Love Employee/iStock via Getty Images

Introduction

Olink (NASDAQ:OLK) is a Swedish company developing a range of protein analysis tools and services. The company is young, but expanding rapidly in a fast growing area of the healthcare market. While the share price may have fallen after an IPO in 2021, a six-month bull trend led to 60%+ returns. With a higher valuation, Olink has announced dilution to raise new funds. These funds will allow Olink to continue operating as they have yet to become profitable. Fret not as the dilution and losses currently seen are supporting strong execution and I believe Olink will become profitable in the future. As such, I believe Olink is worth consideration for investors looking for a high growth play on the blossoming proteomics industry.

Olink JPM HC Conference 2023 Presentation

Olink’s Take on Proteomics

Proteomics is the study of proteins, the complex molecular building blocks of life. Many diseases involve proteins, and understanding them is of importance. In fact, the pandemic pushed the industry to the forefront of healthcare as the industry grappled with the shifting protein structures of COVID-19. However, infectious diseases are not the only treatment area at play, and Olink’s products can serve the entire growing industry.

Olink JPM HC Conference 2023 Presentation

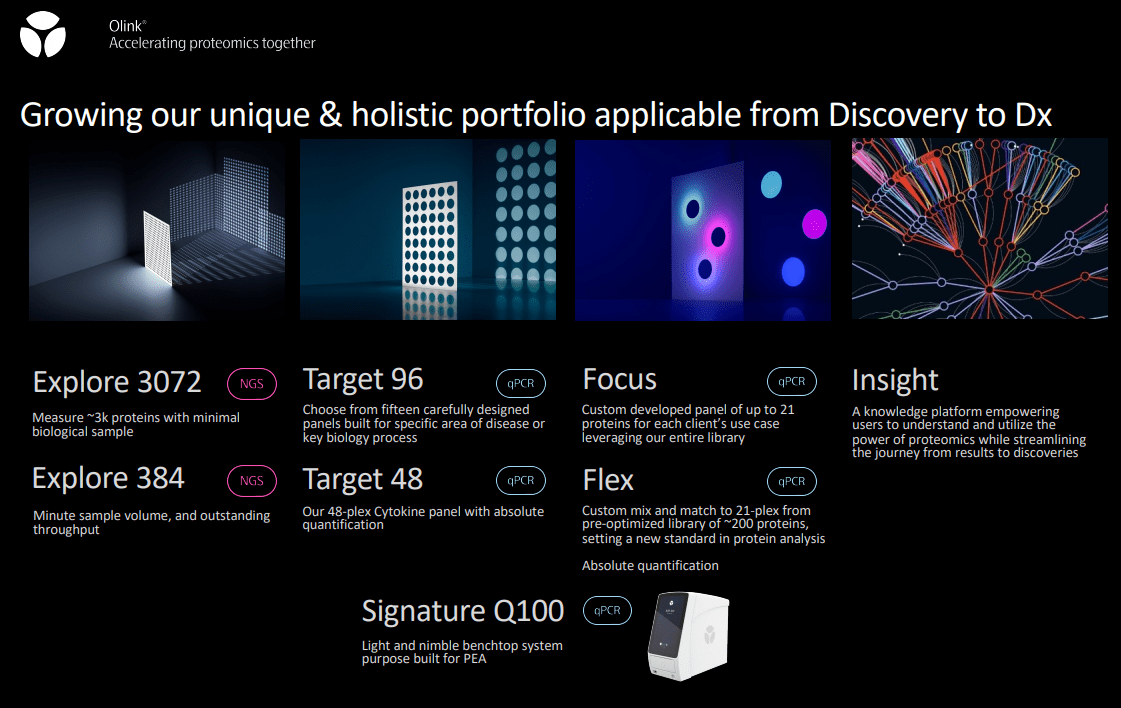

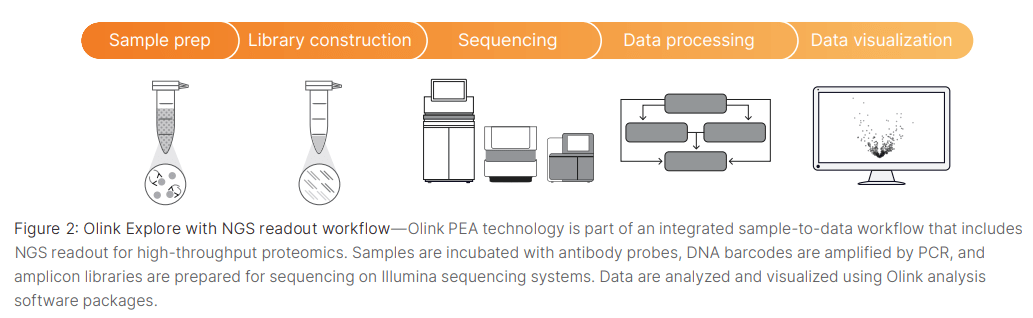

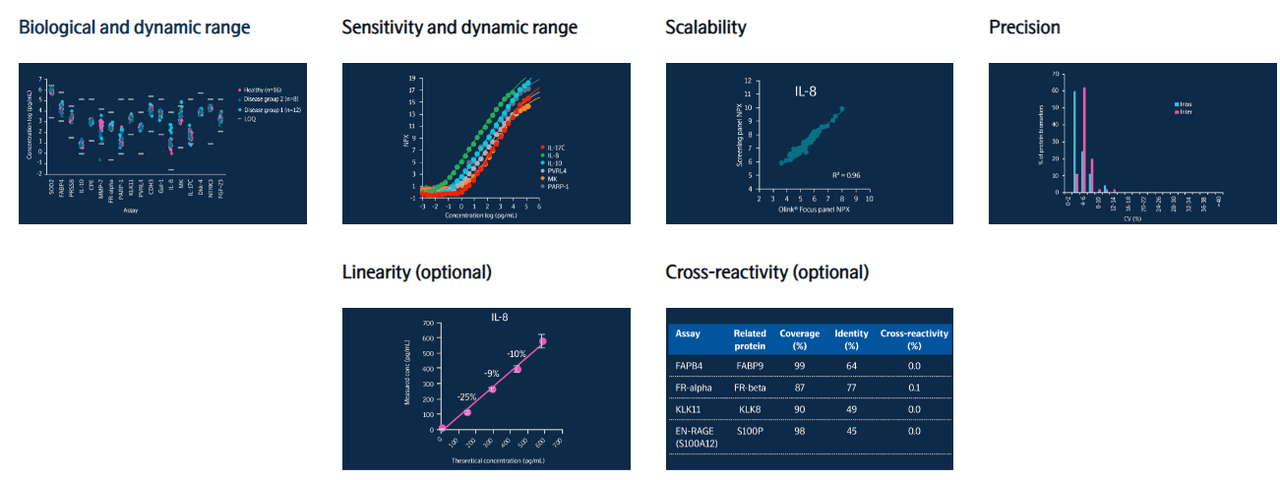

One of Olink’s platforms is the Explore range of products that are based on Illumina’s (ILMN) next-generation sequencing (NGS) technology. However, NGS is based on DNA sequencing, rather than proteins, so Olink’s proximity extension assay (PEA) technology ties the two fields together. Essentially, PEA tags proteins in a sample with DNA-marked antibodies that can be amplified and then sequenced. This is to avoid the difficulties in directly amplifying and sampling proteins on their own.

The final goal is to determine what proteins are the most expressed in an individual or group of samples. The Olink Explore 3072 is the most advanced tool at the moment due to having a diverse library of thousands of protein targets, whether intracellular, surface, or secreted (other platforms are currently surface protein only according to Illumina fact sheets).

