itjo/iStock via Getty Images

Omeros (NASDAQ:OMER) is a long-time favorite of mine that has fallen on hard times. My most recent Omeros article 10/05/2022’s “Omeros: Taking It To The Max” (“Max”), reported on its new OMIDRIA royalty monetization deal. Omeros has since reported its Q3, 2021 earnings call (the “Call“).

Recently, on 12/23/2022 its extreme market gyrations on no apparent news grabbed my attention. In this article I report on the situation and bring the Omeros story up to date.

The Call provided helpful insights on the forward path for Omeros’ stem cell TMA BLA.

Omeros watchers have been repeatedly pummeled by delays in its efforts to get approval for its narsoplimab in treatment of stem cell TMA. It is frustrating that this novel therapy, once so close to a final decision, has been delayed for an indefinite time.

CEO Demopulos opened the Call reporting on the FDA’s recent response to its CRL appeal. The FDA did not reverse the CRL; however it did point to a possible path forward:

… based on historical survival data, specifically the designer proposed a resubmission. That includes comparing response from our completed pivotal trial to a threshold derived from an independent literature analysis and evidence of increased survival from patients in our completed trial compared to an appropriate historical control group.

It also notes that persuasive evidence of superior survival versus a well matched historical control group could be sufficient even in the absence of the independent literature analysis.

This report was understandably limited given the timing of the decision. The important question for interested patients and investors is how long of a wait will it take to move this forward. The answer is unclear. Several analysts on the Call asked penetrating questions which help to shape the situation, including:

- Q…is there a scenario here where Omeros would consider abandoning this indication… A. Omeros believes the data supports approval, abandoning it is not on the option table at this point;

- Q…what is the minimum survival benefit the FDA wants to approve narsoplimab…A. this has not been discussed, but survival benefit exceeds that in the literature and is substantial;

- Q…isn’t the historical control that the FDA is now looking for pretty much what Omeros proposed in 2019 for its pivotal study for narsoplimab in HSCT-TMA…A. yes;

- Q…how close is what the FDA is now proposing to your secondary endpoint in your pivotal trial…A. very close.

Oh what might have been.

The sounds of silence are echoing hollowly following the Call.

Impatient biotech investors are guaranteed a nasty bout of angst. Add a holiday season to the mix and the situation is sure to fester. The Call was dated 11/09/2022, a mere 46 days prior to 12/26/2022 as I write. Unsurprisingly, but nonetheless, frustratingly, there has been no news from Omeros during this period.

I have dutifully checked Seeking Alpha’s Omeros news feed, press releases and SEC filings to see if there have been any developments since 11/09/2022. Crickets.

Ironically the most significant possible news came in the context of a Christmas Day inquiry as a comment to my 08/2022 article “Omeros: Off To Never-Never Land”. The comment from jros asked:

…hoping you can answer a question. It seems NOPAIN ACT is in the omnibus bill. Does this trigger the “bonus” payment under the Omidria royalty deal? This seems like a large potential addition to revenue and the bottom line.

I responded:

…During Omeros Q3, earnings call seekingalpha.com/… CEO Demopulos discussed this as follows:”…the non-opioids prevents addiction in the Nation Act or the NOPAIN Act is making good progress. With strong bipartisan and bicameral support that includes chairpersons and key members of relevant congressional committees. The bill now has half the Senate and 118 representatives as sponsors and co-sponsors. The sponsors are optimistic that a vehicle for the bill will be available in the near future.

The NOPAIN Act would provide separate payment for non-opioid pain management drugs like OMIDRIA in both the ASC and Hospital Outpatient Department settings for our renewable five-year period.

Passage of the no pain Act would trigger a $200 million milestone payment to Omeros from Rayner Surgical. The entirety of this milestone payment would belong to Omeros…

Unfortunately the omnibus bill is such a compendium that I daren’t venture a guess as to whether jros is correct in his supposition that it includes the NOPAIN ACT. If it does then it would be significant indeed. It would add $200 million to Omeros Q3, 2022 reported cash and investments of $221 million.

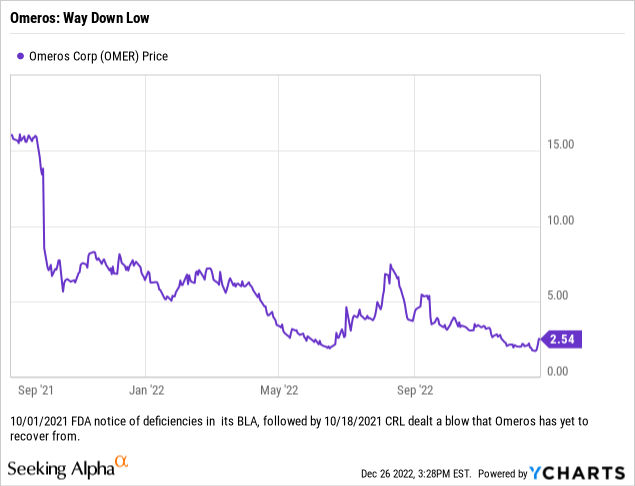

In any case as I write on 12/26/2022 there is no new Omeros news to be had. This lack of news likely contributes to uncertainty as reflected in stock erratic movements below.

Omeros stock went on a wild ride the last trading day before Christmas revealing a high-risk profile.

Omeros stock has provided crazy gyrations for traders during 2022. It has been particularly prone to excess immediately prior to long holidays. For example on the last closing day before Independence Day of 2022 it raced up 69% on no obvious news.

As a not atypical response to such excess, it gave back 29% on the next market day. The volume on run-up was >13 million shares well in excess of its average and even its previous high volumes for the year. As for its trading on 12/23/2022, the last trading day before Christmas, it opened at $2.55, ran up to its high for the day of $3.39; then it dropped to its $2.28 low for the day.

Omeros closed for the Christmas holiday at $2.54; it closed the day down one penny from the $2.55 where it had opened. Its peak to trough was a move of >46%. Its change for the day was a paltry ~01.5%. Its volume was >4 million shares. This was multiples more than typical and only the ninth time it had traded over a million shares since July.

What on earth is going on with Omeros? Why does it have such unusual trading patterns? To me it is an enduring mystery. Its short interest at >15% is far in excess of most of its peers as shown on Seeking Alpha. On the other hand, comparably-sized biotechs from a list of the most highly shorted stocks have short interest well above 25%.

I am an Omeros bull so I am hopeful that its upwards feints are revelatory of good things to come. If it can reel in its NOPAIN ACT $200 million that would certainly merit a nice bump in price. Omeros owns 100% of the development rights for its nice pipeline (slide 3). Its Rayner Surgical deal as described in Max shows that it knows how to make deals that generate top value for it.

Unfortunately, the happy thoughts of a bull seem to lack any real purchase on Omeros’ share trajectory. Despite upward spasms as reported, Omeros bears have maintained a tight grip on its overall movement as reflected by its post 09/01/2021 stock chart below:

When bears look at this chart followed by apparent inability to get its BLA back on track, they see a potential existential crisis.

Check out its “Financial Condition – Liquidity and Capital Resources” section from its Q3, 2022 10-Q. It lists its funding expectations as use of:

- …our cash and investments,

- OMIDRIA royalties and, potentially, the $200.0 million milestone related to achieving long-term OMIDRIA separate payment…

- if FDA approval is granted for narsoplimab for HSCT-TMA, we expect that sales of narsoplimab would also provide funds for our operations

- …we have a sales agreement to sell shares of our common stock, from time to time, in an “at the market” equity offering facility through which we may offer and sell shares of our common stock in an aggregate amount of up to $150.0 million;

- should it be determined to be strategically advantageous, we could also pursue debt financings as well as public and private offerings of our equity securities, similar to those we have previously completed, or other strategic transactions, which may include licensing a portion of our existing technology

- …we could also reduce our projected cash requirements by delaying clinical trials, reducing selected research and development efforts, or implementing other restructuring activities.

Each of these options has its limits which define a risk profile that is definitely speculative. According to the Call Omeros had a Q3, 2022 cash burn of $21.6 million plus $5 million in manufacturing costs. It had $221 million in cash and investments, $95 million of which will likely go to pay near notes due towards the end of 2023. This leaves it with a comfortable year cash runway.

Beyond that the alternatives are unsure.

Conclusion

I am an Omeros bull with significant concerns. I am hopeful that it will be able to get its BLA back on track. If it fails to do so its path to recovery is beyond speculative. I am rating it a hold at its 12/26/2020 price of $2.54. It has been a horrible investment losing some ~65% compared to the S&P 500 over the last year.

Bulls need some positive news. Examples that are reasonable to anticipate/hope for include:

- news that it is in line for the $200 million from Rayner,

- a significant break in FDA intransigence on its BLA;

- a collaboration deal on one of its pipeline assets.

Be the first to comment