SouthWorks/iStock via Getty Images

Investment Thesis

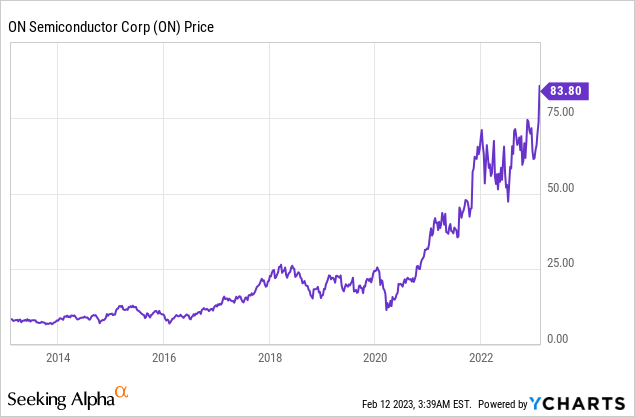

ON Semiconductor (NASDAQ:ON) has been one of the best-performing companies in the past decade, with shares up nearly 900% during the period. Despite facing inflation and macro headwinds, share price continues to rise and is now trading near all-time highs.

The company has a huge and fast-growing addressable market that is benefiting from multiple tailwinds such as the shift to EVs (electrical vehicles). This is reflected in its latest earnings result as it continues to show solid growth even though the semiconductor industry is slowing down. The bottom line is also impressive as it demonstrates strong operating leverage. Even after the rally, the current valuation is still compelling with multiples below historical averages, not to mention its strong prospects and growth. Therefore I rate the company as a buy.

Strong Growth Drivers

ON Semiconductor is a US-based company that focuses on intelligent power and sensing technologies. These technologies are critical for energy infrastructures, centers, electrification, automation, etc. The company’s existing customers include big names like Tesla (TSLA), NVIDIA (NVDA), Boeing (BA), Nio (NIO), and more.

The TAM (total addressable market) for these solutions is huge and growing. According to the company, intelligent power is a $64 billion market growing at a 6% CAGR (compounded annual growth rate) while sensing technologies is a $10 billion market growing at a 10% CAGR.

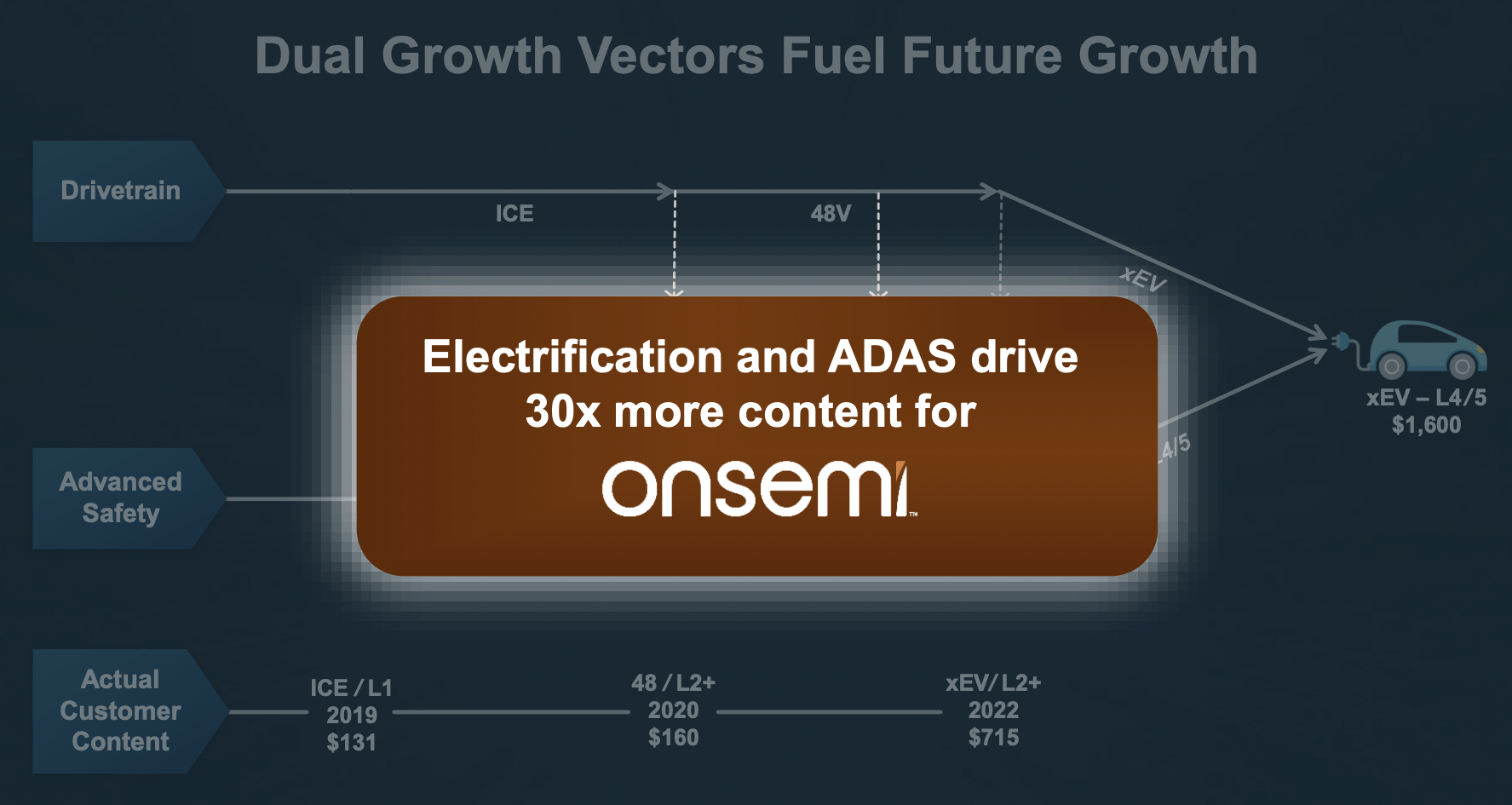

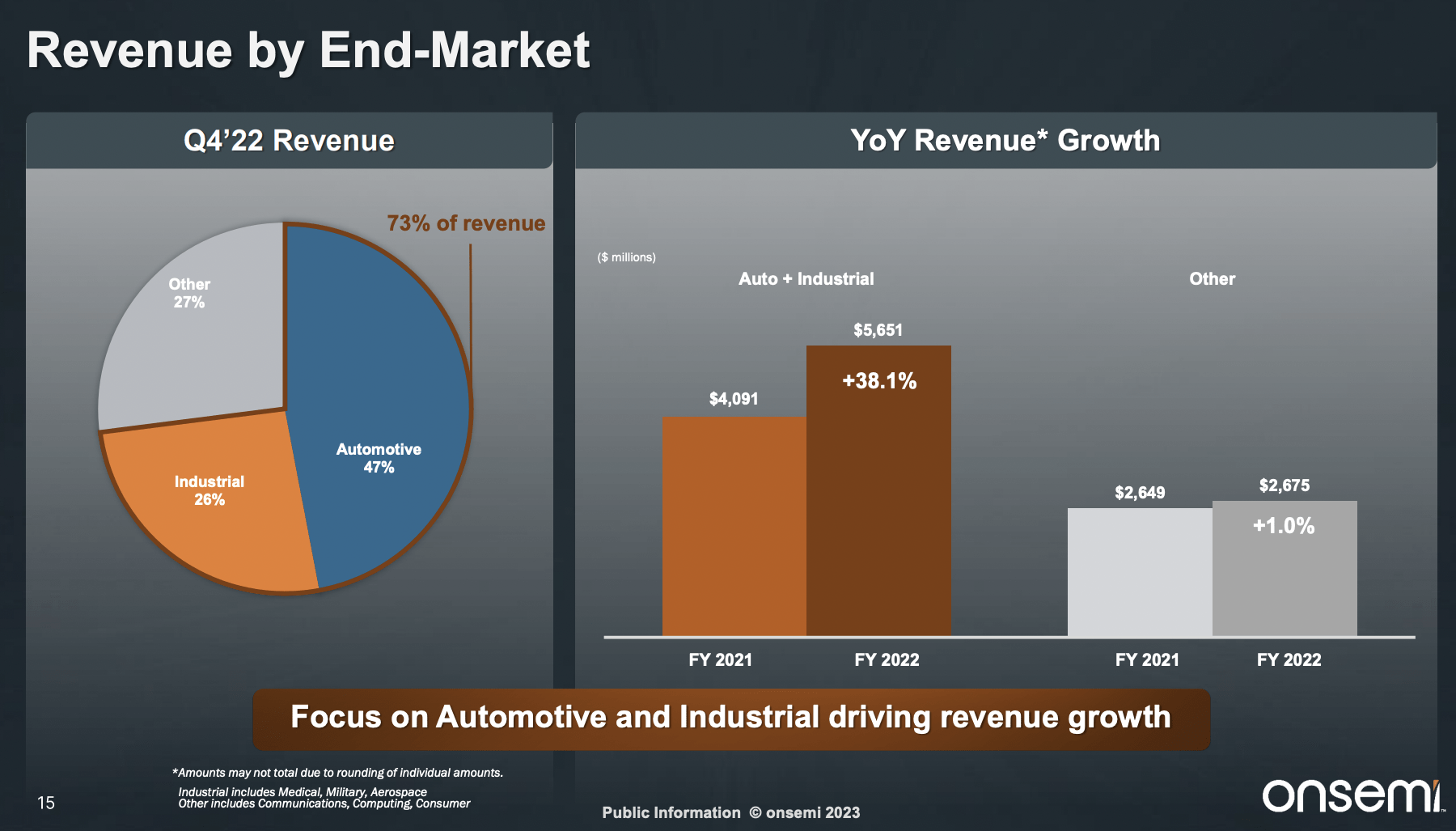

There are multiple tailwinds driving the expansion. The most notable one is definitely EVs. The adoption of EVs has been increasing rapidly and according to S&P Global, 50% of vehicles will be electrical by 2030. This is significant because EVs use a lot more solutions compared to ICEs. A lot of EVs come with ADAS (advanced driver assistance systems) which actually require sensing solutions as well. The company expects the addressable market of its automotive segment will grow at a CAGR of 17% from 2021 to 2025. This is huge as automotive accounts for roughly 47% of total revenue.

Hassane El-Khoury, CEO, on the automotive market:

By focusing on the areas where we provide the most value to our customers, we have positioned ourselves with the market leaders in the fastest-growing segments in automotive and industrial. The top automotive OEMs are not only choosing onsemi for silicon carbide, but for our worldwide class intelligent power and sensing solution. In automotive, we have seen tremendous momentum with silicon carbide, and we believe that vehicle electrification will be a long-term driver for our business.

Other tailwinds include 5G and Cloud. The deployment of cell towers and data centers continues to increase due to digitization, increasing needs for connectivity, and the shift to the cloud. This is driving the demand for intelligent power solutions as operators are looking for products that can optimize power consumption in their infrastructure to improve costs and efficiency. According to the company, the 5g and cloud market is expected to grow at a CAGR of 11% from 2021 to 2025. I believe these are all long-term secular tailwinds that should act as strong growth drivers for the company.

ON Semiconductor

Q4 Earnings

ON Semiconductor reported its fourth-quarter earnings last week and the results are very impressive, especially the bottom line.

The company reported revenue of $2.1 billion, up YoY (year over year) compared to $1.8 billion. The growth is mainly driven by automotive revenue which increased 54% YoY to $989 million. Automotive revenue now accounts for 47% of total revenue compared to just 35% last year. On a segment basis, ISG (intelligent sensing group) revenue was up 44% YoY from $245.4 million to $354.2 million. PSG (power solutions group) revenue was up 10% YoY from $953.4 million to $1.05 billion. While ASG (advanced solutions group) revenue was up 8% YoY from $647.3 million to $701 million.

The bottom line was extremely strong thanks to excellent cost and expense management. Thanks to manufacturing optimization, cost of revenue was only up 6.8% and gross margins increased 340 basis points from 45.1% to 48.5%. Gross profit was $1.02 billion compared to $832 million, up 22.6%. YoY. The management team was very disciplined on operating spending and operating expenses for the quarter actually decreased 10.1% from $351.9 million to $316.2 million. This resulted in operating income up a whopping 46.6% from $480.3 million to $704.3 million. The operating margin was 33.5% compared to 26%, up 750 basis points. EPS for the quarter was $1.35, an increase of 40.6% from $0.96.

The quarter was immaculate in my opinion. Not only did the company manage to grow revenue by double digits despite facing macro headwinds, it also showed significant operating leverage with margins and income increasing significantly.

ON Semiconductor

Investors Takeaway

I believe ON Semiconductor should continue to do well in the long term. Intelligent power and sensing technologies have huge market opportunities and it is benefiting from very strong secular tailwinds. The company’s execution was also outstanding as fourth-quarter results demonstrated solid revenue growth and significant bottom-line improvements. The current valuation is still compelling after the recent run-up. The company is trading at a PE ratio of 19.72x which is cheap on a historical basis. It represents a 33.2% discount compared to its 5-year average PE ratio of 29.53x. Considering its prospect, growth, and valuation, I believe there is still meaningful upside potential from current price levels. Therefore I rate the company as a buy.

Be the first to comment