PhonlamaiPhoto/iStock via Getty Images

Want to benefit from higher interest rates? Check out this floating rate preferred vehicle from NuStar Energy LP (NYSE:NS):

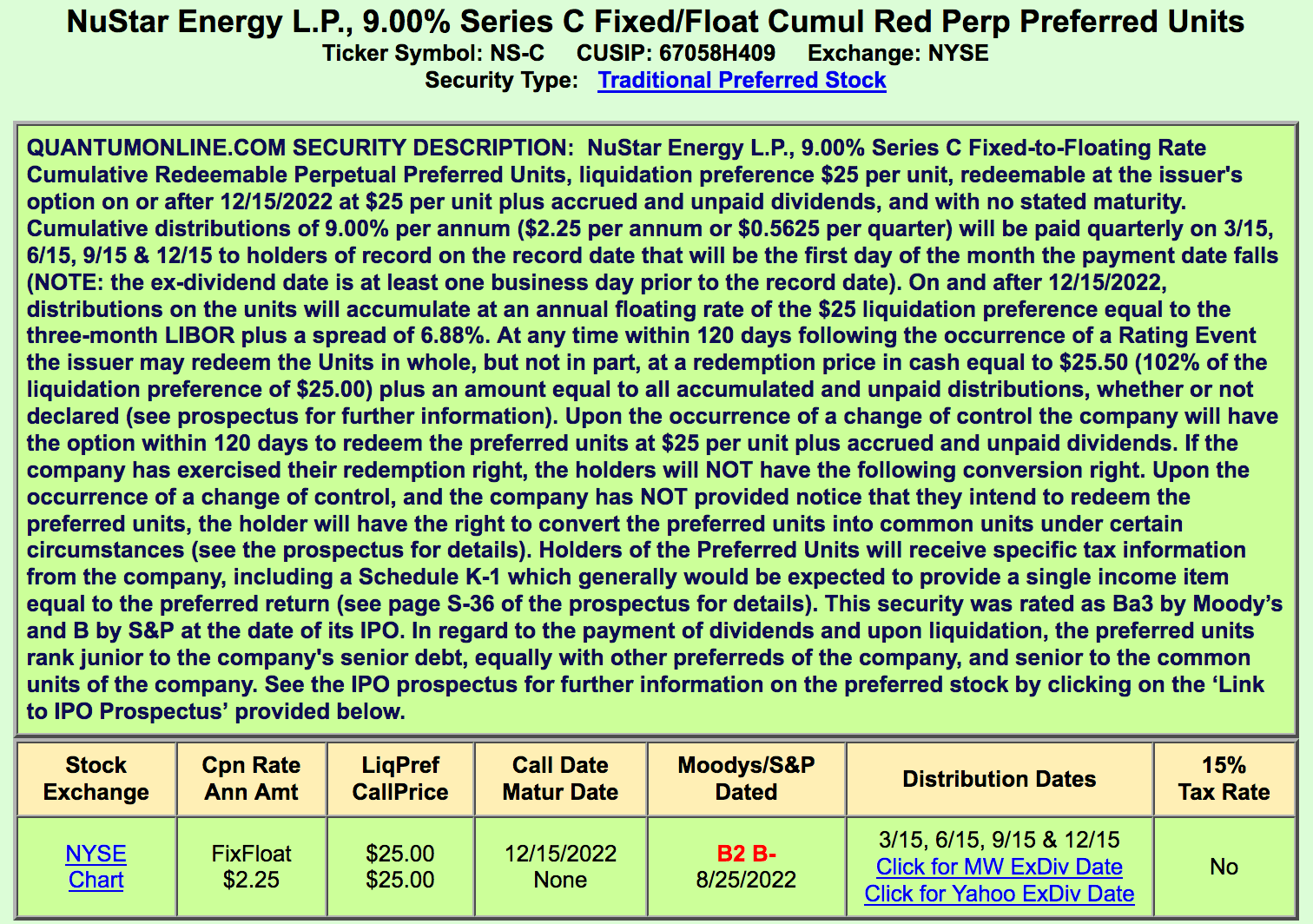

The NuStar Energy L.P., 9.00% Series C Fixed/Float Cumulative Redeemable Perpetual Preferred Units (NYSE:NS.PC).

These preferred units are cumulative, meaning that NS must pay unitholders for any skipped distributions before paying common distributions:

qntmnlne

NSS just entered its floating rate period on 12/15/22, which calls for a 6.88% rate plus the 3 month LIBOR rate, which is currently 4.75%, up dramatically from 0.21% one year ago.

Valuation and Yield:

At $22.13, NS-C is selling at an 11.5% discount to its $25.00 call value, which pumps up its equivalent forward yield even further to 13.14%, as of the 12/22/22 close.

Floating rate preferreds are tending to outperform fixed rate issues in 2023 due to the Fed’s interest rate hikes.

Hidden Dividend Stocks Plus

NS-C should go ex-dividend on ~2/8/23, with a ~2/14/23 pay date. We estimate that NS-C should pay ~$.7268/unit, with a forward yield of ~13.14%.

Hidden Dividend Stocks Plus

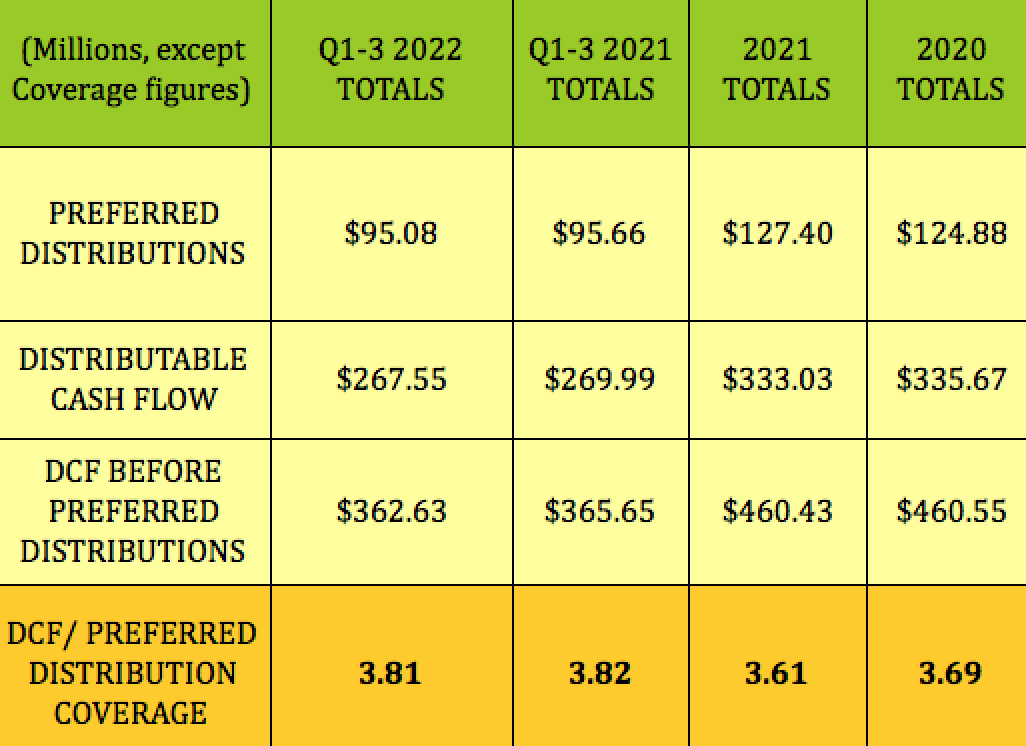

NS’s Distributable Cash Flow/Preferred Dividend coverage is solid, at 3.81X in Q1-3 ’22, vs. 3.82X in Q1-3 ’21, with a 3.69X trailing average:

Hidden Dividend Stocks Plus

Taxes:

NS’s preferred distributions are reported on a K-1 at tax time.

Company Profile:

