Justin Sullivan/Getty Images News

Investment thesis

Despite the major drawdown in the shares, we rate the shares as neutral. Omnicell’s (NASDAQ:OMCL) poor track record, low returns, volatile profitability, and lack of earnings visibility are high risks that are not sufficiently counterbalanced by current valuations.

Quick primer

Based in Mountain View, California, Omnicell is a manufacturer and provider of medication management solutions, supplying care providers and retail pharmacies with automated dispensing systems. The company is aiming to provide an ‘autonomous pharmacy’ and is said to have close to 160,000 devices installed in hospitals around the globe, dispensing close to 5 million doses daily. 90% of sales are derived from the United States, with the remaining coming from the rest of the world. Its peers include McKesson (MCK), Becton, Dickson and Company (BDX), Baxter (BAX), Capsa Healthcare, Swisslog, Willach Group, Yuyama, and Label Pharma.

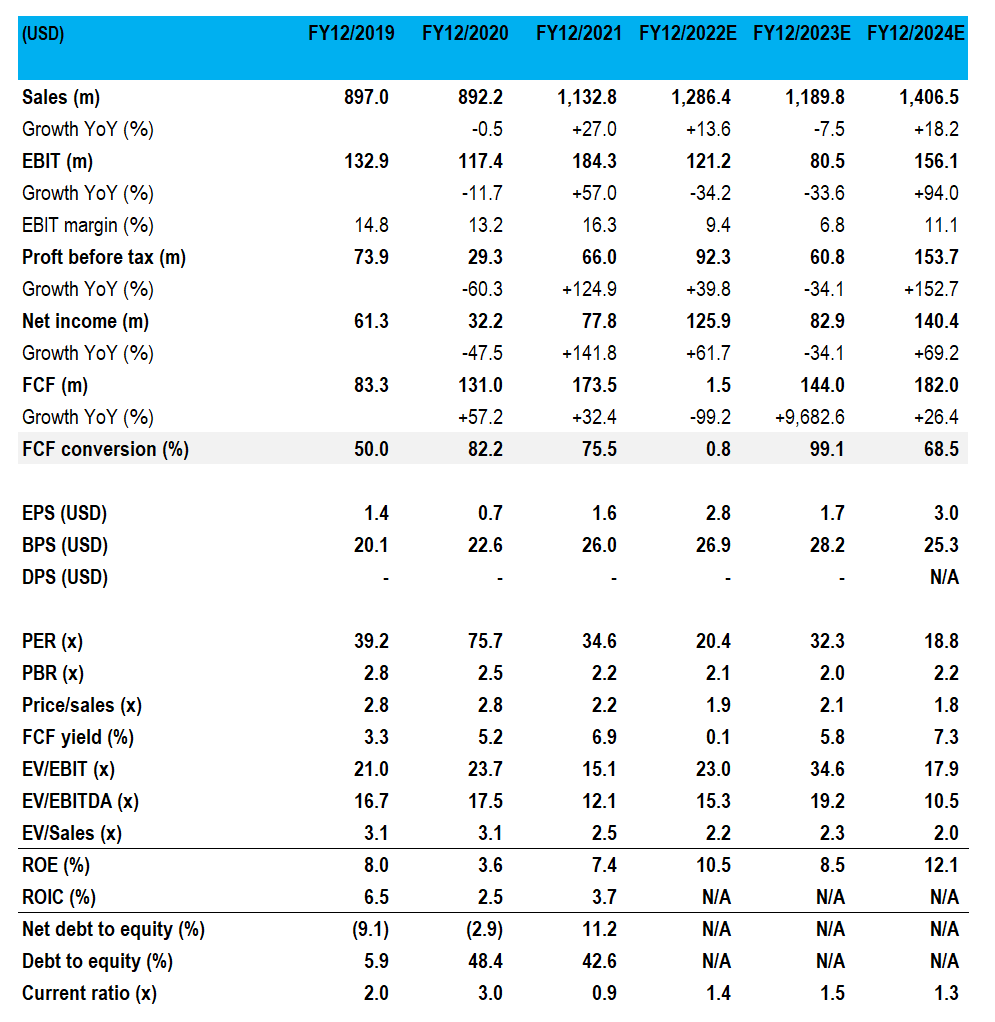

Key financials with consensus forecasts

Key financials including consensus forecasts (Company, Refinitiv)

Our objectives

Omnicell’s shares have experienced a 63% drawdown, following a major negative surprise in Q3 FY12/2022 results. The company guided down its outlook for product bookings (an indication of future installations by customers), due to headwinds driven by budget freezes, project delays, and ongoing customer labor shortages. The company has also stated that it will cut headcount by 9% to address its cost base in light of macro challenges.

The company has had questions raised over its accounting in 2019, and now there are concerns over management’s judgment of assessing booking visibility. Other working practices highlight a higher-than-expected level of aggressiveness in managing accruals by selling the majority of our multi-year lease receivables to third-party leasing finance companies (page 15) and capitalizing software development costs despite its hardware lease business.

We want to assess whether the shares are investable, given the major drawdown event.

Major drop in perceived quality

For a business operating in a defensive medical sector, Omnicell’s track record is exemplified by a focus on steady sales volume expansion, but unstable profitability (margins have ranged from 1.6% to 11.2% over the last 10 years), continually low ROE and lengthening cash cycles (signifying poor working capital management). All in all, the company is a low-return business but has been viewed and valued somewhat questionably as a high-quality Medtech franchise. Their solutions are relatively low-tech; EBIT margins should be in excess of 20% to denote major value-add. The total addressable market looks relatively mature in the US given their growth to date, and the fact that overseas markets have refused to open up signifies that there appears to be a limited need for Omnicell’s solution versus a traditional human pharmacy model.

We view management as being focused on volume growth (as opposed to earnings). Disclosure of strong product bookings has always been a major driver of the share price, and the guidance cut from a range of USD1.37 billion-USD1.43 billion to USD0.95 billion-USD1.05 billion for FY12/2022 in just a matter of 9 months signifies to us that management has either totally misjudged customer sentiment, or are guilty of pursuing unrealistic targets. Either way, management’s credibility has irrevocably fallen.

With a negative earnings outlook, management announcing a 9% headcount reduction signifies expectations of a major slowdown in business activity, as opposed to a transient blip in demand from delays and postponements. The company has been found to be a weak performer on multiple fronts – we assess the outlook for a recovery.

Recovery may take some time

Consensus forecasts (see Key financials table above) show a continued decline of 34% YoY in EBIT for FY12/2023, followed by a major recovery into FY12/2024. Management indicated that there were multiple reasons for product bookings guidance to be lowered; delays and postponements from capital budget changes, lack of staff at customer sites for installation work, and concerns over nursing shortages. We want to assess whether these factors can be mitigated into FY12/2024.

Many developed economies are facing affordability and access issues in their healthcare systems, and the US is no exception. COVID-19, inflationary cost pressures and a recessionary environment is placing pressure on care providers as well as end customers. As a result, we believe that hospital budgets will remain under pressure and will prioritize spending on new approaches to healthcare such as virtual and available-at-home services. Investment into pharmacies is also focusing more on provider-owned specialist pharmacies, as opposed to automating commoditized generic operations in a hospital. Direct-to-consumer pharmacy space is pushing new forms of drug delivery. Investing large upfront costs in an ‘autonomous pharmacy system’ no longer looks as relevant as before.

Nursing shortages are expected to continue, driven by factors such as burnout, an aging population, and limited training. The lack of nursing staff has been said to result in postponements as installing new systems causes disruption. If this is the case, we believe that lead times for system delivery will be longer than in the past, resulting in poorer working capital management and lower free cash flow generation.

As things currently stand, we believe consensus is being too optimistic for a recovery profile in FY12/2024. We also have concerns that with low single-digit ROIC in FY12/2020 and FY12/2021, the company has been investing unsuccessfully in its business.

Valuation

On consensus forecasts, the shares are trading on PER FY12/2023 32.3x; a strong recovery in FY12/2024 lowers the multiple to 18.8x. With limited visibility for the short to medium term, we believe these valuations are too optimistic.

Risks

Upside risk comes from a major recovery in demand from hospitals as budgets are allocated to medication management solutions. The possibility here appears low, given the immediate company effort at headcount reduction.

The company could start paying a dividend or conduct large buybacks as the shares have fallen (the last was back in 2014).

The downside risk is a continued weak outlook for product bookings, worsening the earnings outlook and limiting free cash flow generation.

Continued weak quality of earnings will result in the shares being downgraded, with the majority of sell-side ratings still remaining as a ‘buy’.

Conclusion

With the recent price action, we were hoping the shares were an opportunity. Unfortunately, given the poor track record of the business, poor management, low returns, and limited earnings visibility, we are going to remain on the sidelines. Our conclusion is that Omnicell’s addressable market is ex-growth, and the company has limited options to drive growth.

Be the first to comment