Illumina

Olink also has other PCR-based platforms that begin to narrow the focus of PEA technology to individual areas. In particular, they allow for targeting proteins related to particular diseases or biological function. Essentially, Explore finds what disease or issue may be evident based on groups of proteins, and the PCR solutions dive into finding known biomarkers based on various Olink-provided kits. PCR then allows a far wider variety of visualization and analysis to drive actionable conclusions for drug discovers, researchers, physicians, or patients. The premier offering is the Focus range, and as the Olink website states, the difference between each platform is key:

While our standard offer of Olink® Explore 3072 and Olink® Target 96 panels provides an ideal broad screening-to-targeted discovery solution, our custom panel development [Focus] enables customers to take the next important steps towards protein biomarker validation and implementation.

Olink Website

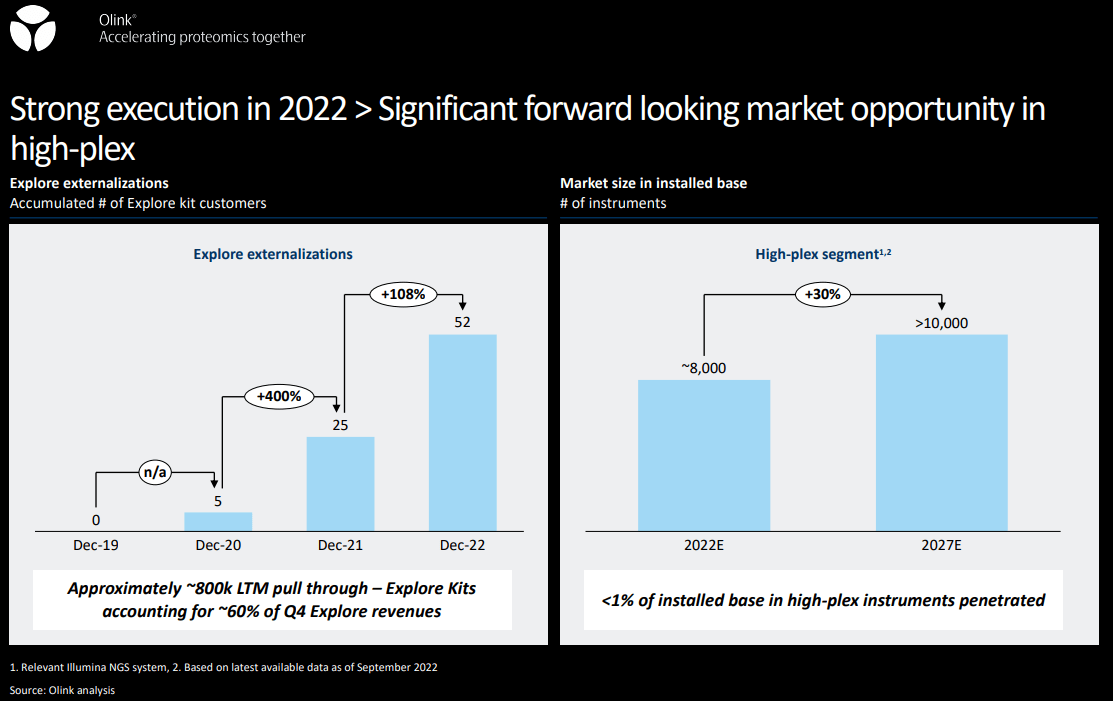

For all product groups, Olink gains revenues from hardware, software, consumables, and services. Having the fully integrated suite allows Olink to self-sustain growth without relying on other companies. However, as stated, Olink works with a variety of partners in order for their technology to work, whether it’s the NGS platform by Illumina or consumables from Beckman Coulter (DHR). This should not be a problem at this point as Olink is a new market entrant and management states they have less than 5% penetration of available Illumina workstations, just as an example of the organic growth opportunity.

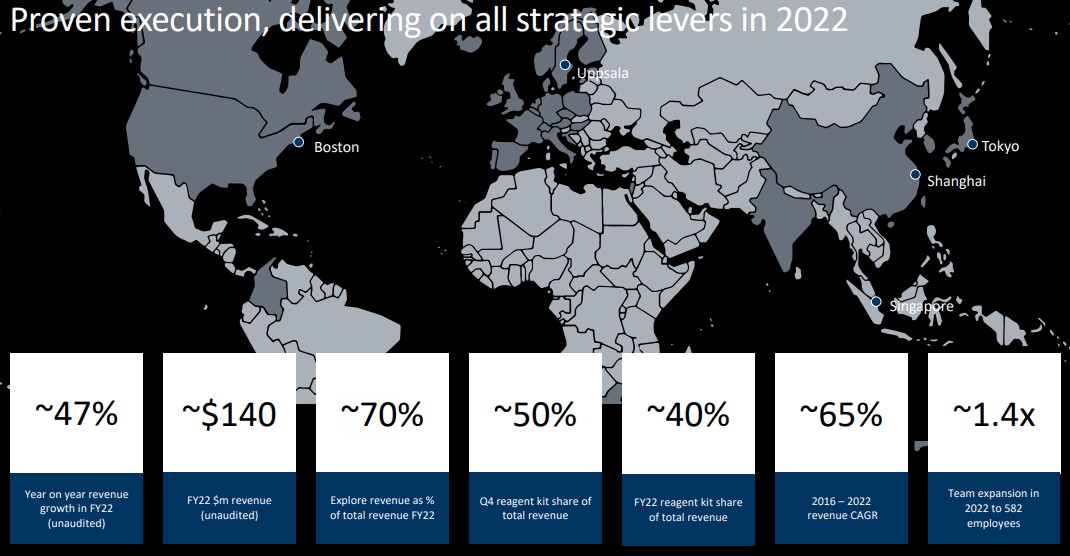

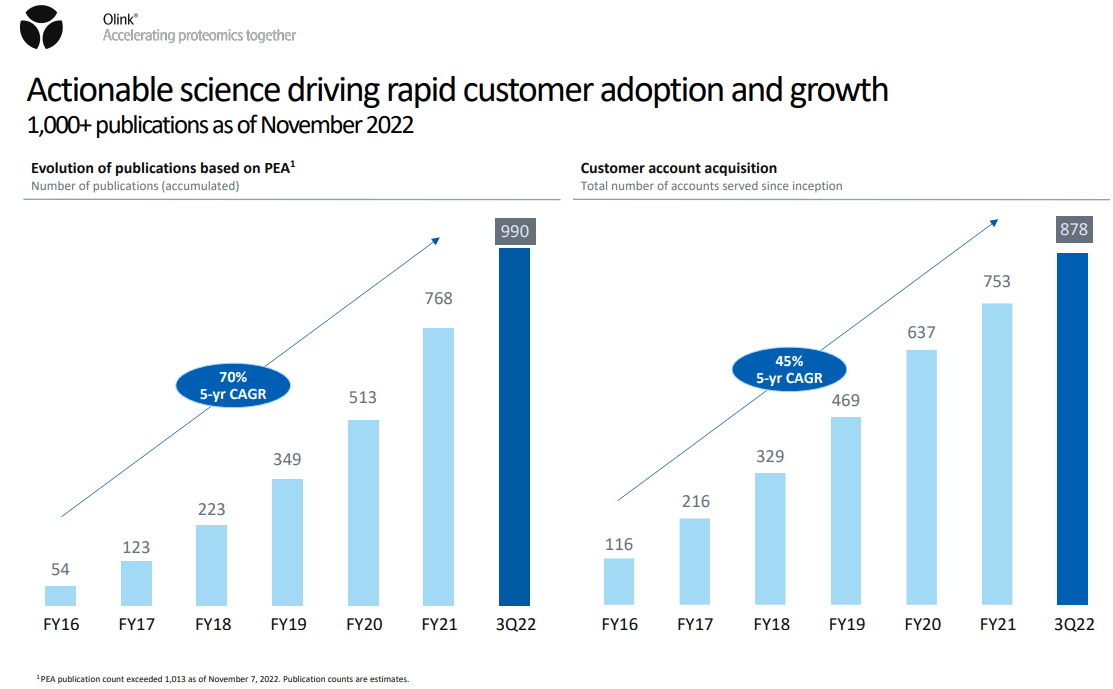

For now, Olink will focus on getting their own hardware out to labs across the world, and then use services and consumables to drive growth upon market saturation. This means growth will remain elevated for at least a few more years as the proteomics industry just gets started. One growth measure is through the number of publications that utilize Olink’s PEA technology, and these are growing over 50% per year. Also, the number of customer accounts is growing at approximately 45% per year, suggesting the growth opportunity remains.

Olink JPM HC Conference 2023 Presentation Olink 22Q3 Investor Presentation

Financial Implications

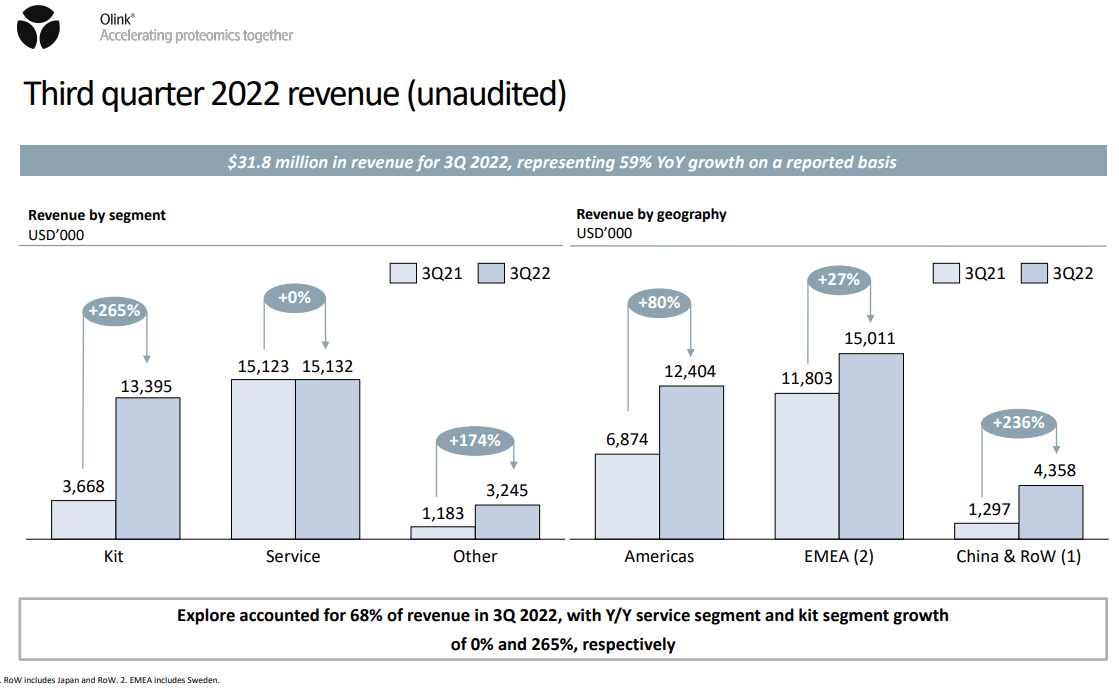

Olink’s current goal is to manufacture and distribute their platform equipment to the market as fast as possible. This has allowed for significant organic revenue growth over 50% YoY to $31.8 million for the quarter, despite economic weakness from inflation and other high costs. The explore platform is the main growth driver at the moment as kit sales increase over 200%. The weakest area is overall growth in the EMEA region where Olink is based and saturated, but Americas and RoW sales are picking up the slack. It is also important to note that Olink is still not profitable on an EBITDA basis, so organic growth remains the key financial indicator.

