Eric Francis/Getty Images News

Occidental Petroleum (NYSE:OXY) has been one of Warren Buffett’s best investments in years. The stock, which Buffett has been accumulating since February, has risen 85% year-to-date. Buffett’s more recent OXY buys were above the current price, but given when he started buying, he probably enjoyed 50%+ gains on his earlier purchases. For Buffett, that’s not a positive, since he likes to accumulate cheap, but it will probably be seen as a positive by many Berkshire Hathaway (BRK.B) (BRK.A) shareholders, who presumably want to see stock prices rise.

Buffett’s OXY buys (Google Finance)

Buffett’s gains on oil and gas stocks this year have been well-publicized. In addition to the recent OXY buys, he also bought enough Chevron (CVX) to make it his fourth-biggest holding. That Buffett has made gains on these stocks is not in doubt: everybody knows that oil stocks are doing well this year.

The more controversial matter is whether Occidental Petroleum is still a buy. Unlike the giant Chevron, Occidental is not a household name. With a mere $54 billion market cap, it is a bit player compared to the oil and gas titans. This means that making an informed investment in Occidental Petroleum takes more due diligence than does an investment in Chevron, as you do not have ready access to as much “Scuttlebutt” in OXY’s case. With a company like Chevron, you can get regular clues as to the company’s performance just by going outdoors and checking out Texaco prices and traffic levels. OXY’s operations are not quite as visible in the world, and therefore its success is less obvious.

Nevertheless, OXY is in fact succeeding. Its revenue, earnings and cash flows are up dramatically this year, and its balance sheet is in OK shape too. With a 4.44 ratio of price to operating cash flow, the stock is cheap even if we assume that oil prices decline. Finally, it has a smaller market cap than some of the big energy names out there, giving it more room for multiple expansion. On the whole, the company’s future appears bright, and Buffett’s investment in it is just one vote of confidence among many.

OXY’s Operations

To understand why Occidental Petroleum is so well-positioned right now, you need to understand its operations. OXY has three main business units:

-

Oil and gas.

-

Midstream.

-

Chemicals.

The oil and gas business is the one that benefits the most directly from the rising crude prices we’re seeing this year. This is the business unit that sells the crude oil OXY extracts. When oil prices rise, OXY’s revenue rises, and its profit margins widen. According to CEO Vicki Holub, OXY breaks even at $40 oil (WTI Crude). So, oil prices can fall considerably and the company’s oil and gas business will still be profitable.

Next up we have midstream. This business mainly ships Occidental’s own products to buyers, which helps the company save money. OXY also has a partially-owned midstream subsidiary, Western Midstream (WES), which transports oil and gas for other companies in exchange for fees. However, that business is in the process of being spun off. The midstream segment lost $50 million in the most recent quarter, although the equity income in WES was $159 million. On the whole, midstream is not OXY’s most profitable business unit, but it helps the company avoid paying for third-party midstream services.

Last but not least, we have chemicals. This segment produces industrial chemicals like chlorine, vinyl, sodium silicate, potassium carbonate, and others. This segment is profitable, with $671 million in earnings in the most recent quarter.

OXY’s business mix gives it some durable competitive advantages. The fact that it can transport its own oil and gas lets it capture operational efficiencies, and the chemicals business adds an additional revenue stream on top of its thriving oil and gas business. Compared to, say, a pure-play midstream company, Occidental Petroleum has significant operational diversification.

Financials and Valuation

Speaking of OXY’s businesses, we can now get into their financials.

In the most recent quarter, OXY delivered:

-

$8.5 billion in total revenue.

-

$4.67 billion in net income, up from the prior-year quarter’s loss.

-

$4.65 in EPS, also up from a loss.

-

$3.2 billion in operating cash flow, up 311%.

From these figures, we get a 54.9% net margin and a 37% cash flow margin – indicating solid profitability. The trailing 12-month figures also show solid growth and profitability, but to a lesser extent, because 2021 wasn’t as strong as 2022 has been so far.

Having looked at OXY’s recent earnings, we can now turn to its balance sheet. Occidental Petroleum’s balance sheet is, like those of many oil companies, pristine, boasting metrics like:

-

$74.2 billion in assets.

-

$49.3 billion in liabilities.

-

$24.9 billion in equity.

-

$10 billion in current assets.

-

$8.7 billion in current liabilities.

-

$25.6 billion in long-term debt.

From these balance sheet metrics, we get a debt-to-equity ratio of 1.02 and a current ratio of 1.14. These suggest decent liquidity and solvency. The balance sheet is probably the weakest part of the picture for OXY – long-term debt in excess of equity isn’t great, but OXY can use its enormous profits this year to pay down its debt. So, interest expenses should go down, and solvency should improve.

Now, let’s look at OXY’s valuation. Based on today’s stock price and trailing 12-month financials, we get the following multiples:

-

Adjusted P/E – 12.6.

-

GAAP P/E – 9.

-

Price/sales – 1.95.

-

Price/book – 2.5.

-

Price/cash flow – 4.44.

These are all rock bottom multiples. Even if you slashed OXY’s operating cash flows in half, they’d still only give a single-digit multiple at today’s prices. Of course, if oil prices fell enough, then OXY’s cash flows could fall by more than half. That’s most likely what has some people unconvinced by OXY stock. In the next section, I’ll explore the matter of oil prices, and what they mean for Occidental Petroleum.

Oil Prices

Oil prices have been responsible for much of Occidental Petroleum’s gains this year. Buffett himself called OXY a “bet on oil prices,” so naturally, prices are a big part of the bull thesis.

At the time of this writing (Tuesday afternoon), oil prices were trending downward. Crude oil had dipped below $100 for the first time in many months, and OXY stock had fallen right alongside it.

It’s only natural for oil stocks to correlate with the price of oil. After all, the higher prices go, the more money oil companies make. In a past article, I wrote that oil prices are likely to be pretty strong all year long. I still believe that, but there’s more to the story. Oil companies have a certain oil price they need to clear to make money; beyond that point, costs and production can influence profitability quite a bit. In OXY’s case, the breakeven oil price is $40 – few experts think we’ll go that low any time soon.

Furthermore, OXY stock remains cheap even if we assume prices go much lower than they are now. In the fourth quarter of 2021, WTI oil prices averaged about $75. In that quarter, Occidental Petroleum did $1.37 in EPS. Let’s assume that, tomorrow, oil prices crash to $75, and OXY only does $1.37 in EPS per quarter for the next 12-month period. That works out to $5.48 over 12 months. At today’s stock price of $57.69, that gives us a P/E ratio of just 10.52. So, OXY is still cheap by at least one metric even if oil prices fall to 2021 levels!

Risks and Challenges

As we’ve seen, Occidental Petroleum is a very cheap oil stock that will remain cheap even if oil prices fall to $75. That’s not even factoring in the possibility of oil prices rising again after the strategic petroleum release ends. There are certainly many things pointing toward OXY having a strong year. However, there are risks and challenges to keep in mind, as well. They include:

-

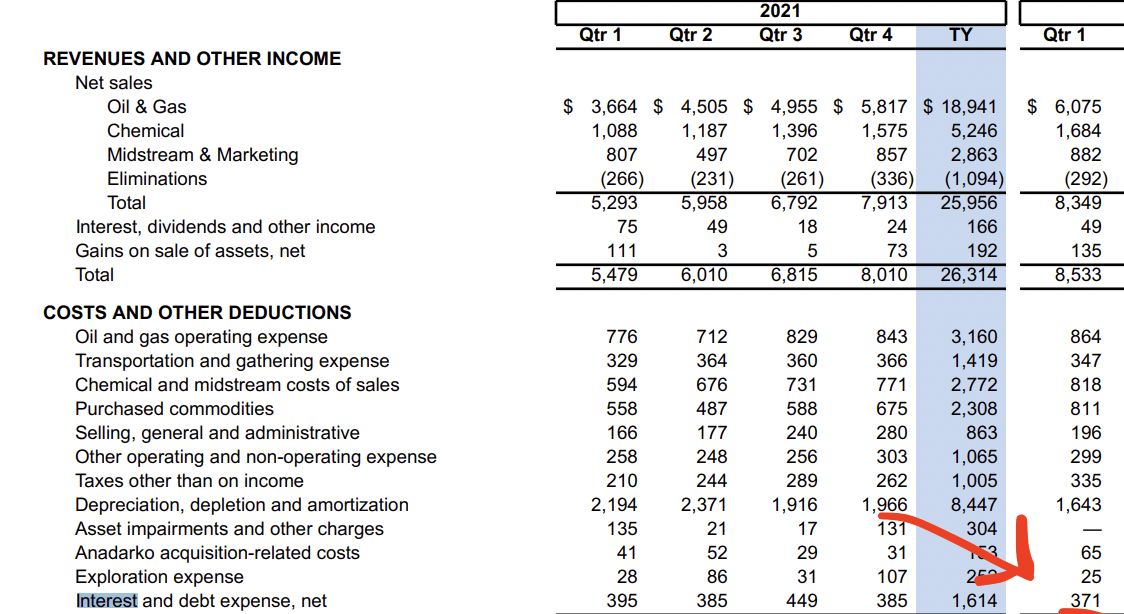

Debt. One thing that’s not as attractive with OXY as with other oil stocks is its debt level. At $25.6 billion, it’s currently higher than total shareholder equity. A debt-to-equity ratio of exactly one isn’t terrible, but it’s not amazing either. $25 billion in debt produces a lot of interest expenses, $371 million worth per quarter, to be precise. In addition to having to clear a $40 oil price, OXY has to clear $371 million in interest before it can turn a profit. So, the debt could be a problem if the price of oil goes down.

OXY’s enormous interest expenses (Occidental Petroleum)

-

Interest rate hikes. The Federal Reserve is hiking interest rates this year, hoping to get prices (especially oil prices) down. Inflation is a big concern these days, and the central banks are trying really hard to combat it. The higher interest rates go, the more expensive it is to borrow. That can lead to people spending less money on things like gasoline. So, the Fed’s interest rate hikes may take a bite out of oil prices this year. If they do, then OXY shares could go down, since the stock is highly correlated with oil prices.

The risks above are very real. If the Fed hikes interest rates enough to crater OXY’s earnings, then it could lead to issues with servicing the debt. However, there are enough reasons to think that oil will stay strong this year, too. The SPR release will end, and OPEC is running out of spare capacity. These two factors alone suggest that oil prices will be strong over the long term. So, there’s reason for optimism toward Occidental Petroleum, the latest big winner in Warren Buffett’s portfolio.

Be the first to comment