Justin Sullivan

Beyond The Hype has been ahead of the curve on Nvidia (NASDAQ:NVDA). Our recent articles on the subject, with the stock trading near record highs, portended a valuation compression for Company.

Seeking Alpha

The above theses were written at a time when the sell-side was pushing the stock hard and slapping stock price targets as high as $375. Of course, unbeknownst to the sell-side and many investors, the Company’s growth was being fueled in large part by crypto mining. When crypto imploded as forecasted by Beyond The Hype, it became clear that the sell-side prognostications were not worth the digital ink they were written with.

Unfortunately, there seems to be little in the form of learning from this recent experience. We are, once again, seeing irrational exuberance and bullish analyst and investor behavior since Nvidia preannounced its fiscal Q2 earnings. As a result, the stock does not move down much after that disastrous Q2 preannouncement. Even now, analysts are pushing the stock as a recovery candidate as it was when crypto imploded last time in 2018.

This article makes a case for why it is unwise to be chasing Nvidia stock at the current levels and why this stock could easily lose 50% of its value as the unsupportable assumptions behind the Company’s bull case unravel.

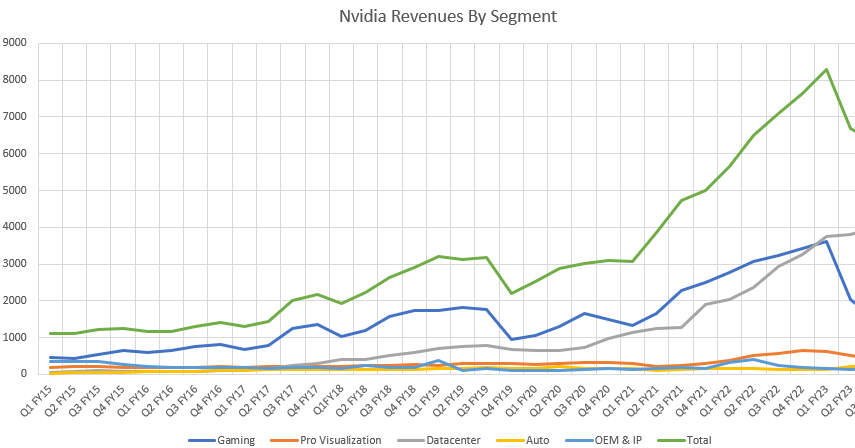

The Company’s current narrative is driven by expectations of hypergrowth. Investors and the sell-side analyst community have been thoroughly hoodwinked by the Company’s hypergrowth narrative. It is an easy trap to fall into given the Company’s revenues did grow rapidly over the last couple of years (see image below).

Nvidia Revenue Trends By Subsegment (Author – from Nvidia filings)

But appearances can be deceptive. The reality is that the growth of this so-called hypergrowth company is moderate outside of unsustainable short-term or one-time vectors. Let us start with breakdowns of revenues by segment charted in the image above.

Firstly, note from the image above that growth outside of “Gaming” and “Datacenter” is pretty much nonexistent. While management continues to talk in superlatives, especially when it comes to the “Automotive” segment, the narrative has been and continues to be disconnected from reality and there is no evidence that autonomous vehicles are imminent. The “Pro Viz” segment gives an appearance of strong recent growth, but anecdotal evidence suggests that this is being driven, at least in part, by crypto mining. It would not be surprising if $200M to $300M of this $600M quarterly run rate in this segment is from crypto. Note that Nvidia’s preannouncement indicates a $200M shortfall in this segment. This is consistent with the $200M to $300M estimate. In other words, there may not be much, if any growth in this segment outside of crypto mining.

Secondly, note that the “Gaming” revenues fell by about $1.6B between Q1 and Q2. As any reasonably diligent investor knows, this was mainly driven by the cryptocurrency bubble bursting. This bubble, unlike in the past cycles, is not coming back due to the well-known “Ethereum Merge“. Ethereum Merge is increasingly appearing to be a September event. In other words, Ethereum will go to Proof-of-Stake, and crypto mining demand would plummet in about a month from now. What is a reasonable level of “Gaming” revenues post Ethereum PoS? $1.5B a quarter? $2B a quarter? To estimate this, we need to consider how crypto mining affected Nvidia revenues over the past few years. This will be covered later in this article.

Thirdly, the Datacenter business has also been driven in part by COIVD, crypto, and free FED-driven opulence with many worthless startups spending like drunken sailors, especially on esoteric AI projects. These temporary growth vectors will now abate. This will act as a headwind to Datacenter growth and near-term growth is likely to be more moderate than investors have witnessed in the last couple of years.

Finally, it should not be missed that a good part of the Datacenter growth has come from the Mellanox acquisition. While Nvidia does not break out revenues from the Mellanox side of the Company, it appears that about a third of Datacenter revenues come from Mellanox. Note that this purchased growth is not likely to recur unless Nvidia makes another big acquisition.

The point of the above discussion is that much of Nvidia’s recent growth is driven by unsustainable “onetime” events such as COVID and crypto and that a valuation based on this growth is unrealistic.

How do we get to estimate the new-post-reset level of business at Nvidia? What is a sustainable long-term growth rate for the Company? The sections below will address these aspects.

Crypto Headwinds Are Deeper Than The Market Realizes

A good starting point for estimating sustainable Gaming GPU demand is understanding the PC industry dynamics. While desktop PC AIB business has been declining for the past decade, gaming laptops have been offsetting the AIB decline. It is unclear if there is meaningful growth in the combined desktop plus laptop GPU market, but there is not much evidence to support strong overall growth. Much of Nvidia’s “Gaming” growth has been occurring due to ever-increasing GPU prices.

As a point of reference, the top 3 Turing SKUs RTX2080Ti/2080/2070 launched at $999/$699/$499, respectively. The top 3 Ampere SKUs RTX3090Ti/3090/3080Ti launched at $1999/$1499/$1199, respectively. We do not believe there was ever a meaningful demand for gaming at $1000+ price points and the ASP uptick was fueled almost entirely by crypto.

PC units, after a big jump during COVID times, are now headed back to pre-CVOID levels. If we back up the clock to pre-COVID times, we can see from the image above that the “Gaming” peak was below $2B and revenues have been in the range of $1B to $2B since Q3 FY2017. If one were to be generous to the management, $2.0B is not a bad quarterly Gaming revenue estimate in the coming quarters.

In the short term, Nvidia will also have other problems with GPU inventory – both new and used. Ethereum PoS merge, possible in Q3, is not going to help matters much. The merge will not just cut the demand for new GPUs but make useless a ton of GPUs already being used in mining. This could bring a flood of used GPUs into the used GPU market.

This inventory, especially the new card inventory, also impacts new product releases. The Lovelace generation GPU releases will have to be slowed down as the Company flushes out the Ampere generation inventory from the channel. Nvidia and its partners would have to heavily discount the current premium parts 3080/3090 series. Even with price cuts, time is of the essence. Rival Advanced Micro Devices (AMD) is set to introduce its next-generation RDNA3 solutions in Q4 and it does not appear that AMD has much of an inventory problem.

Recalibrating Nvidia’s Past Sustainable Growth

The above vectors mean that the sustainable current business level for Nvidia is likely about $6.0B to $6.5B. If we generously ballpark Q3 FY23 revenues to be $6.5B, this suggests a revenue CAGR of about 20%. This is respectable growth but hardly the hypergrowth reflected in the Company’s valuation.

Note that this 20% growth rate includes the Mellanox acquisition. The growth rate would be in the teens.

Looking Ahead: Investors Expecting A Rapid 4-Quarter Recovery Will Be Disappointed

Note from the image above that, when the last crypto bubble burst in 2018, it took the Company about 4 quarters to recover from the malaise and revenues accelerated subsequently in 2020. Investors looking at the 2018 burst as a guide are going to be misled on how long it will take Nvidia to recover from the current crypto bubble bursting because the environment today is much different. In addition to the factors discussed earlier, here are some important ways in which the current recovery cycle will be different from the 2018 cycle.

- The current crypto wave is a far bigger wave than the previous waves.

- Preliminary indications are that AMD will improve its competitive position against Nvidia with RDNA3.

- Unlike in the 2018 cycle, Intel (INTC) is now competing at the low end of the GPU market and will almost certainly take share from Nvidia – especially in lower-end laptops.

- Nintendo Switch shipments were in ascendency post-2018. After the COVID peak, Nintendo Switch console shipments have continued to drop

- Datacenter business does not look that great either. For H2, Beyond The Hype is watching carefully the spending of technology companies as the public and private market valuations of these companies compress.

H2 Prognosis And Relative Valuation

The factors discussed above suggest that between Gaming and ProViz businesses, Nvidia is likely to see another $500M drop in Q3 revenues compared to the recently announced Q2 outlook. Datacenter growth will not be able to offset it in a meaningful way. In other words, Q3 revenues are likely to be in the $6.0 to $6.5B billion range. Given crypto business commands high margins, the gross margin hit will be significant.