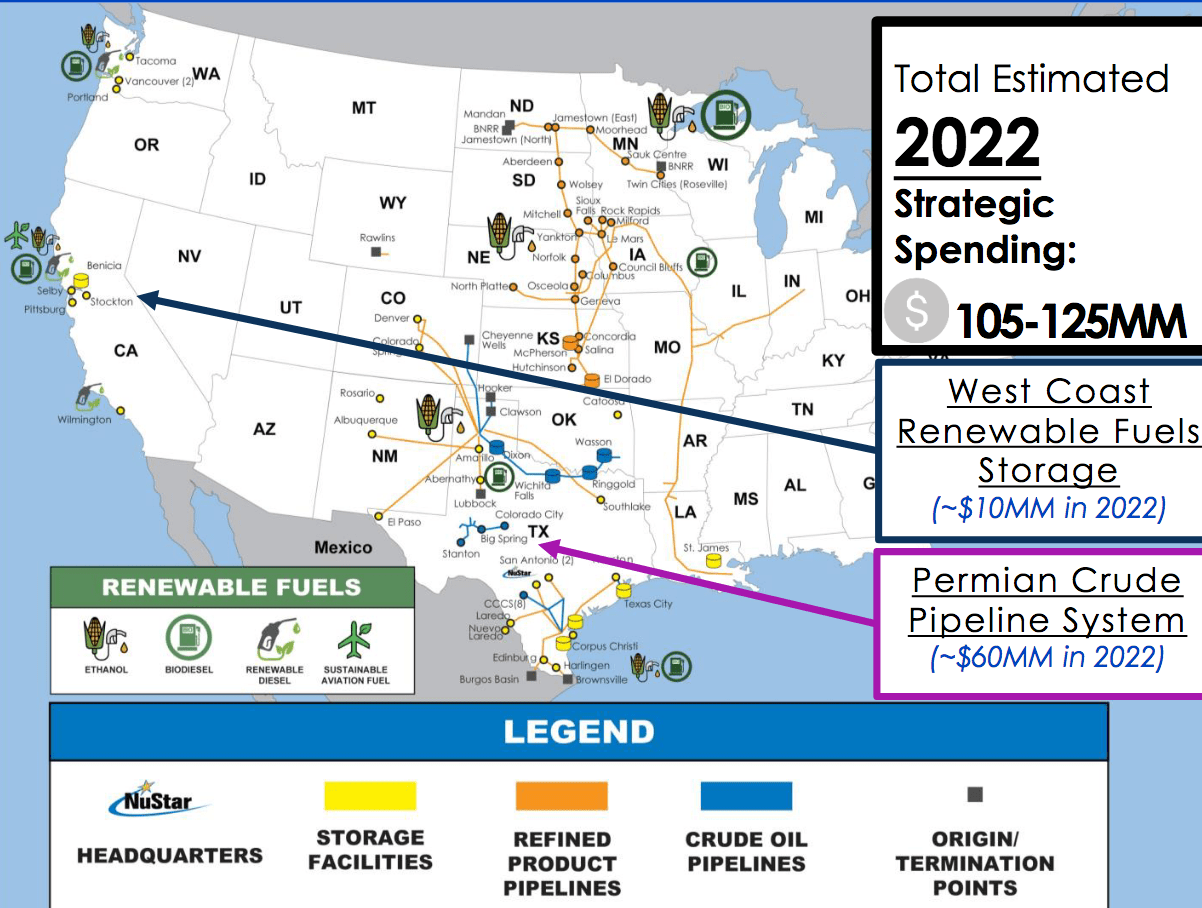

NuStar Energy LP currently has ~10,000 miles of pipeline and 63 terminal and storage facilities that store and distribute crude oil, refined products, renewable fuels, ammonia and specialty liquids. The partnership’s combined system has approximately 49M barrels of storage capacity at its facilities, and operations in the US and Mexico.

Since it went public in 2001, NuStar Energy L.P. has grown from 160 employees to about 1,200 today; from $387M in assets to $5B; and from $100M in revenues to $1.6B. (NS site)

NS is active in several US energy basins, including a concentration in the prolific Permian Basin, where management is spending ~$60M in 2022. It also has a presence in the renewables industry, with assets already in place in California.

NS site

Permian: NS’s Permian system continues to outgrow overall Permian Basin growth over the past several years. Oil production grew from 4.7 mmbpd in 2021, to 5.4 mmbpd in 2022, and is expected to grow to 6.3 mmbpd in 2023:

NS site

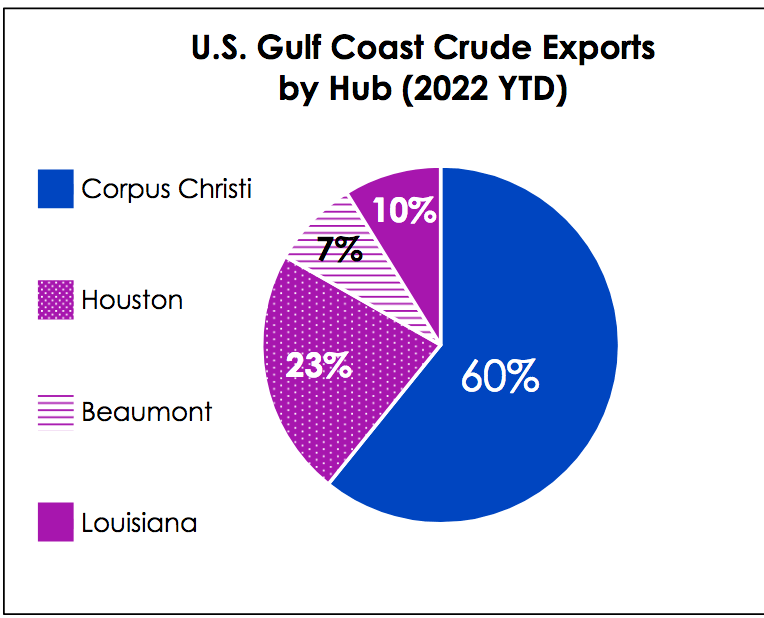

Exports: NS’s Corpus Christi facilities are well-placed for exports, with that hub accounting for 60% of Gulf Coast crude exports. NS’s North Beach Terminal, which receives barrels from its South Texas Crude Oil Pipeline System, its 12” Three Rivers Supply Pipeline and its 30” pipeline from Taft, as well as from third-party pipeline connections, It has an outbound capacity of 1.2M barrels/day.

NS site

Earnings:

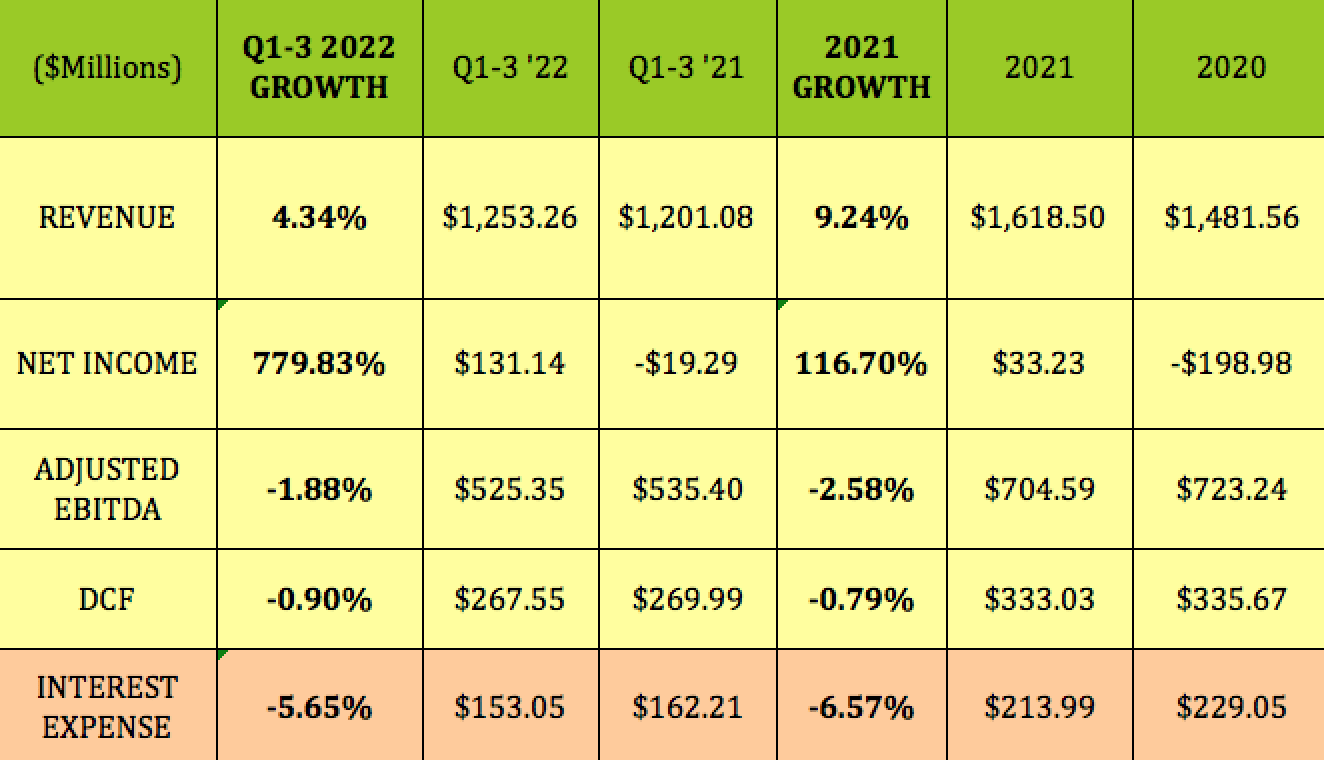

NS had a good Q3 ’22, with its Permian Crude System volumes hitting a record-breaking average of 580,000 Barrels/Day. Net income was $60M for Q3 2022, or $0.20/unit, vs. a net loss of $125M, or -$1.48 per unit, for Q3 2021, while adjusted EBITDA was steady, at $178M, vs. $177M in Q3 2021.

For Q1-3 ’22, revenue is up modestly, at 4.3%, whereas net income swung to a $131M gain, vs. a -$19M loss in Q1-3 ’21. Adjusted EBITDA growth is down a bit, at -1.88%, as is DCF, at -0.90%. Management has continued to whittle down Interest expense, which fell -6.57% in 2021, and -5.65% in Q1-3 ’22.

Hidden Dividend Stocks Plus

Profitability and Leverage:

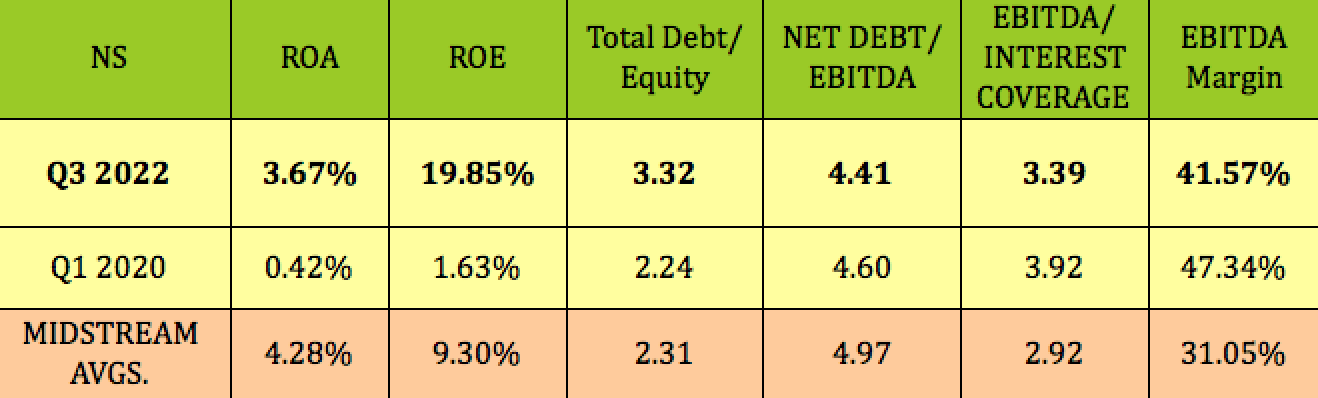

NS’s ROE has improved dramatically since Q1 2020, jumping from just 1.6% to 19.85%, far above the midstream industry average. ROA also improved, rising from 0.42% to 3.67%, as of 9/30/22.

Net debt/EBITDA improved a bit, to 4.41X, which is below the 4.97X midstream industry average, whereas EBITDA/Interest has fallen from 3.92X to 3.39X, but remains above average.

Hidden Dividend Stocks Plus

Performance:

Unlike some preferred stocks, the NS-C units have good average daily volume of 18,866 units. They’ve traded in a range of $20.98 to $25.50 over the past year, with a ~1% recent daily trading range.

Seeking Alpha

Debt & Liquidity:

As of 9/30/22, NS had liquidity of ~$1B, comprised of Credit facility availability of ~$993M and $7M in cash. Its next Senior Note maturity isn’t until 2025, when $600M comes due.

However, NS also has a privately held Preferred D obligation with a yield scheduled to rise to 13.75%, or $81.1M/year, which management plans to accelerate repayment on in 2022-2024. These are held by investment funds managed by EIG Management Company, LLC and FS/EIG Advisor, LLC, the advisor to FS Energy & Power Fund.

“We are now in discussions with the holders to repurchase as much as one-third of the Series D by the end of this year and we plan to redeem another third in 2023 and complete the redemption in 2024 several years ahead of schedule.” (Q3 ’22 earnings call)

Management already made good on part of its D series payoff goal – they repurchased 6.9M units, 30% of the outstanding D units, in November ’22.

That’s a good situation for holders of the NS-C units, since they probably won’t also try to redeem the NS-C units until the private NS-D preferreds are paid off over the next 1-2 years.

The number of Series D Preferred Units issued and outstanding as of Sept. 30, 2022, totaled 23,246,650, with a total redemption value of ~$581M.

NS site

Risks:

The $581M preferred D series payoff is key for NS. If they’re able to successfully complete this accelerated payoff, they’ll decrease the total amount of annual preferred distributions dramatically. That will subsequently further improve NS’s already solid preferred distribution coverage.

Parting Thoughts:

We rate NS-C a BUY, up to $25.00, as our top high yield pick for 2023, due to its discounted price, attractive 13% forward yield, and solid dividend coverage, which should further improve as NS repurchases the private D preferred series.

With the Fed still on a rate-rising path for at least Q1-2 2023, holders of the NS-C units should benefit from very attractive yields in 2023.

There’s also the potential for capital gains – NS-C is selling at an 11.5% discount to its $25.00 call value, but should catch a higher bid, once the market realizes it’s now in its floating rate phase.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

Be the first to comment