JHVEPhoto

Dear readers/followers,

Olin (NYSE:OLN) is a chemical company with a great business. It’s volatile, as many basic materials companies are, but the key to handling that volatility is knowing where the company can go, and where it typically goes. That’s how I’ve been handling my investment in the company. A relatively small position for the time being, but one I slowly intend to grow as things move forward.

Chemical businesses are a big thing for me, with names like BASF (OTCQX:BASFY), LyondellBasell (LYB), Dow (DD) being part of my portfolio to various names.

So, let’s see an update for Olin here.

Olin – Updating on the company

So, chemical businesses. Olin is one – and a good one, even if there are significant drawbacks to the company. These come in the form of a poor yield and poor fundamentals in the form of a somewhat sub-par non- IG-rating. Also, remember – that dividend isn’t really going anywhere, because it’s not really growing – at least not for the past few years.

But the positives are significant as well. Over a century of solid history, revenues are in the billions. What’s more, the company gets its revenues from things like chlorine, sodium hydroxide, copper alloys, epoxies, and vinyls. The company also does ammunition and rifles in the Winchester segment, basically as sort of a VAP. How volatile do we think this is? There is volatility in the company, but these products, even if there is ups and downs, have resilient, underlying demand.

Olin is one of the world’s largest producers of EDC, which is a chemical precursor of PVC.

Its ammunition business also doesn’t come from nothing, as Olin’s historical business was in part supplying coal mines and quarries with explosives – so Olin can be said to have been in that business for 120 years. It’s a global producer with facilities in Germany – of course working against the company at this time due to electricity prices and similar issues.

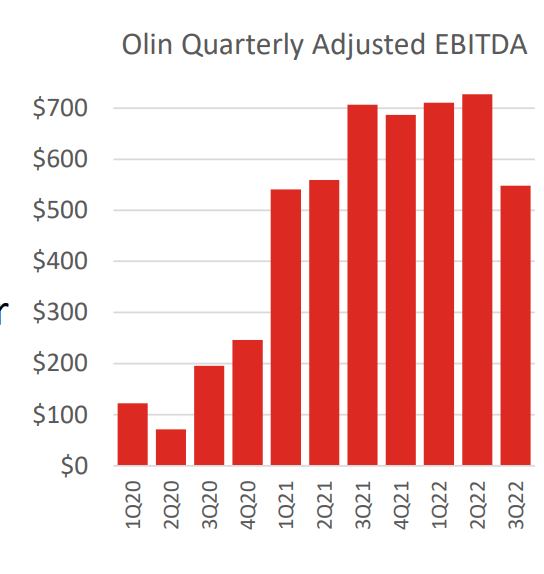

The company has a massive backlog that it’s working through, and the current trends have seen impressive improvements in EBITDA due to pricing – and this is despite low sales and volume in epoxy. This story has basically been confirmed as of the latest quarterly.

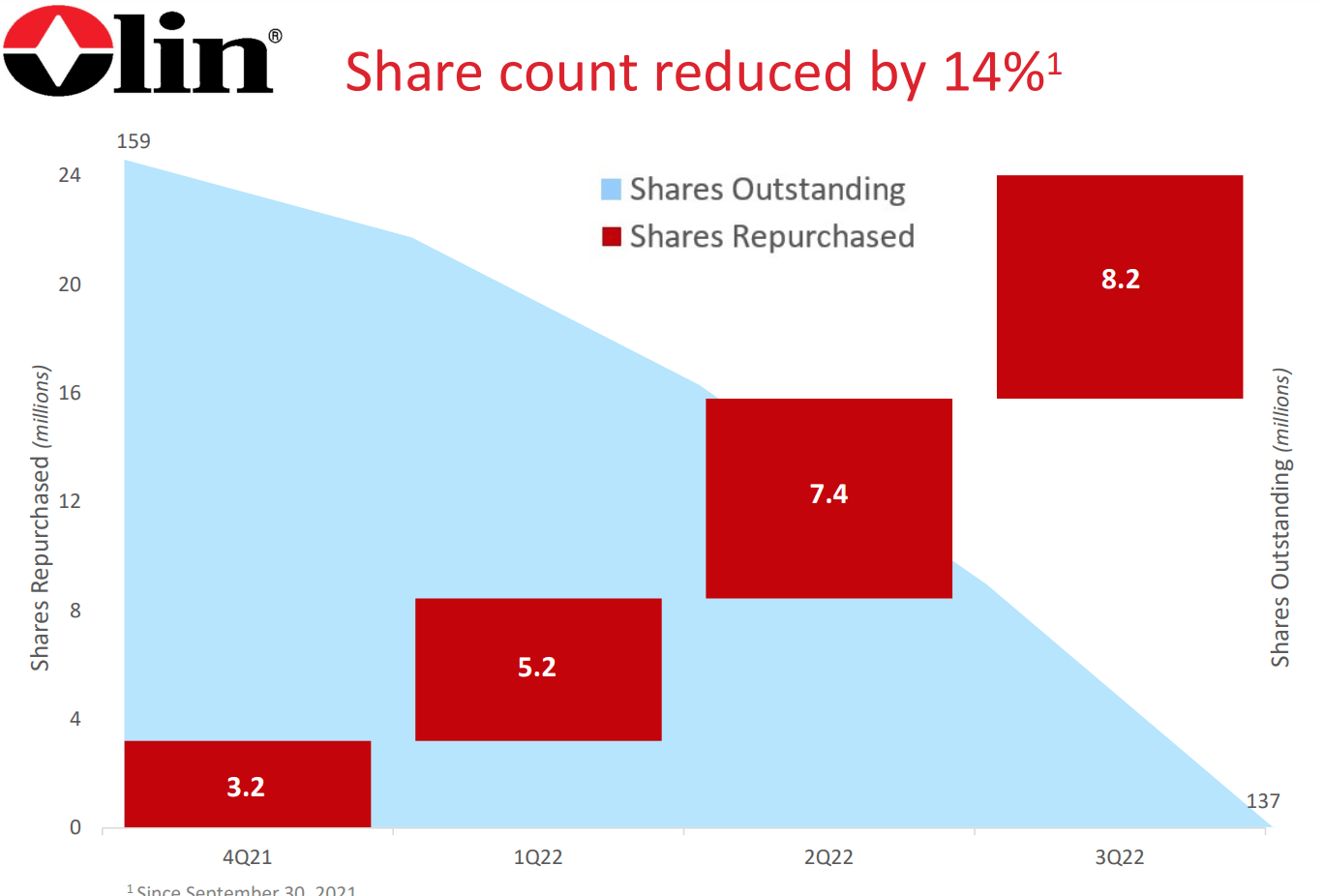

3Q22 saw improvements in pricing for chlorine and caustics, with even lower volumes and participation for EDC and Epoxy. The company also enjoyed high sales due to shooting sports participation, which enabled the company to buy back 6% of its outstanding shares. For the next quarter, the company is also forecasting further improved results in chlorine and caustics, with lower results in mostly everything else due to seasonality.

Olin IR (Olin IR)

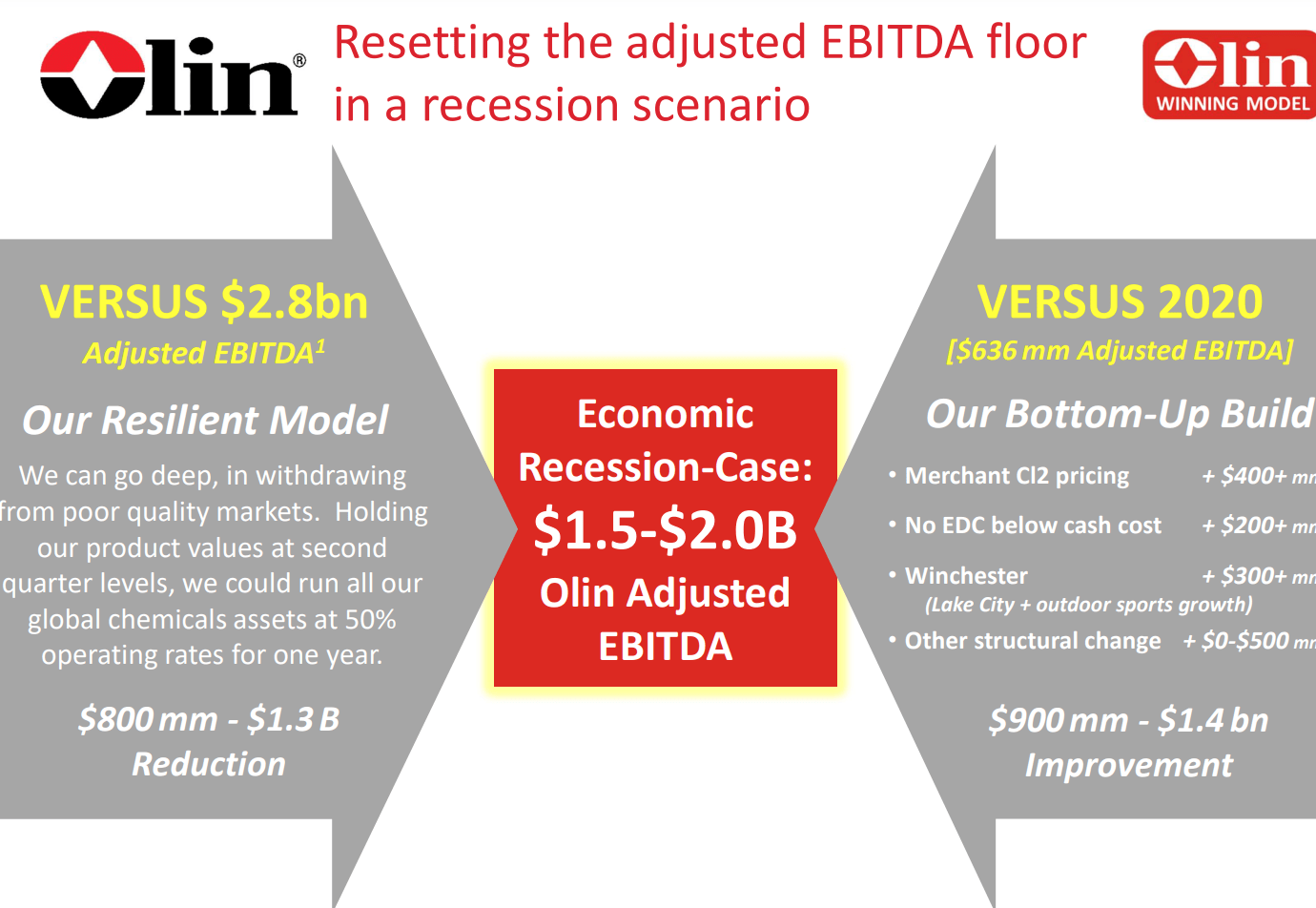

Even in the case of a recession, which seems not unlikely at this point, the company’s levered FCF is forecasted above $1B – and the uses for these is going to be share buybacks as well as shareholder dividends in the form of the company’s dividend.

The share count has been reduced by 14% in less than a full year. This is some amazing progress on part of the company, taking advantage of its cash-flow heavy trends as well as the current volatility in the market. While my position in the company is small, it has paid off considerably already.

OLN IR (OLN IR)

What is perhaps more important is that Olin is fully prepared for the recession. The company has a current leverage that below 1x, and a non-recession FCF that’s above $1.5B for the year. Olin has managed to cut its debt, and only 30% of what remains is floating/variable interest. The company’s available liquidity has improved to over $1.5B, enough to cover the company’s expenses and business for the foreseeable future.

Furthermore, history proves that a recession does not de-rail Olin’s cash flows completely. The company has the ability to generate meaningful amounts even during downcycles, and its adjusted capital spending plans and asset management has prepared it well.

The company is even prepared to use share price troughs to keep reducing shares outstanding – the main method it delivers returns to shareholders at this particular time. It’s close to IG at BB+, but more importantly, the share price in no way reflects the current earnings trends, with over 800% improvement in 2021, and expected flat earnings trends for 2022. The company is currently expected to see about a third of a drop in EPS for the next fiscal – my own forecast is around 30% in the case of a recession, but this would still be a very good level compared to where the company was before.

The company views its balance sheet as ready for IG – and having gone through it, there are many companies that have IG, that have worse balance sheets and higher debt than does Olin. From that perspective, their goal of moving to IG makes sense, and is realistic, even if the potential leverage moves to 1.2-1.7x here for 2023.

OLN IR (OLN IR)

The pricing trends for every single chemical that Olin sells is improved or stable – with the exception of EDC. Caustic Soda has seen two separate price increases in less than 3 quarters.

Full-year results come in with the following forecasts. Capital spending is going up, and expenses overall are expected to be up for the year, or similar (as in the case of environmental expense).

The case I want to present here is that even in the case of a realistic recession – again, I expect this in the next year – things are looking good for the company, even in the worst of cases. And if the company drops backs down to trough, I’ll be buying more.

The fundamental investment cases for Olin have not shifted one hair since my last article.

What are they exactly?

- The company is virtually in a market-leading position in every business it has.

- It has superb trends across cycles.

- The free cash flow yield, on a levered basis, comes out to over 20% – which is amazing.

- The market, due to a mix of low yield, low credit rating and low DGR, has a recorded trend of significantly undervaluing Olin, meaning triple-digit return potential if bought at the right price.

So here’s my updated thesis on Olin.