Olink 22Q3 Investor Presentation

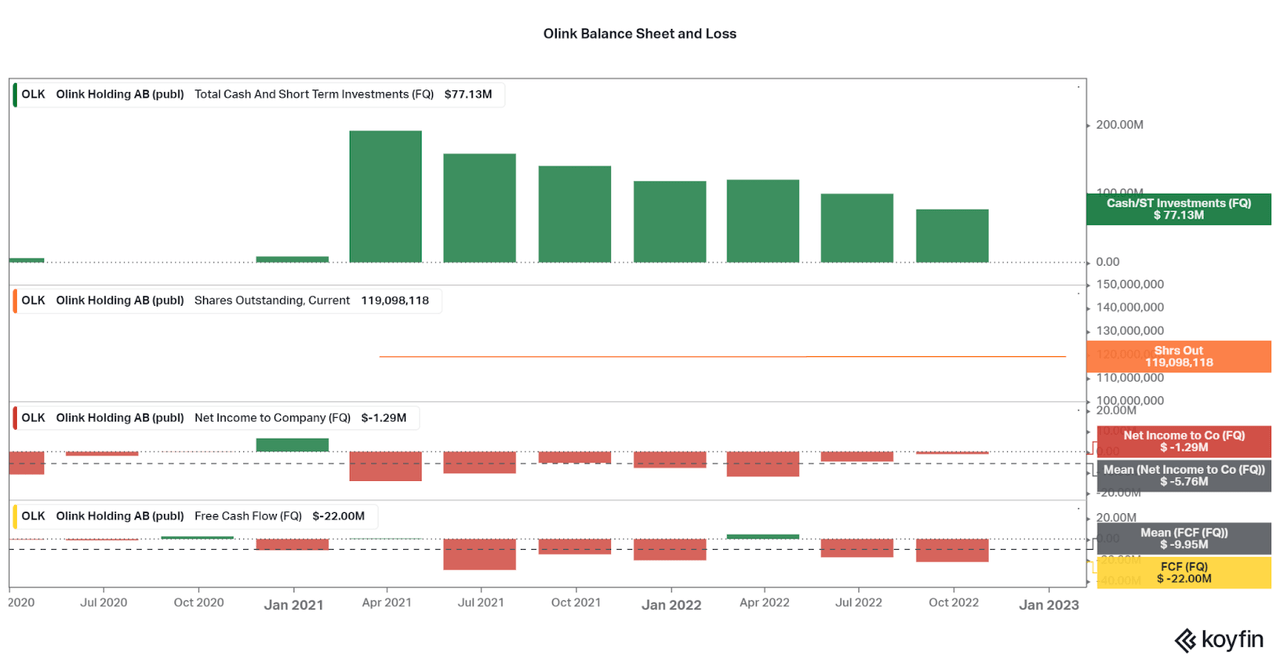

As losses remain present, it is important for Olink to have the resources on hand to sustain operations. After an IPO in 2021, Olink gained ~$200 million in cash and this has fallen to $77 million. Average net income loss per quarter is $5.75 million, while FCF losses are higher at $10 million per quarter on average. This suggests that Olink can support an additional two years of operations. This is why the recent announcement of a public offering of an additional 5 million ADR shares, or 4% of shares out, was not unforeseen.

The offering equates to over $85 million in potential cash based on company shares, not selling shareholders. Shares of Olink sold off by 16% as investors consider the dilution implications and frown upon the low $20 asking price per share. However, investors should be happy that Olink is generating cash to support their growth, and the short-term dilution will likely not hamper total return in the years to come.

