Jonathan Kitchen

The S&P and other US indices have been rallying quite aggressively these last few weeks after the recent Fed meeting and the unemployment results. We are quite surprised by the market reaction, and think that the news points to the downside rather than the upside. Moreover, prices are nearing a recovery to pre-invasion levels. While there might be speculative reasons for this being a fair position, we still think that ETFs that follow the S&P, including the iShares S&P 100 ETF (NYSEARCA:OEF), have rallied prematurely. US investors should be concerned about the near and medium term direction of their indices.

S&P View

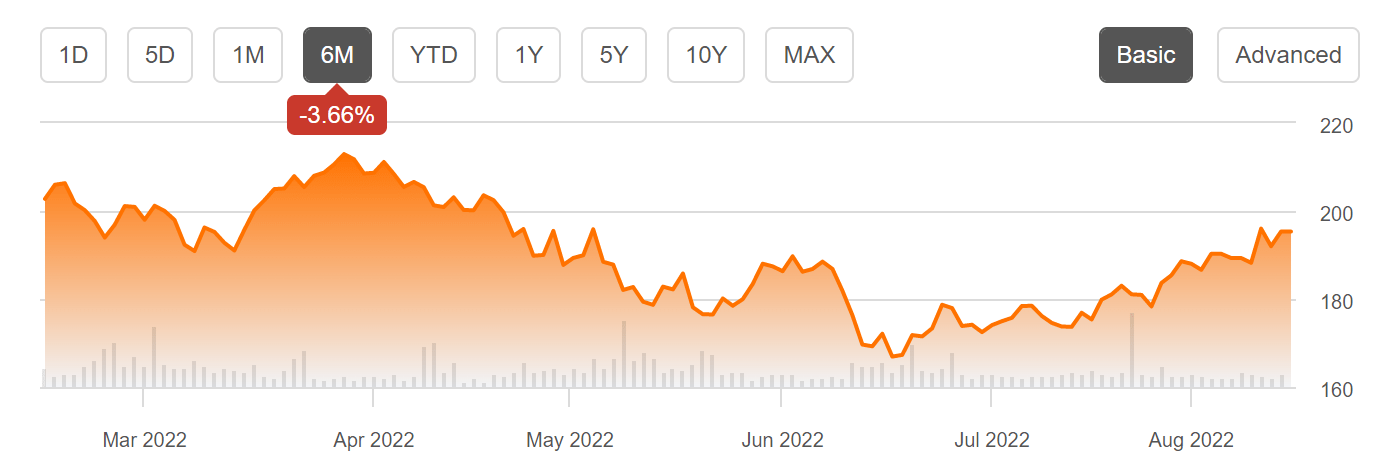

Looking at the OEF’s price data, we see quite a meaningful recovery from the June lows.

OEF Price Movements (Seeking Alpha)

Over the least six months, declines have been very limited in actuality. In fact, we are looking at a period that begins before Russia invaded Ukraine. This mirrors the movements of the SPDR S&P 500 ETF (SPY) exactly, which has also recovered meaningfully and is only awaiting a 5-10% cumulative spurt before it recovers to pre-invasion levels. The SPY and the OEF only differ in terms of depth: the OEF has the first 100 largest companies in the S&P, but since they dictate so much of the market cap of the US market, they are the ultimate drivers anyway.

Developments

Why would such a recovery be premature? The first reason has to do with market composition and potential market risks. Technology is a big part of the US market, and while corporate technology like cloud has done really well, and in general corporate spending has been keeping up, consumer facing segments or whole companies have been seeing hits. There is a clear bifurcation between corporate facing and consumer facing businesses, where corporate facing businesses are faring well for the moment on corporate optimism while consumer facing businesses aren’t. Simply put, consumer pessimism will eventually pass through to corporations. When this happens we may finally see the rate hike hit to employment, at which point macroeconomic contraction will begin in earnest.

Conclusions

The biggest concern we have is the quantum of the recovery and how it compares to pre-invasion levels. The invasion has unraveled important threads of cooperation and that has definitively destroyed economic value. That has been seen in cost-push inflation. Unless you’re sure that the majority of the inflation right now is being driven by speculative forces, i.e. traders and terminal owners hoarding product, and not by good-faith limits on resources, bidding the markets up to pre-invasion levels seems optimistic. Having noted this ourselves we weight more to European markets right now if we were to take a market index overall. Although in the current environment, investors are rewarded for being active and selective.

While we don’t often do macroeconomic opinions, we do occasionally on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment