Kanrawee Jinpanich/iStock via Getty Images![]()

About the company

Opal Fuels (NASDAQ: OPAL) is a nationwide operator in the production and distribution of low-carbon intensity renewable natural gas (RNG). Their waste-to-energy model combines the production and distribution of RNG, providing a cost-effective solution to reduce carbon emissions in heavy-duty transportation and other industrial markets. Their model primarily works by capturing methane emissions from landfills and dairy farms (upstream), purifies them, and uses that energy to replace diesel and other high carbon intensity fossil fuels (downstream).

RNG output is expected to grow rapidly in the years ahead as more companies work to minimize environmental damage. Opal is vertically integrated, meaning it can simultaneously work with landfills and dairy farms to limit their emissions while meeting demand for clean fuel from large companies. Currently, RNG is a tiny sliver of the energy market and significantly cheaper than diesel fuel. The biggest incentive for customers using RNoh G is potentially obtaining fuel and green-energy credits.

Opal Fuels went public through a SPAC at a valuation of roughly $2 billion and also raised $125 through PIPE (private investment in public equity). NextEra Energy, a leader in the renewable energy space also made a preferred equity investment of up to $100 million. The next decade is going to be very interesting for renewable energy and with fresh capital from the SPAC transactions, I think it is poised to deliver on multiple fronts as we will see in the upcoming sections.

Business Scope and Impact

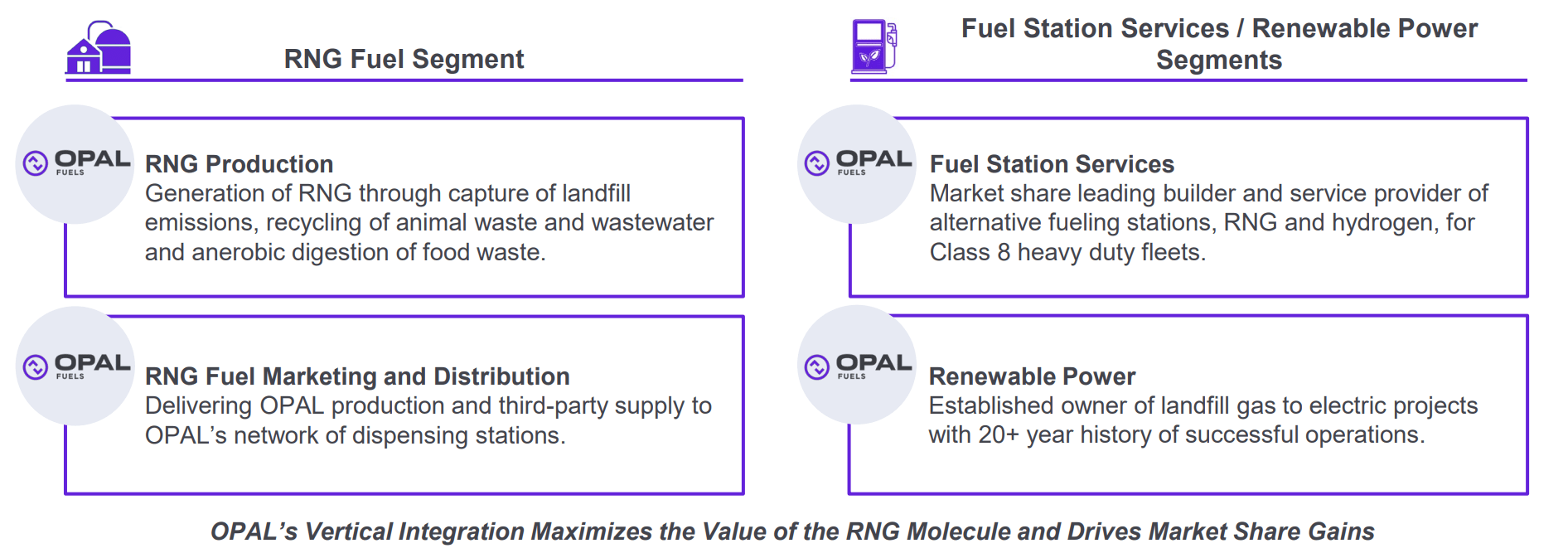

One of the things that stands out for this company is that it is a leader in its segment. As a vertically integrated operator, it has full control of the entire process of developing renewable natural gas. Below is a demonstration of the RNG value chain that is fully controlled by Opal Fuels.