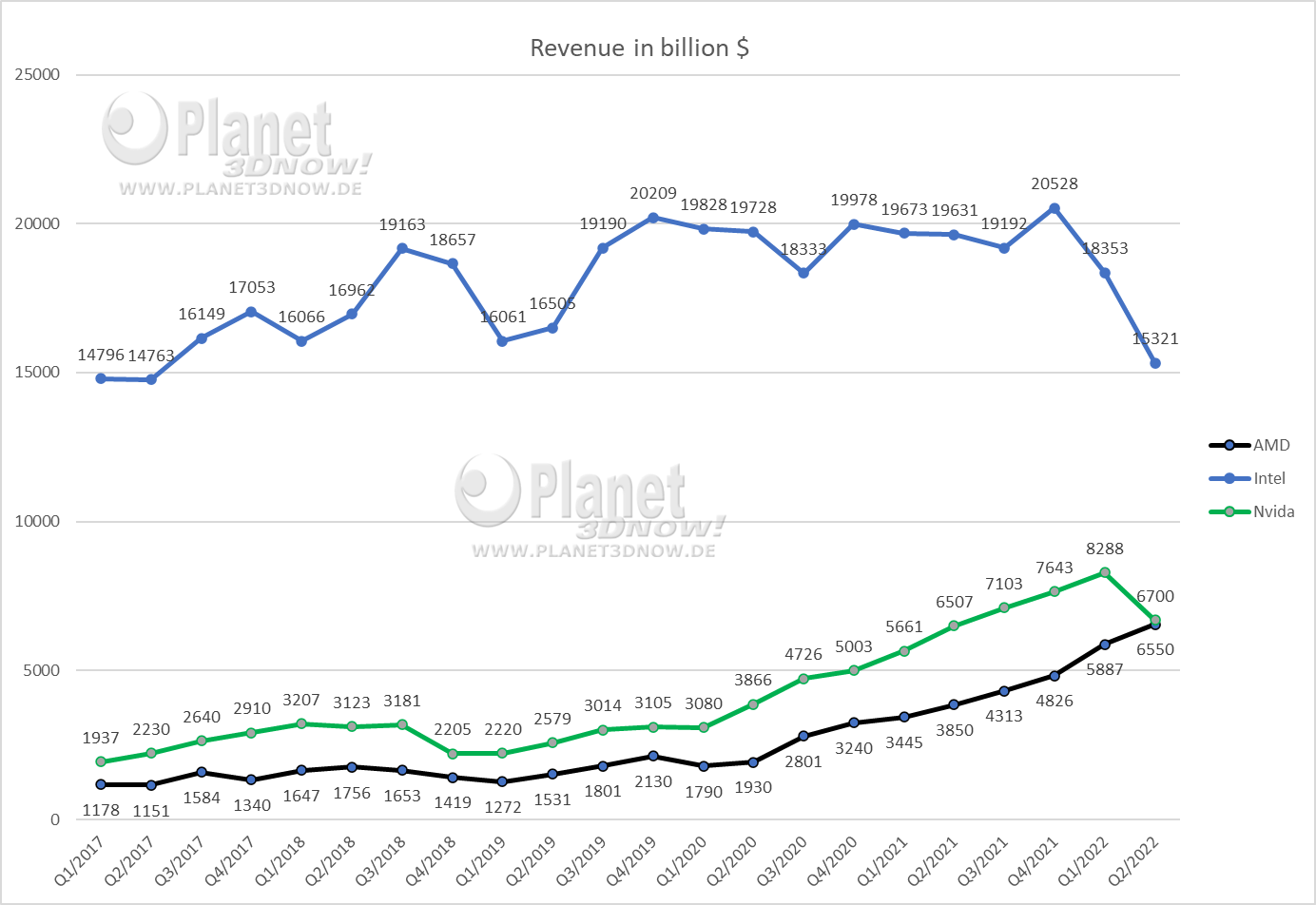

In addition to lower growth, lower revenues, lower margins, and lower EPS, Nvidia is also likely to start suffering from a relative valuation problem. Note from the image below that, AMD has now caught up to Nvidia in revenues and is growing at a faster rate. As such, AMD is likely to deliver higher revenues and profitability than Nvidia in Q3. Given this reality, the much higher multiple being ascribed for Nvidia will increasingly look ridiculous.

Revenue Trends – AMD, INTC, NVDA (Planet3DNow)

https://twitter.com/planet3dnow/status/1556708886760943616/photo/1

With profitability shot due to various factors, the stock may start trading on a revenue multiple instead of a PE multiple and it could get ugly.

The market also does not seem to have figured out that the very high-margin crypto business is not coming back. Contrary to management guidance, Nvidia’s long-term gross margins and profitability will be negatively impacted by this development.

Many other headwinds mean that revenue recovery will be long and profit recovery even longer. With decreasing profitability and lower growth rates, Nvidia’s valuation is overdue for a reset. With EPS shrinking, should Nvidia’s valuation start approaching that of peer AMD on a revenue multiple, the stock could fall at least 50%, if not more.

Be the first to comment