Koyfin

Valuation

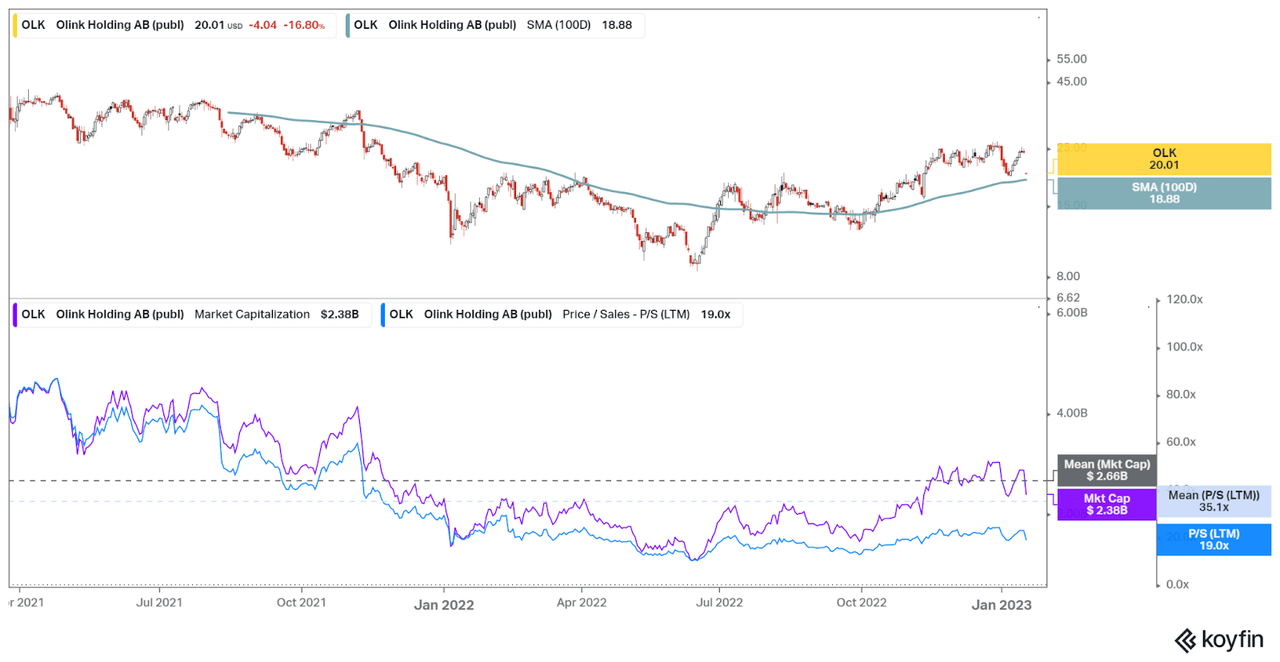

Despite the 16% fall, Olink’s share price and valuation remains far above lows seen last fall. The market cap is now at $2.4 billion compared to an average post-IPO market cap of $2.6 billion. The price to sales looks more realistic as the current 19.0x ratio looks better than the post-IPO average of 35.1x. However, as a speculative, loss-producing company, volatility will be an issue. Therefore, I believe that timing the potential drawdowns will be difficult, and the 100 day simple moving average may be a good momentum indicator for a flat trading pattern. For me though, I believe that slowly accumulating shares over time will fare far better for investors, as Olink has the opportunity to become a major Lab Analytical Tools provider in the coming years.

Koyfin

Conclusion

I recently ranked the top Laboratory Analytical Tools companies and found that an issue with the larger market cap peers is that they lack exposure to organic growth trends. This has led to numerous acquisitions of smaller, innovative tool makers like Olink. I suppose that Olink has a high valuation, but strong IP, so the potential for an acquisition may be low. However, the partnership with Illumina seems like the key influence, and investments or a purchase may be possible due to Illumina’s large size.

As a standalone investment, Olink offers strong qualitative factors that support the growth opportunity, but losses and a high valuation will create volatility in the coming years. Therefore, the investment is speculative so having a long-term mindframe is key. If profits can be found over the next 1-2 years, I believe the current valuation is fair and investors will be quite happy. As developments arise, I will be sure to update.

Thanks for reading.

Be the first to comment