hh5800

The chip industry has seen a lot of changes in recent years. With Advanced Micro Devices’ (AMD) impressive resurgence, Intel (INTC) is losing market share. Additionally, Apple (AAPL) shocked everyone by debuting its M series chips, which crushes the competition. As a result, many engineers became inspired, leaving the big hardware companies (Apple, AMD, Intel) to start their own chip startups. As well, tech software giants with deep pockets decided to make their own custom computer chips: Meta Platforms (META), Alphabet (GOOG, GOOGL), and Microsoft (MSFT).

There have been a lot of shakeups, and the demand in the computer-making business has never been hotter, as the Intel monopoly looks like it may be coming to end.

In 2021, one very promising chip startup, NUVIA (founded by ex-Apple employees), was purchased for $1.4 million by Qualcomm. I believe that out of all the competition and companies out there, NUVIA is probably the most likely to succeed. However, that doesn’t mean it is guaranteed. In this article, I will lay out the likelihood of QUALCOMM Incorporated’s (NASDAQ:QCOM) segment NUVIA being able to pull off what they have been promising. If so, expect it to be a very big deal for Qualcomm and a game changer in the computer chip market.

What Is NUVIA

NUVIA was founded by high-level ex-Apple employees, with the aim of providing the best performing chips in terms of performance per watt using ARM-based Instruction Set Architecture (ISA). They aim to create the fastest chips on the market covering: the server market, personal computers, as well as the mobile space. Previous research on Seeking Alpha has a detailed breakdown of their performance plans and vague plans on how they attempt to achieve them.

Recently, Qualcomm’s CEO claimed NUVIA chips will beat Apple’s M2 performance. That is quite a statement from the CEO, and just shows the confidence that Qualcomm has in its newly acquired unit. However, the possibility of that actually occurring is something we will discuss further down in this article.

The Competition

There are many start-ups popping up with huge talent leaving the big companies as previously mentioned. Private companies are not really covered on Seeking Alpha, so we will leave those out. But none of them look like a real threat so far, as they are far too early in development. The majority of the industry just assumes these startups are not much of a threat and don’t have much of an end game other than just trying to be purchased by bigger companies.

Producing computer chips are extremely hard, and it’s why very few companies have been ever been able to commercially successfully sell on a personal computing and server market scale: AMD, IBM (IBM), Intel, and now Apple.

This is what makes NUVIA’s story interesting. They achieved the goal of being bought up, and surprisingly are not following the route of the vaporware realm, much like the majority of chip-startups purchased in the past, like this Intel purchase.

On the non-startup side, the server and custom chip market is having tons of activities as big tech giants are trying to produce their own chips. Following the movement of employee migrations from company to company on LinkedIn shows veterans of the industry moving to companies like Alphabet, Meta, and Microsoft (MSFT) (traditional software companies). These veterans are being lured with huge pay and enjoying the perks that only software developers exclusively enjoy.

As I mentioned with startups, it’s also unlikely that the tech giants, with almost 0 hardware experience will also be able to create successful hardware divisions. Their real motive is likely to threaten AMD and Intel to bring the cost of their hardware down.

Apple is one of the biggest threats to everyone because they actually pulled it off, and it took over a decade with very deep pockets. After all, they have always been a hardware company, they just didn’t make their own chips. In terms of competition, Apple’s M series chip only goes in one place, Apple products. Their competitive edge in power and performance heavily relies on the Apple ecosystem. If you want their chips, you will have to own Apple. So in other words, there is plenty of room in the market for new competition.

Why NUVIA May Fail

The point of this article is to help investors determine the probability of NUVIA succeeding, thus adding a new dimension to Qualcomm’s business strategy. At this point, no one outside the company has any idea whether NUVIA will be to succeed in providing a working product, as well as one that is competitive in terms of performance and power. The best we can do is make an educated guess.

In this section, I will talk about the difficulties that NUVIA/Qualcomm will face, as well as past roadblocks that have led to failure in the past. This should give the reader a good understanding of how difficult it is to enter and succeed in the hardware chip business.

- Qualcomm has been here before, having its own data unit center, based on ARM products, they sadly failed in 2018 laying off the entire division. Goes to show you even hardware companies have difficulties expanding from the mobile market.

- Optimized software is a necessity to take advantage of the hardware. Qualcomm CEO’s claim of NUVIA potentially beating M2 chips is somewhat of an absurd statement. Even if the hardware is there, there needs to be massive software support to be able to fully take advantage of the hardware architecture. This is why X86 has such a huge edge, despite its archaic Instruction Set Architecture: software optimization. In other words, to see the hypothetical edge of NUVIA chips, Microsoft would have to be fully on board producing a highly optimized Windows operating system. Optimization requires employee commitment, which always costs money. So Microsoft would have to invest and believe in NUVIA chips.

- NUVIA is already experiencing delays, their chip has already been pushed back to 2023. Also, it’s possible by the time NUVIA is faster than the M2 chip, it’s likely Apple releasing its M5 chips.

- Apple is suing NUVIA, the matter is playing out in the courts, and now it’s Qualcomm’s problem.

- NUVIA has claimed they will be the best in the market, however, aside from a few PowerPoint slides on performance and power, there is no clear understanding of how they will pull it off. They haven’t shown any ideas/innovations that give many people in the industry that they will be able to succeed. They have been really just living off the reputation of their founders.

Why NUVIA Might Pull It Off

As we have gotten the negatives out of the way, let’s review some reasons why this time it might be different and NUVIA will be able to pull it off and not only have a working product but the best in the business.

- NUVIA was able to convince a tech giant to purchase it. As I discussed in this article, there isn’t a lot of public information about NUVIA, but they seem to have impressed Qualcomm enough to purchase them.

- NUVIA is paying top dollar for talent. According to anonymous posts on Blind (a website dedicated to employees to discuss salary offers), NUVIA is giving massive salaries to new employees. Matching or even paying better than Nvidia (NVDA), Apple, Google, and others. This is a big deal, talent is everything when you want to make the best chips, and Qualcomm believes in this division enough to essentially give a blank check for hiring.

- According to Gerard William, NUVIA chips are being built from the ground up, completely reimagined pipeline architecture, much like how M1 changed the industry. It’s not hard to believe that the same pedigree from Apple, can do it again. As the industry had been stagnant for decades since it essentially has been a monopoly. So yes, this does seem like a plausible claim. They are doing it from the ground up, from scratch with fresh code, not constrained by legacy restrictions that hamper the current chip industry.

- ARM and Nvidia Merger fell through. As mentioned, NUVIA is using the ARM ISA, a potential merger could have created unforeseen issues, but luckily that fell through, a relief to the entire chip-making industry.

Technical Analysis

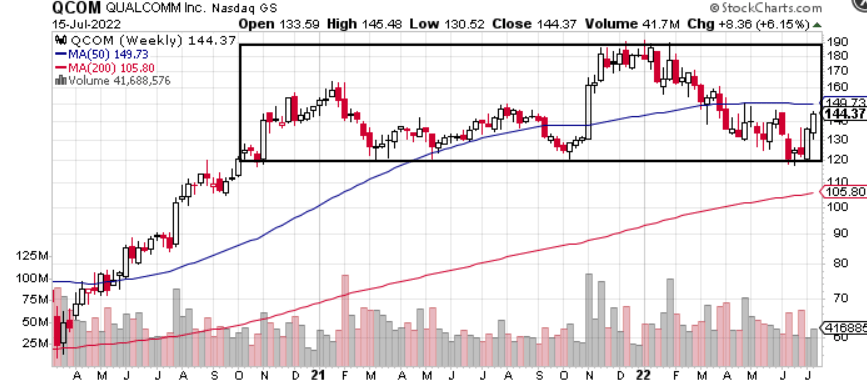

There is nothing particularly interesting about Qualcomm’s stock chart, keeping in mind the current terrible state of the market. I suppose that is good news, as the stock looks to be trading sideways for the last two years, pulling back just 23% so far this year (doing better than a lot of competitors).

Overall, it looks like the stock is trading sideways in a holding pattern. It’s personally not a stock I would purchase based on the chart, and at the same time, I don’t particularly see any red flags.

QCOM Weekly Stock Chart (stockcharts.com)

Conclusion

Qualcomm has made quite the statement purchasing an ambitious start-up like NUVIA. Their intent is clear, to be on top of the chip market, where power and performance are everything. If NUVIA/Qualcomm can pull it off, this will be a gamechanger for their business.

However, as I mentioned, there is a long way to go, even though there are promising signs. I personally, would not make any purchasing decisions solely based on the potential of NUVIA now, as more information needs to come out publicly.

However, is Qualcomm stock now a buy? The Fed has been creating a great buying opportunity as we speak. So, the answer is maybe, depends on your risk appetite, strategy goals, and investing capital. It’s clear that NUVIA was a purchase to help maintain Qualcomm’s relevance, as the battle with Apple rages on. If it ends up working, Qualcomm investors will be rewarded handsomely, but there is a long way to go.

Be the first to comment