Olin – The updated valuation

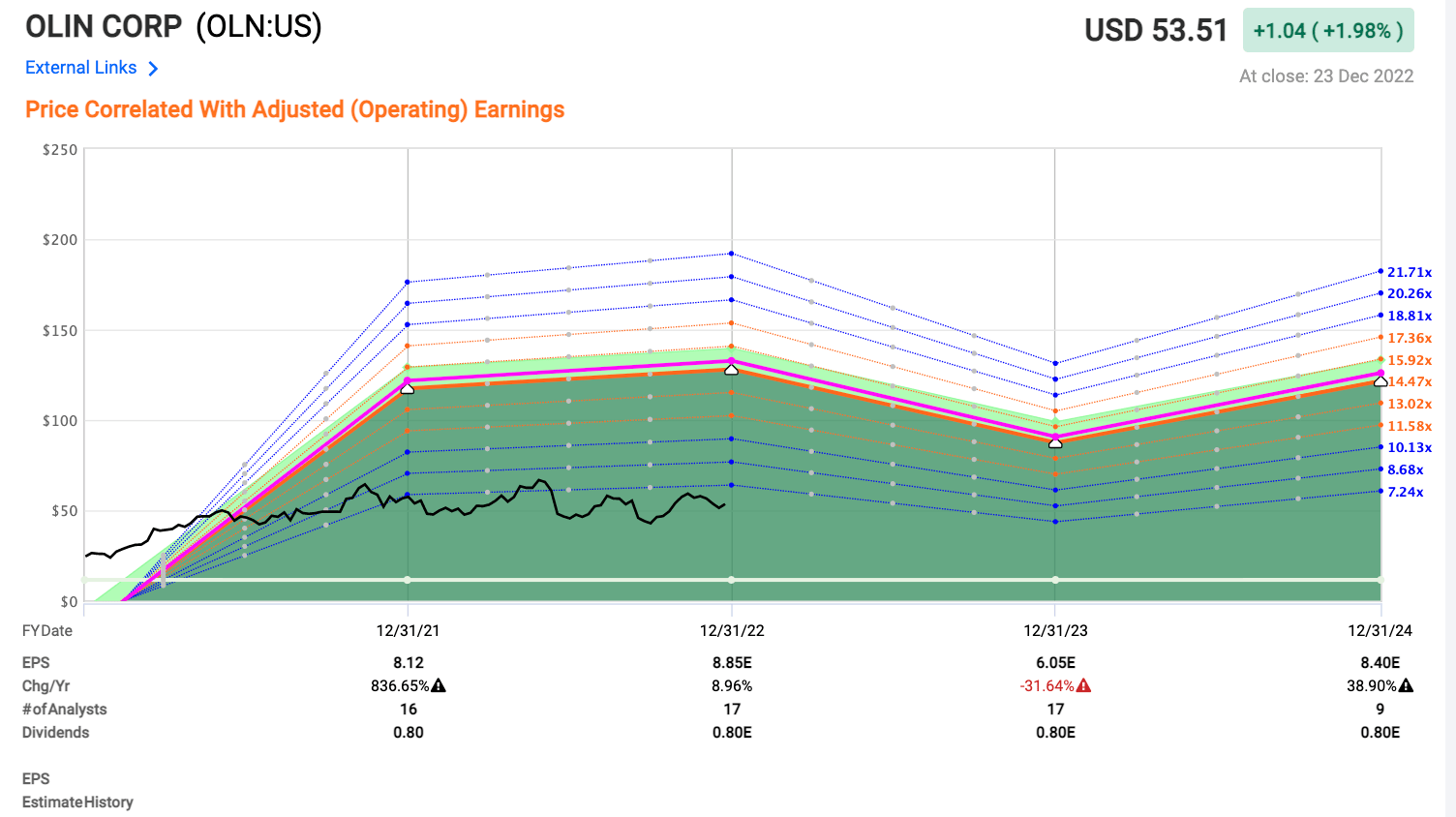

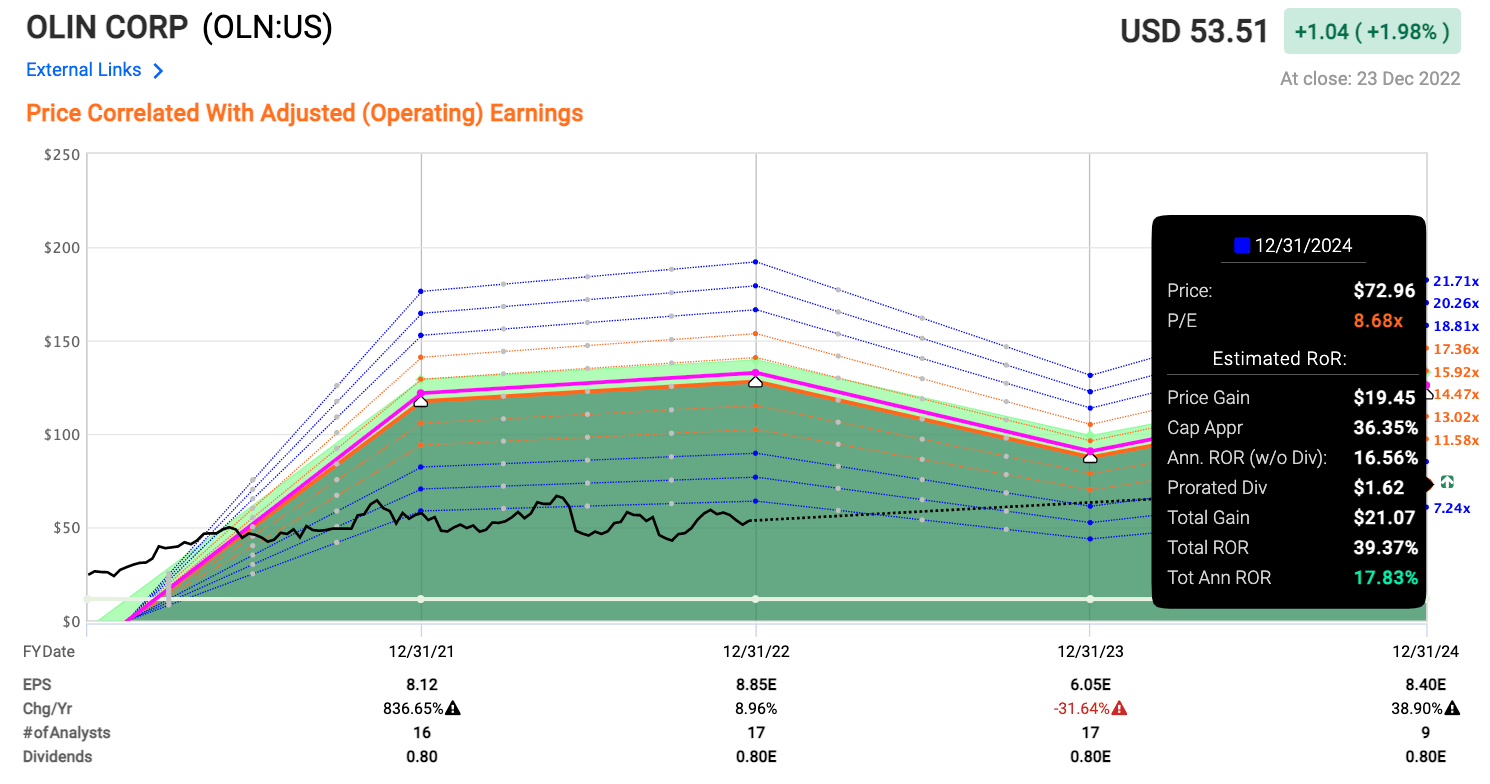

The improved earnings levels mean that the relative valuation remains excessively low here. The company has already proven that it can deliver high earnings in 2021, and the quarterly earnings are in line to deliver solid results for 2022E as well.

Even a 2023 dip wouldn’t necessarily derail things here.

OLN Upside (F.A.S.T graphs)

You can see that the market has a hard time deciding where to value the company in this new earnings reality here, which is significantly higher than it has been before.

The more often we see the positive quarterly results we’re seeing from Olin, the less ambiguous the results, forecast trends, and uncertainties get. Simply put – with every positive or decent quarter, my confidence in the company rises.

Even on a 10-13x forward P/E, the company will, based on current forecasts, rise, and deliver RoR well into the double digits. Forecasting it at a level below 9.5x wouldn’t be feasible, and the potential RoR here looks like this.

OLN Upside (F.A.S.T graphs)

As I also mentioned before, there are plenty of catalysts for the company to rise in the long-term here. The shift to any kind of BBB-rating would be major, and the company seems on track to improve here given the latest 4 years. If the company hits its targets, even the somewhat lower one, I expect stability or growth here as well. There’s also the potential that the company might bump the dividend once its buyback ambitions are fulfilled. The reason is that the current level is extremely low, all things considered, given earnings.

