bjdlzx

(This article was in the newsletter on August 19, 2022.)

The question with Occidental Petroleum (NYSE:OXY) is when the game ends will you have a seat? For Warren Buffett, meanwhile, the bigger question is why Occidental Petroleum was not a buy at $10 but is a buy now at several times the price. What changed so much that Occidental is now cheap at a far higher price? But the musical chairs crowd may not care about the question. They are more excited about the game and its speculative possibilities. There are all sorts of theories about how to win big on this one while the music is playing.

But Warren Buffett, through Berkshire Hathaway (BRK.A) does not have to play the game the way the musical chairs players envision. This is why it is so important to make sure you have a safe landing (a chair) when the game is over. The purchase of common shares by a major shareholder can stop at any time. Furthermore, there is nothing preventing that shareholder from selling in the future (except a certain reputation for not selling). This is why the reason to buy the stock at the current price has to be sound in its own right. Otherwise, the risk of loss in following a large buyer can be more than meets the eye.

Still, the market likes a good story and there is no better story than a rising stock price.

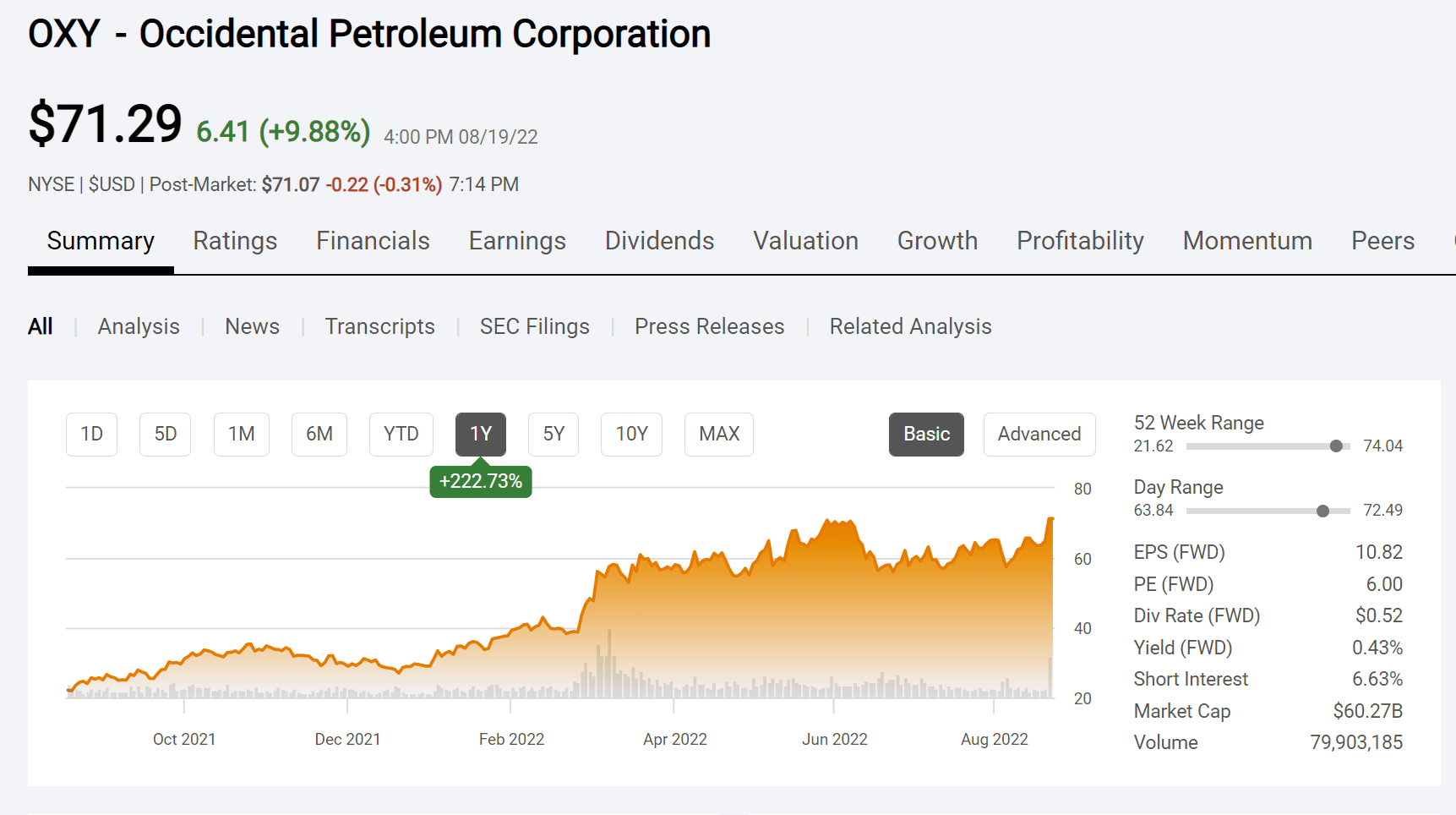

Occidental Petroleum Common Stock Price History And Key Valuation Measurements (Seeking Alpha Website August 19, 2022.)

Just in the short time shown above, the stock price has about tripled from its lows. If one goes back to the nadir of fiscal year 2020, the stock price performance is even better. When it comes to the idea of market efficiency and perfect information, this really should not be happening. The decision by one person to purchase stock in a company does not materially change the outlook of the company.

Furthermore, an agreement to allow a major shareholder to purchase up to 50% of the shares outstanding is just that: an agreement. There is no promise to buy a single share more and there is always a risk that beginning tomorrow, no more shares will be purchased. If the buying ends without a speculated complete buyout of the company, then what will the company be worth in the eyes of the market?

Finances

Occidental is a company with a lot going for it. Then again in this market, most energy companies are looking healthier than has been the case probably since 2014.

