Sundry Photography

The rebound in mid-cap growth stocks has begun, and in my view, the best way to play it is to focus on “growth at a reasonable price” stocks. Many high-quality technology companies, particularly in the software sector, fell to multi-year lows last year despite strong fundamental results (including and especially a renewed focus on profitability, driven in part by layoffs), and it’s a great time to capitalize on low valuations to build long-term positions.

Nutanix (NASDAQ:NTNX) is one company worth watching. This infrastructure software provider, best known for its “hyper converged” infrastructure that eliminates data center siloes to help backend operations run more smoothly, was recently the subject of potential acquisition talks by Hewlett Packard Enterprise (HPE). When these talks came to a halt, shares of Nutanix took a large breather. Yet, I continue to think there is plenty of opportunity for Nutanix to shoot higher, even in the absence of a near-term acquisition.

The bull case for Nutanix: even standalone, this company shines

Yes, there are macro headwinds at play. Like other IT technology companies, Nutanix is facing a situation where company leaders are delaying capex and digital transformation products. That doesn’t mean, however, that Nutanix isn’t priming itself for a return to growth. The company has continued to build up its ARR, and its focus on the bottom line has delivered tremendous results in bringing Nutanix above breakeven on a pro forma operating margin business. Once thought of as a hardware vendor with occasional software add-ons, Nutanix is now a pure software vendor with gross margins above 80% that is capable of running on any commodity data center hardware.

I am retaining a bullish opinion on Nutanix (the reason I am not very bullish as in the past is because Nutanix has seen a relatively more modest decline in 2022 relative to other software stocks, and comparatively speaking a lot of other very attractive bargain-basement plays have opened up in the sector).

Here is my full bullish thesis on Nutanix:

-

Enabling the hybrid cloud: Not all workloads can be moved to the cloud. These days, IT and computing are all about the cloud. But while the market is chasing after all the hot cloud stocks, the reality is that most companies – especially those in complex or highly regulated industries, or those that simply want more direct control over their data – will never entirely move their systems into the cloud. Nutanix is a champion of the “hybrid cloud” strategy, in which some of a business’s assets are in the cloud and others are in on-prem environments. For the on-prem assets, Nutanix’s hyper-converged technology ensures that customers get the same performance and agility benefits that users receive in the cloud. Most companies today employ some sort of hybrid cloud strategy – meaning Nutanix products are widely applicable to all IT departments.

-

Thought leader in hyper-converged infrastructure. VMware has been chasing Nutanix’s tail ever since the company gained prominence. For multiple years in a row, the company has been recognized as the category leader by Gartner, the software industry’s leading analyst and reviewer.

-

Software-first. Earlier on in Nutanix’s lifespan, the company sold server devices as its primary business, with its proprietary software overlaid as a “package solution.” Now, Nutanix sells only software. This has dramatically raised its margin profile while also making it more palatable for companies who only want to consume software to run on their own hardware.

-

Executing its new sales strategy. At the beginning of Nutanix’s fiscal 2021, the company made the earth-shaking decision to incentivize its sales staff based on ACV and not TCV. In the past, Nutanix’s account executives sold longer-term contracts and incentivized customers with bigger discounts because they were paid based on the value of the total deal. What’s important for Nutanix and for investors, however, is how much Nutanix can rake in annually and for each customer’s lifetime. So Nutanix shifted its sales compensation in line with this priority and began paying its sales teams based on ACV – and this has yielded very strong results in growing both ACV and ARR.

-

Prioritizing profitability. Nutanix made the decision to lay off 4% of its workforce, which is helping the company push above breakeven pro forma operating margins and deliver positive FCF.

Valuation update

At current share prices near $28, Nutanix trades at a market cap of $6.44 billion. After we net off the $1.39 billion of cash and $1.32 billion of convertible debt on the company’s most recent balance sheet, Nutanix’s resulting enterprise value is $6.37 billion.

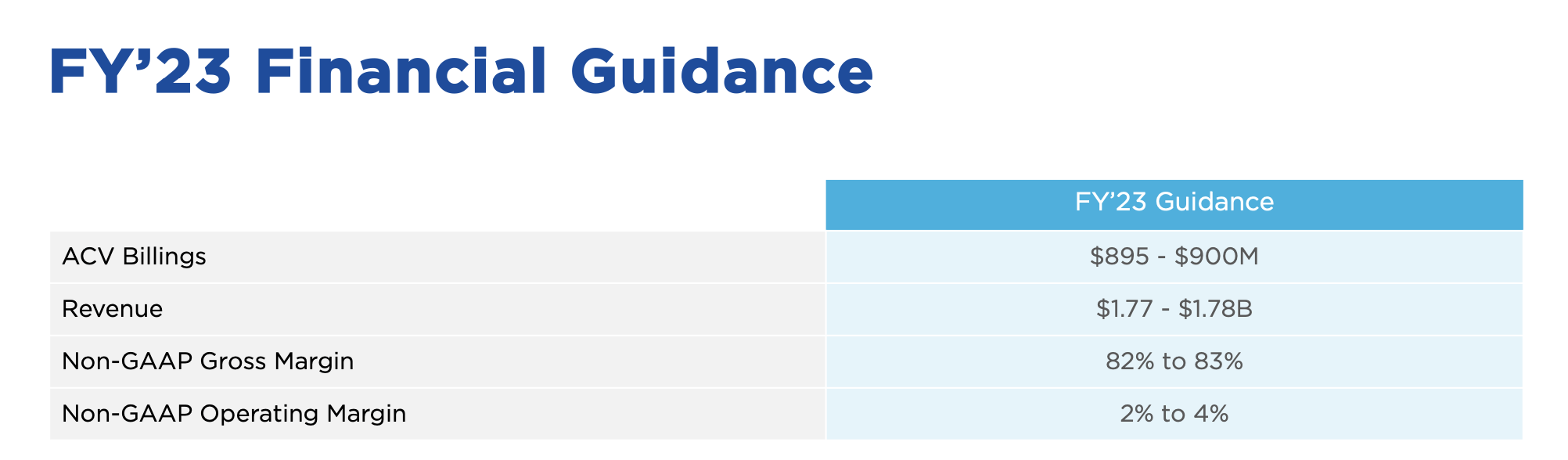

Meanwhile, for the current fiscal year FY23 (the year for Nutanix ending this July), the company has guided to $1.77-$1.78 billion in revenue (representing 13% y/y growth), on top of a 2-4% pro forma operating margin.

Nutanix outlook (Nutanix Q2 earnings deck)

This puts Nutanix’s valuation at just 3.6x EV/FY23 revenue. Note as well that Wall Street consensus is calling for Nutanix’s growth to accelerate in FY24, at a 16% y/y pace to $2.06 billion (putting Nutanix at a 3.1x EV/FY24 revenue multiple).

Needless to say, these are quite low multiples for a company with 80%+ margins, a largely recurring revenue base, expected acceleration to mid-teens growth, and above-breakeven margins with positive cash flow.

Strong recent trends underlie business health

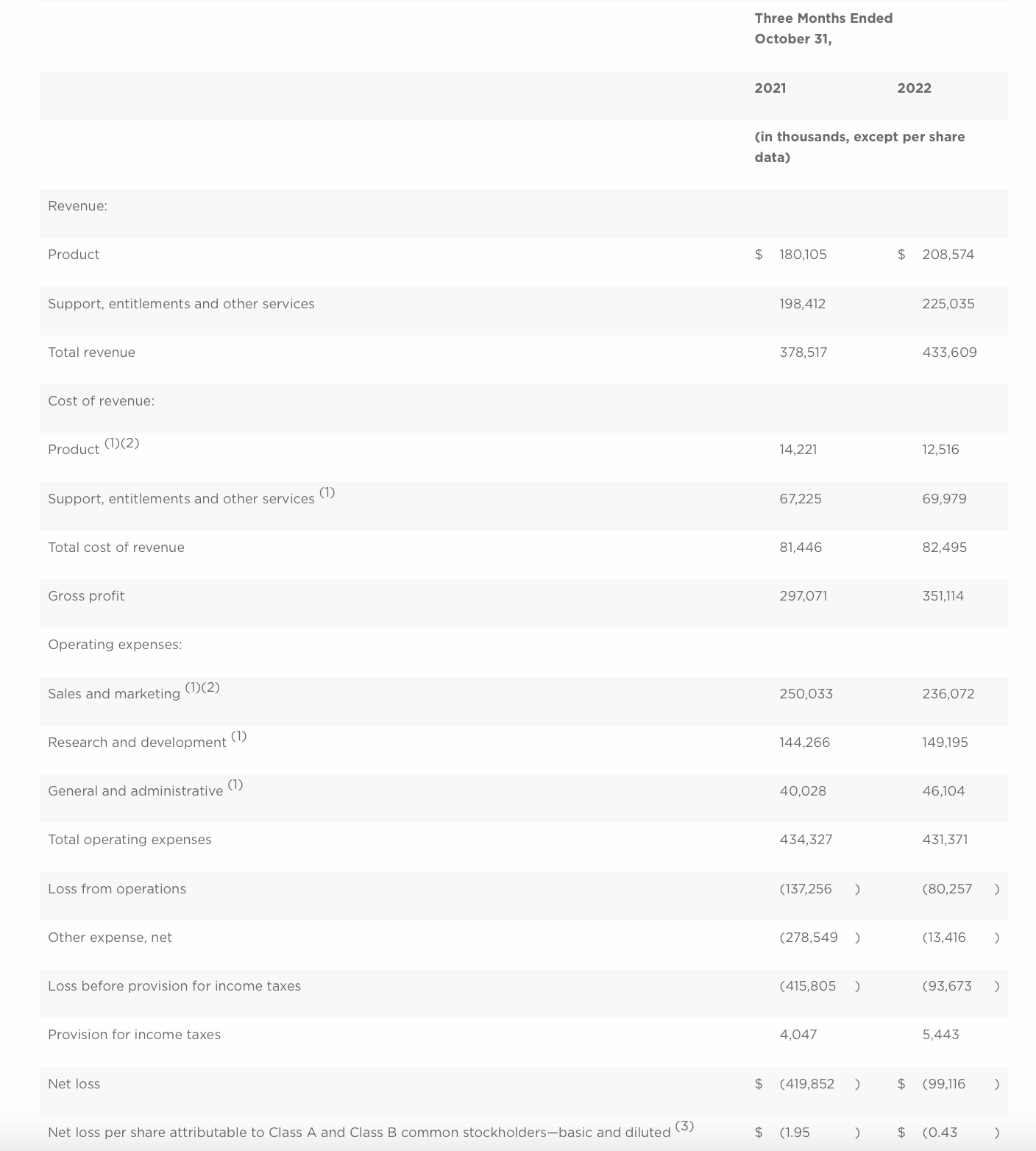

We don’t need an acquisition scenario for Nutanix to be a successful investment. The company has done incredibly well at growing its recurring revenue while also slimming down opex to improve profit margins in the past few quarters. Take a look at the fiscal Q1 (October quarter) results below:

Nutanix Q1 results (Nutanix Q1 earnings release)

Nutanix’s revenue grew 15% y/y to $433.6 million, beating Wall street’s expectations of $412.1 million (+9% y/y) by a huge six-point margin. This quarter also represents a huge comeback from Q4, which suffered a -1% y/y decline driven by supply constraints that caused availability shortages in the company’s server partners.

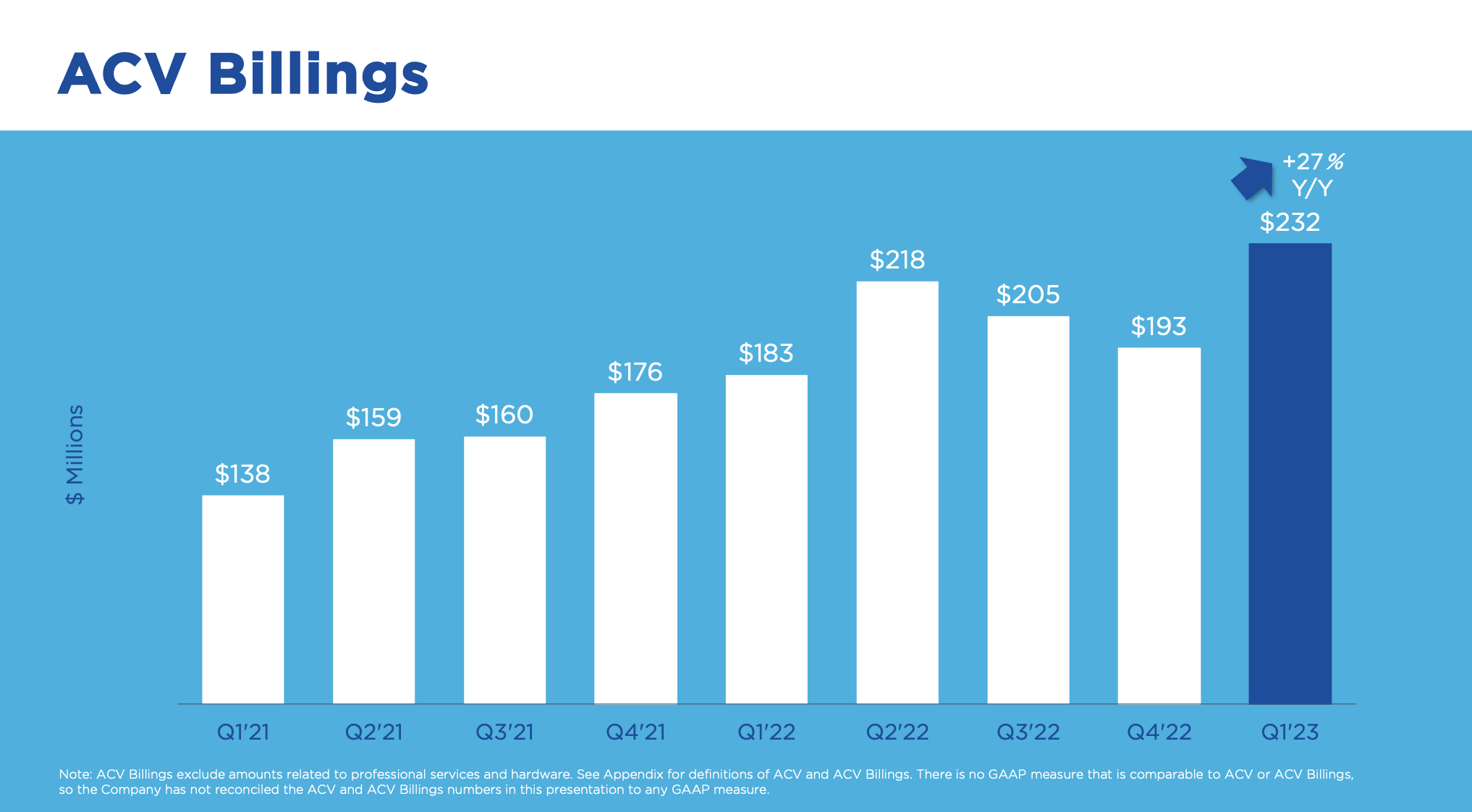

ACV billings also shot up 27% y/y to $232 million, a marked acceleration from 10% y/y growth in Q4.

Nutanix ACV billings (Nutanix Q1 earnings deck)

The company noted that despite continued customer interest in digital transformation initiatives, deals are seeing more management inspection and delays – which is similar to the commentary other software companies have made surrounding deal momentum in the last quarter of calendar 2022. Per CEO Rajiv Ramaswami’s remarks on the Q1 earnings call:

With respect to the macro backdrop, in our first quarter, we continue to see businesses prioritizing their digital transformation and data center modernization initiatives enabled by our platform. We have seen anecdotal evidence of increased inspection of deals by customers, which we believe is likely related to the more uncertain macro backdrop. We continue to factor this uncertainty into our outlook for the remainder of the fiscal year.

Taking a closer look at the first quarter, we delivered ACV billings and revenue above our guidance, driven by strong continued performance of our renewals business. We again demonstrated good expense management coming in slightly below our OpEx targets. Top line outperformance, combined with diligent expense management, enabled us to achieve positive non-GAAP operating income for the first time, another milestone in our drive towards sustainable, profitable growth. Finally, strong billings linearity and collections contributed to generation of $46 million of free cash flow, meaningfully exceeding our breakeven target and continuing our strong recent free cash flow performance.”

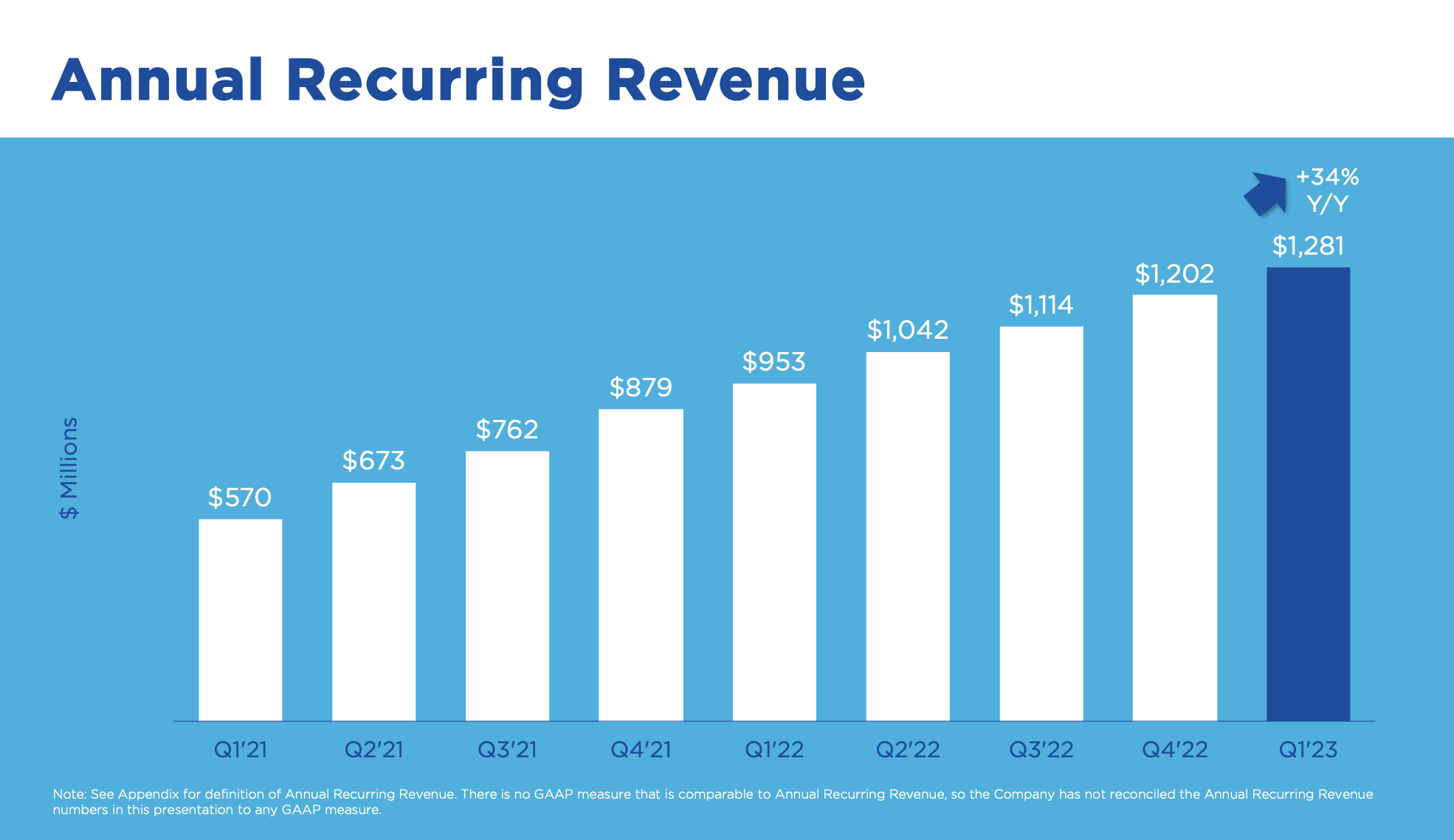

This did not impede Nutanix from continuing its rapid ARR buildup, however, as the company added $79 million of net-new ARR and grew 34% y/y to an ARR base of $1.28 billion.

Nutanix ARR (Nutanix Q1 earnings deck)

The company also noted that contribution from federal agencies was a big driver of Q1 performance, particularly in a federal civilian agency that signed on for a major expansion of its relationship with Nutanix to add workloads across storage, database automation, and cybersecurity.

Nutanix also boosted its pro forma gross margins by 130bps to 83.4%, from 82.1% in the year-ago quarter, while pro forma operating margins jumped more than thirteen points to 2.4%, from -11.1% in the year-ago quarter. Opex came in roughly $10 million below where the company had guided; partially driven by Nutanix’s layoffs, and looking ahead to Q2, the company expects pro forma operating margins to continue to expand sequentially to an expected range of 5-10%. First-quarter free cash flow also jumped to $45.8 million, representing an 11% FCF margin, versus a cash burn of -$1.9 million in the year-ago Q1.

Key takeaways

Low valuation, major boosts in profitability, a rapid buildup in ARR, and a solid software-driven product that boasts huge gross margins – there’s a lot to like about Nutanix heading into the remainder of 2023. Stay long here.

Be the first to comment