The current average target for Olin based on current S&P Global averages come to around $63 – this is also a pretty fair average over the past 12 months, with no lower PT than $49, with a high-end range of $88/share.

Out of 14 analysts following the stock, 10 have either a “Buy” or an equivalent bullish rating on the company. That’s an 18%+ upside, conservatively – and its one I don’t consider to be unlikely here.

The lowest forecast level is very close to today’s valuation, while expecting things to normalize to lower levels, resulting in a relatively flat RoR over time. However, as I said, if the company retains its new EPS level and slight growth rate, I do expect Olin to start normalizing to these higher levels, resulting in massive outperformance.

The company’s issues dictate that Olin requires a cheap investing level. We still have that level. In my latest article, I put the company at my PT of $65/share. I won’t shift from this target here, because I rarely shift my PT’s. At least not without very good reason – and that isn’t what we have here.

Thesis

- I’m sticking with my Olin thesis, which is bullish, and I stick to my PT for the company, which has been set for the past few articles. I consider the company to have performed very well.

- There are at least 2 not-unrealistic catalysts for an upside here, beginning with a bump in credit, to a bump in dividends – and even without this, there are things to like about Olin.

- I’m holding to my $65 PT, but I’m firming up my “Buy” here.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized). But in this case, note that the fundamentally safe is with a * due to the BB+ rating.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.*

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Be the first to comment