At scale, Opendoor aims to get its Operating Expenses down to ~3% and Interest, D&A, and Tax expenses down to ~2%. I believe these targets are achievable. And if Opendoor can shift to a 3P model and build an advertising & discovery business on top of its platform (like Zillow), then margins could go even higher.

Hence, Opendoor’s free cash flow margins could reach a 6-10% level at maturity. To implement a margin of safety, I chose an optimized FCF margin of ~5% in my valuation model for the company.

TQI Valuation Model (Author’s website: tqig.org)

Under TQI’s required IRR [discount rate] of 25% (for moonshot growth investments), Opendoor’s fair value came out to be ~$17.7B (i.e., $27.16 per share). With the stock trading at $3, it is currently trading at a significant discount to its fair value. Mr. Market has no faith in the iBuying business model, and Opendoor’s depressed valuation is a reflection of widespread FUD.

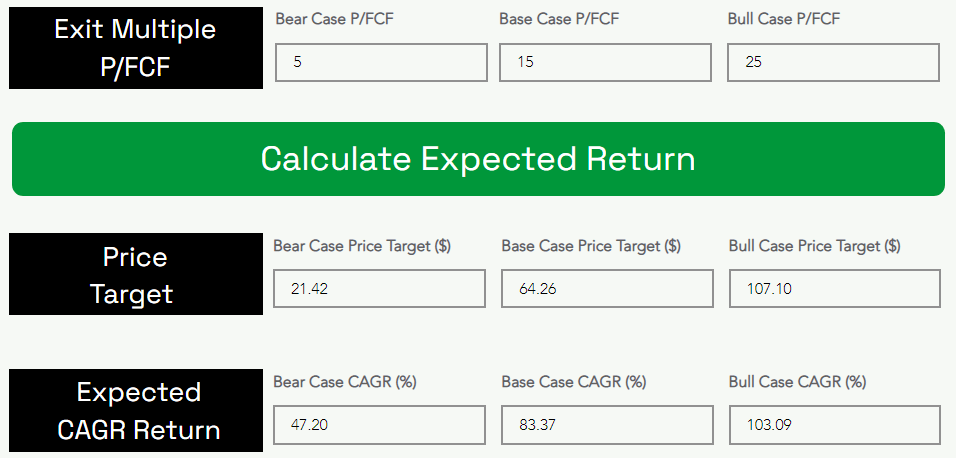

In a base case scenario, I expect Opendoor to trade at ~15x P/FCF (optimized FCF) at the end of 2027, which would be equivalent to ~0.75x 2027 P/S ratio based on my forward revenue projections shared above.

TQI Valuation Model (Author’s website: tqig.org)

With these assumptions, I see Opendoor trading at ~$42B in market cap by the end of 2027 [~21.4x higher than current levels], which would translate to an expected CAGR return of 83.37% over the next five years.

Risks

Here’s an updated list of investment risks associated with Opendoor:

While Opendoor has achieved a positive contribution margin for the last 21+ quarters (and is projected to do so in Q3 2022, too), Opendoor’s AI/ML-based pricing models have not been tested in a bear market (buyers market). If Opendoor’s models fail to adapt in a bear market, the company could suffer significant losses.

Mortgage rates have gone up vertically in 2022, with the 30-yr fixed rate going from ~3% to ~6.6% in a matter of months. As mortgage rates rise, house prices are resetting lower.

Over the last two years, the Fed was a massive buyer of mortgage-backed securities, and not having monetary policy support could further slow down demand for housing. With that said, mortgage rates and the Fed could do nothing to increase the housing supply, which is still much lower than demand. Also, homebuilders are cutting back on building new homes.

Due to a tight labor market, Opendoor could face higher wages and labor costs. Also, a shortfall of labor could lead to slower asset turnover, which could affect sales growth and hurt the bottom line at the same time.

Rising interest rates will increase financing costs for Opendoor. As we know, Opendoor buys homes using floating-rate credit facilities, and while they hedge for interest rate risks, the hedges may prove to be inadequate if rates move too fast or too far. This may lead to higher interest costs and lower profitability (or greater losses).

During the housing bubble [GFC] burst, average house prices in the US fell by about 25%, and this decline materialized over four years (the worst quarter being -3%). Typically, the housing market moves slowly, and a decline after the initial shock in the summer of 2022 will likely be a slow burn lower. Opendoor’s average holding period is less than 120 days (and they claim to buy 5-15% below fair value), i.e., they are unlikely to lose a lot of money even during bear markets.

Lastly, I would like to highlight a long-term risk. Opendoor is pioneering the iBuying industry; however, iBuying makes up less than 2% of the real estate market. While it is easy to say that iBuying will scale just like e-commerce, iBuying may hit a wall at some point in the next few years. Consumers know that an iBuyer will offer a price somewhat below fair value for the added convenience, and buyers know that they will be asked to buy somewhat above fair value. The economic interests of iBuyers and their customers are not aligned, and that could hinder the rise of iBuying. I believe Opendoor is the only player in the market that has the scale to operate at razor-thin margins and still make the numbers (unit economics) work. With that being said, Opendoor may fail to appease the masses and change consumer sentiment around iBuying.

Personally, I am not a big fan of hyperbole, but in my view, “Opendoor is a generational company that is showing similar potential to an early-stage Amazon or an early-stage Tesla”. At $3 per share ($1.9B in market cap), the iBuyer is trading at less than its net cash balance of $2.2B on widespread fears of a potential cash burnout and bankruptcy.

As I see it, Opendoor’s management team has showcased its ability to navigate a challenging macro environment through proactive risk management in 2020. And with a cash cushion of $2.2B, the company can afford to take the upcoming hit from transactional losses in Q3 and Q4. Once the ongoing uncertainty in the housing market (with regards to mortgage rates & restrictive monetary policy) recedes and affordability shows signs of improvement, homebuyers will step back within the next few months because housing supply is still very much constrained (and well below demand) and homebuilders are pausing on new projects due to high rates. A slow burn lower (like what we saw after GFC) is a possible outcome for the housing market; however, Opendoor is built to survive and thrive across all market cycles.

The iBuying business model has little to no credibility among investors, especially after Zillow’s (Z) iBuying operations blew up in 2021. With that being said, Opendoor is the pioneer of this nascent space, and the operational execution shown by Opendoor’s team is far superior to Zillow. The recently announced partnership between Opendoor and Zillow is a big vote of confidence in Opendoor’s vision and implies a big victory on the seller side of its platform. Opendoor’s buyer solutions are still early, but the product development trajectory is very impressive.

We are entering a period of weak financial performance for Opendoor with a downward inflection in the housing market; however, the stunning financial performance of the last five years indicates that Opendoor can make iBuying work. Opendoor is set to do revenues of $15B in 2022, and it is now operating in 50+ markets across the United States. In a nutshell, Opendoor is no dot-bomb; it’s a generational company in the making.

My detailed coverage of Opendoor is available in the following research notes:

While Opendoor is certainly a high-risk, high-reward bet (considering the ongoing volatility in housing markets), we may not get a better valuation to take a long position in Opendoor (with the iBuyer trading below net cash levels, i.e., $1:$1 valuation). In conclusion, I view Opendoor as a generational buy at $3 per share for bold, contrarian, long-term investors.

Key Takeaway: I rate Opendoor a generational buy at $3 per share.

Thanks for reading, and happy investing. Please share your thoughts, questions, or concerns in the comments section below.

Editor’s Note: This article was submitted as part of Seeking Alpha’s best contrarian investment competition which runs through October 10. With cash prizes and a chance to chat with the CEO, this competition – open to all contributors – is not one you want to miss.Click here tofind out more and submit your article today!

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment