PonyWang

NVIDIA Corporation’s (NASDAQ:NVDA) shares are down nearly 60% year to date, and many hopeful investors believe the stock is forming a bottom. Where some feel the chipmaker will post a strong set of quarterly results to drive its shares higher, others are of the opinion that the stock is undervalued and is due for a major rally. But that doesn’t seem to be the ground reality. Latest channel sales data reveals that Nvidia’s Q3CY22 is shaping up to be an ugly quarter, which means its shares can potentially fall further in coming weeks and months. In this article, I’ll attempt to explain why this might not yet be the best time for bottom fishing. Let’s take a closer look at it all.

Monthly Sales Data

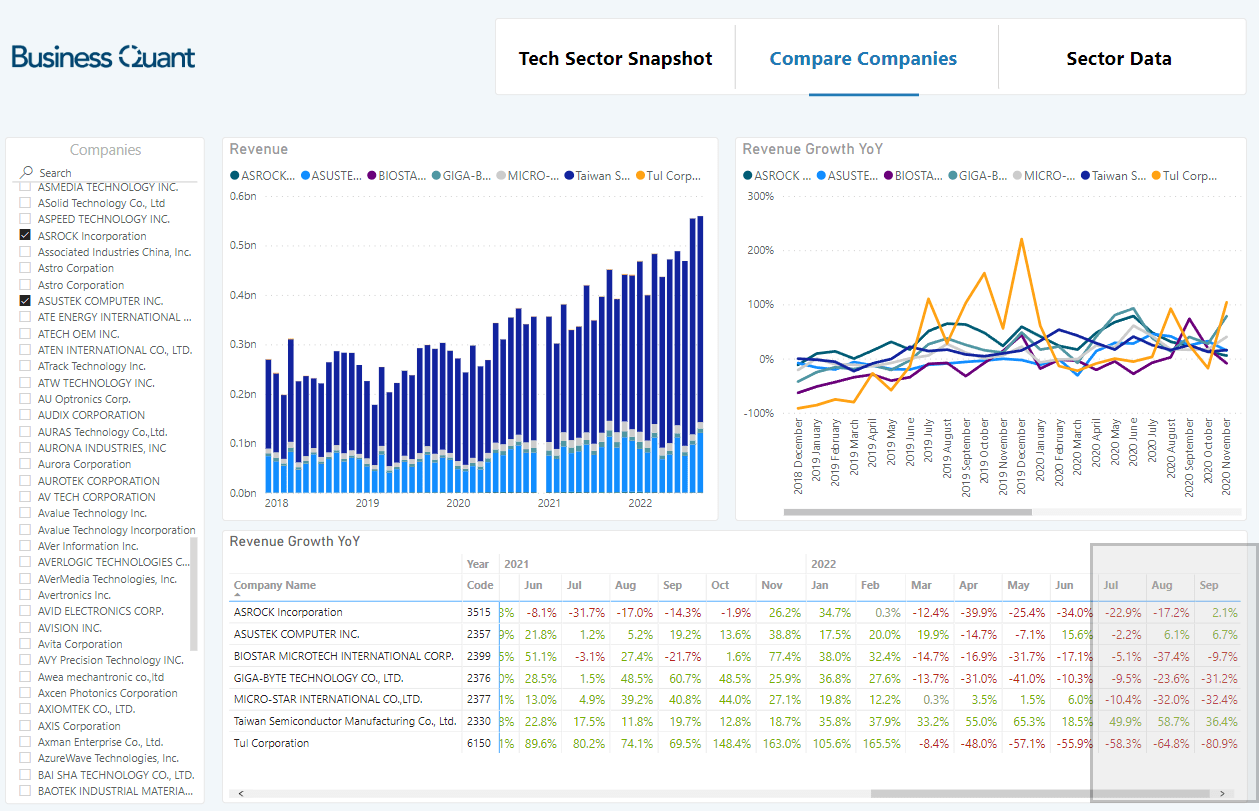

I’d like to start by saying that Nvidia is practically a chip designer today. Its engineers design chip circuitry, which are sent to Taiwan Semiconductors or Samsung for fabrication on actual silicon wafers. Then, these chips are packaged and assembled in the form of usable products and later distributed to end-markets by Nvidia’s board partners such as Gigabyte, ASRock and Micro Star International. Some of these companies also manufacture and distribute computing peripherals around Nvidia’s ecosystem of products. With so many channel partners involved, we can monitor their monthly sales data and get an idea of how Nvidia’s ongoing quarter is shaping out to be.

We, at Business Quant, have developed a tool to serve exactly this purpose. It tracks and monitors monthly sales data for over 1200 Taiwanese suppliers, so we can get insights about the state of supply chains across different industries. Note in the chart below that sales of Gigabyte, Micro Star International, Biostar Microtech and Tul Corporation shrank significantly from July through September. These firms manufacture Nvidia-branded GPUs, motherboards and/or other computing peripherals. Also note that for a few companies, the sales decline accelerated in September. This suggests that financials for Nvidia’s channel partners are deteriorating quickly.

BusinessQuant.com

If Nvidia’s SKUs were selling like hotcakes and preserving their average selling prices (or ASPs), then its channel partners would have seen their sales grow or at least plateau for the time being. But sales decline to the tune of 30% to 80% across channel partners suggests that Nvidia is struggling to sell its SKUs for the time being at least. This signals weak consumer demand muted consumer spending power, despite plummeting GPU prices.

It’s evident from the table above that Taiwan Semiconductor (TSM), which is a fabrication partner for the chipmaker, registered elevated sales growth during September on a year-on-year basis. This is counterintuitive – if chip designers and their channel partners are struggling to make sales, then how can a chip fabrication company thrive at the same time?

There’s one probable explanation for this – chip designers such as Advanced Micro Devices (AMD), Nvidia, and Qualcomm (QCOM) are yet to cancel their orders with Taiwan Semiconductors. We’ve already heard rumors of AMD planning to cut production in light of slowing consumer demand but there hasn’t been an official confirmation on this. But this data suggests that chip designers like Nvidia and AMD will have to cut production in order to avoid inventory build-up.

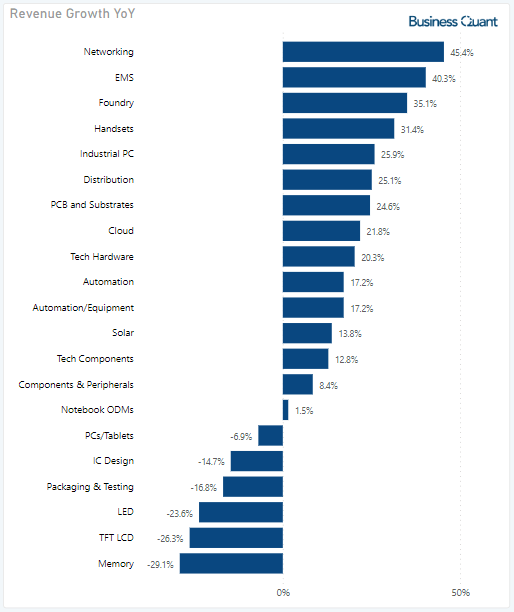

To have a better understanding of the situation, I pulled the industry-wise sales numbers for September. As it turns out, sales are down for computing and some of the other closely associated industries, but still up for others. So, it seems the slowdown is either limited or not yet proliferated to the broad swath of other industries.

BusinessQuant.com

But this begs the question – what does it all mean for Nvidia’s shareholders?

Impact for Investors

I’d like to clarify that most of the companies mentioned in the table above, have diversified product portfolios and have non-exclusive manufacturing arrangements with Nvidia. For instance, Gigabyte, MSI and ASRock, manufacture GPUs, motherboards and other computing peripherals for Nvidia as well as its competitors, that is, Intel (INTC) and AMD. So, we have to take note that these monthly sales figures are indicative of the state of personal computing industry sell throughs, rather than specifically being limited to Nvidia’s ecosystem of products.

But having said that, if Nvidia, AMD and Intel, in general, had a strong sales momentum, then these partner firms would have also reported strong sales figures. Their sales slump only shows that Nvidia and its peers are going through a sales downturn and investors need to brace for impact in the upcoming earnings season. AMD has already reported weak preliminary Q3 results, and I contend that Nvidia and Intel will follow suit in the coming days.

Although Nvidia has released its next-generation RTX 4090 GPU, I don’t think one SKU alone will make much of a difference on the company’s overall financials and its blended ASPs. It would have to release more SKUs in the coming months under its RTX 40-series banner, whilst carefully depleting its RTX 30-series channel inventory, to be able to tackle this sales slump. So, I believe that Nvidia is set for a quarter or two of sales slowdown at least.

There is one way where the company might be able to trump this sales slump quickly — bear in mind that this is pure speculation on my part. Last month, U.S. regulators imposed an export ban on Nvidia and AMD-branded datacenter GPUs to Chinese customers. The affected Chinese datacenter clients must be frantic and would be looking to stock up on these enterprise-grade GPUs before the ban comes into full effect. If Nvidia can prioritize production of its datacenter GPUs on a short notice (like it’s being rumored here) then it might very well be able to sell volume quantities to desperate customers at a premium, and stabilize its sales along the way.

(Read – Yes, AMD Is Now On Sale)

Investors Takeaway

The takeaway here is that Nvidia is likely going to post dismal sales numbers for the next quarter or two at the very least. Risk averse investors who don’t have the appetite for portfolio drawdowns and volatility, may want to exit the stock on rallies.

BusinessQuant.com

However, investors with a multi-year time horizon and have the appetite for portfolio drawdowns, may want to wait for potential price corrections before calling it a bottom. The stock is trading at a steep premium compare to many of the other rapidly growing semiconductor stocks, and there are going to be more attractive entry points especially now that we’re in a recessionary environment. Good Luck!

Be the first to comment