RNG Value Chain (Company Website)

Furthermore, as a nascent industry, there is big potential for this business to grow further for the following reasons –

- Market fundamentals for renewable energy are supported by strong policy. Policy is also driven by climate change goals and RNG offers immediate carbon reduction impact

- High diesel price makes using RNG attractive as it is priced less than diesel

- Currently, RNG covers less than 1% of the US heavy duty market and it is forecasted that the supply will triple in five years

When it comes to methane, it is much more lethal than CO2 for its impact on global warming. RNG has an immediate positive impact on climate change as it helps with methane capture at the source. It is estimated that RNG can help eliminate up to 28% of U.S. methane emissions. Also, one of SEC’s recent mandate forces publicly traded companies to report on greenhouse-gas emissions from their own operations (Scope 1) as well as from the energy they consume (Scope 2). When RNG is used as a transportation fuel, it results in zero Scope 1 and Scope 2 emissions.

Financial Dive

Opal Fuels had their first earnings call as a public company. Here, they clearly demonstrated that they have been able to deliver on multiple fronts – securing new biogas rights, starting new RNG projects, commencing operation from recently completed projects, increasing the number of fuel stations that dispense RNG and most importantly, secure the needed capital to fund the next wave of growth. How does this all translate to their financials? Let’s dig in.

Between 2020 and 2021, their business saw a 41% growth rate in their revenues. Their first 9 months of 2022 saw an increase of 60% in revenues when compared to the same time period. Zooming in specifically for this quarter alone, Opal Fuels made about $66M in revenues, an increase of 40% from the same time period over a year ago. There have been a lot of SPAC transactions which included rosy projections in revenue but didn’t really deliver after the deals went through.