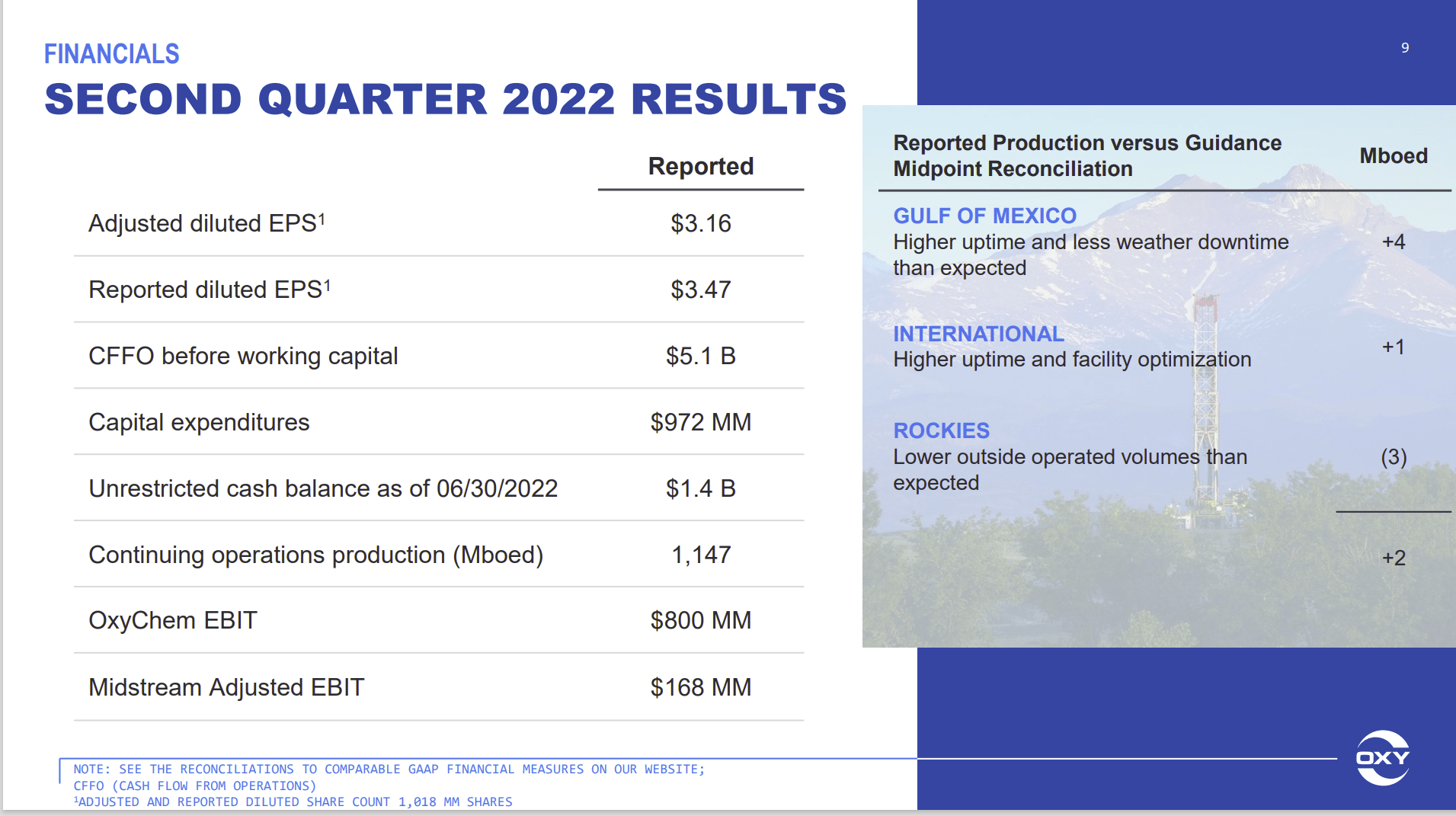

Occidental Petroleum Second Quarter 2022, Earnings Conference Call Slides Showing The Second Quarter Financial Summary. (Occidental Petroleum Second Quarter 2022, Earnings Report Materials.)

One of the things that the market clearly “never saw coming” back in fiscal year 2020 was the effects of the low oil prices on the future balance between supply and demand. Admittedly, the war magnified the situation. But as I covered the industry, so many managements were concerned what the future would look like that they hedged at what turned out to be very low prices compared to what happened.

Demand “snapped back” so fast in so many areas including oil and gas that it completely took the world by surprise. We had never been in a pandemic before and had no idea what the recovery would look like. So, the situation in fiscal year 2020 and 2021 was navigated as best as anyone could figure out. Clearly all those managements that hedged production were worried about a weak recovery or one that would take “two steps back for every step forward”.

More importantly, the unconventional business is known for wells that have a steep production decline in the first year and a significant decline in the second year. In fiscal year 2020, those declines were not matched by replacing production. So that led to one of the bigger industry wide production drops on record. When that is combined with a demand that was growing through the pandemic (which is what appears to have happened). A sizable mismatch between production and demand developed.

Add to that a lending market that wised up to some of the more foolish lending practices by demanding that companies “live within their means”. Meanwhile the stock market demanded some cash for shareholders. The result is less money to reinvest in growth than would have been the case in the last couple of recoveries. The lending market also wanted more conservative financial ratios. So, the first year or so of the recovery would be devoted to “balance sheet repair”.

All of a sudden, the rapid growth that was a huge sign of the unconventional business now became a thing of the past. Once the balance sheet repairs of the past are complete, there will be more money to invest in growth and shareholder returns in the future. But the unsound lending practices that happened in the past will probably not happen in the future. The inexperienced “fast buck” money appears to be staying away as well because of past losses. So, things will be more orderly in the future.

That means that the second quarter results the company posted are likely to be repeated for some time to come. The market (as usual) underestimated the strength of the industry recovery. The only sources of capital and debt are sources that know this industry well. So going forward, the unconventional business is likely to behave like a mature industry than a new fast-growing idea for the “get rich fast” crowd.

The Future

What Warren Buffett likely sees is a very profitable company that can use the current commodity prices to reset the balance sheet. A few more results like the second quarter shown above, and the company will not have any financial leverage worries that plagued the company throughout fiscal year 2020.

Unlike economic theory, information is rarely perfect, and it is even less rarely available far into the future in this industry. Instead “group-think” is often an investment hazard.

Investors need to keep in mind that Warren Buffett is a big investor who often needs to make big purchases in order for those purchases to have a significant effect on the returns he reports to shareholders. When he is done buying (if he does not buy the whole company), the market will then come up with a valuation for the company into the future.

For the time being, the current price still appears to be a decent price for potential investors to consider. However, there is a risk of a price retracement once a major shareholder stops purchasing the stock. Warren Buffett often has a long-term time horizon. Mr. Market could have a dozen “fits of worry” between now and that time horizon that would shake individual investors to the core. So, it is wise for individual investors to have a complete strategy before they invest in Occidental Petroleum.

The chances of Warren Buffett ever selling are slim. But if any of my friends are an indicator, they can be talked out of their investment position before they make a reasonable profit because the stock unexpectedly went down. That “talked out of” part is what needs to be prevented before you get in because that often removes solid long-term profits from investors’ portfolios.

Be the first to comment