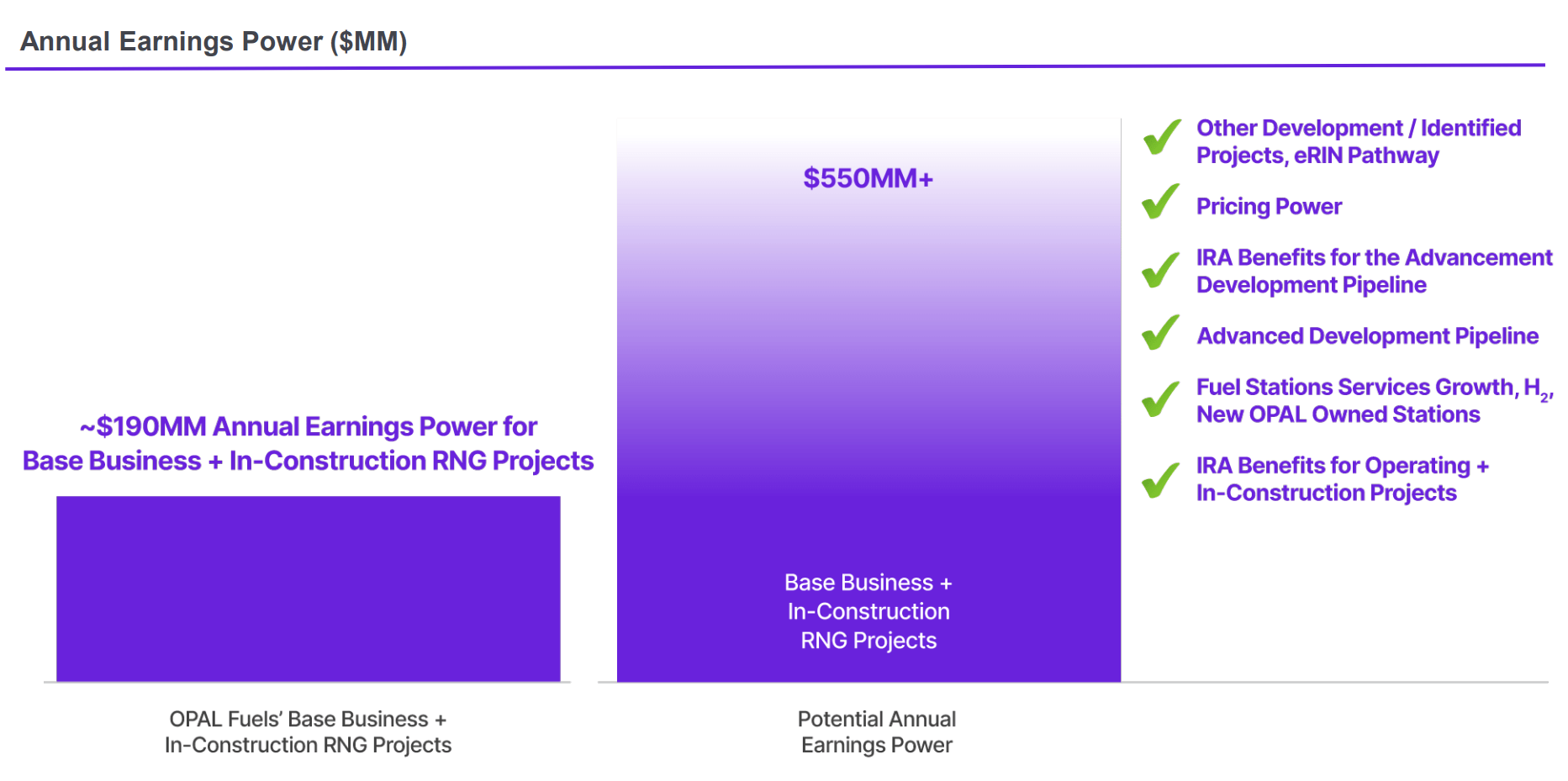

In light of this, it’s good to see an example of a company which is firing on all cylinders. Strong numbers for Opal are primarily driven by its Fuel segment and it will be interesting to see how much of an impact the new projects will have on the company in the near future. Its strong pipeline of projects and strong public policy initiatives are expected to give Opal Fuels strong earnings power.

Author Calculations – Company Data Annual Earnings power (Company Website)

The next question we need to answer is if the company has enough liquidity to deliver on the promised earnings.

- Its total assets stand at $650M which includes more than $150M in Cash

- Its short term assets exceed both its short and long term liabilities

The above information combined with its liquidity ratios give us enough confidence that the company has no problems with its balance sheet and its pipeline of projects could be conveniently financed with available cash, its anticipated cashflows from its operations of its existing business and available credit lines under existing debt (Currently, the company operates about 6 RNG facilities and 18 renewable power plants and has about 7 RNG projects in construction. In the fuel station segment, it operates 123 stations and has about 43 stations under construction)

Valuation

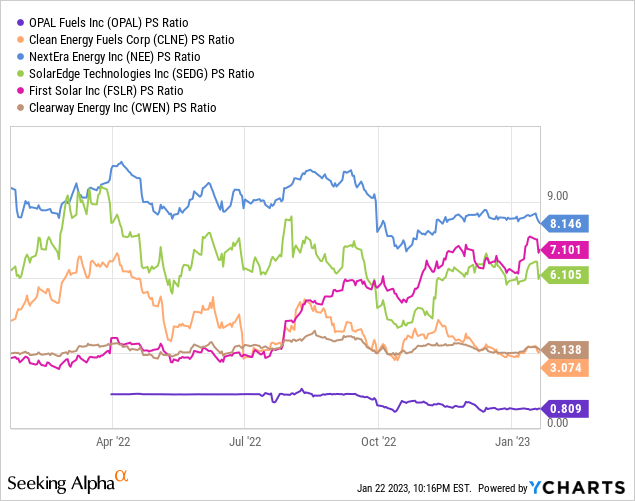

As this is a newly formed public company that has shown promising growth, one reliable indicator to value this company would be the Price to sales multiple. It currently trades at 0.8, far lower than the Energy sector median at 1.35. If we look at this only through the lens of renewable energy, the comparison gets even better (In fact, one of the comparables, NextEra Energy (NEE) is a big investor in Opal Fuels). The nearest comparable is Brookfield (BAM) and this is at 1.7!

From a valuation standpoint, the stock is already quite attractive at these levels. If Opal fuels continues to put out growth numbers as impressive as the previous years, valuation will get depressed even further. The company anticipates to provide guidance for 2023 along with its results for fiscal 2022. I for one will be eagerly watching out for this guidance.

Competition

Opal’s nearest competitor in the renewable natural gas space is Clean Energy Fuels (CLNE). Clean Energy Fuels has a bigger footprint of stations than Opal and also bigger in terms of its overall operation. It is also the largest renewable natural gas provider under California’s Low Carbon Fuel Standard (LCFS) program. However, there are a couple of things that comfort me if I am being an investor in Opal and gets me less worried about the competition.

- Clean Energy Fuels is richly valued at 3 times sales

- Revenues at Clean Energy have been flat for almost a decade

- They have been unprofitable for almost every year in the last decade and shareholders have also been diluted rapidly

So between the two companies, even though Clean Energy Fuels is bigger and competes directly with Opal Fuels, I feel I am in a better position investing in Opal than Clean Energy Fuels.

Final Call

I am rating Opal Fuels as a buy. I will also be initiating a very small position less than 1% of my portfolio and will be closely watching for their fiscal 2022 results and their guidance for 2023. This would give me more confidence to either increase or trim my position.

Be the first to comment