enigma_images/E+ via Getty Images

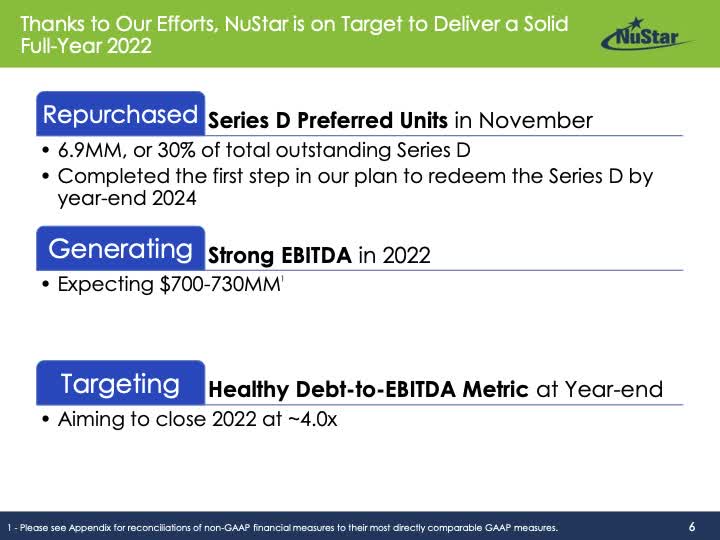

NuStar Energy L.P.’s (NYSE:NS) crippling coupling with high interest preferred stocks appears to be uncoupling. At the last financial conference, management announced its formal attack on that problem by repurchasing Preferred D shares, the company’s most offensive. A few weeks later, the company repurchased approximately 30% of those shares at $226 million.

Management’s intention initially indicated that this process would commence in 2023, ending in 2026. Good financial performance moved the beginning date to 2022, ending in 2024. This earlier approach for extinguishing this cash eating investment is a huge boon for investor. Understanding how well NuStar’s financial performance has improved is of utmost importance.

The Quarter & Year-to-Date

We begin with the September Quarter performance of the company:

- EBITDA increased by 6% year-over-year after discounting asset sells.

- Permian volumes increased by 15% year-over-year to 580,000 barrels per day. (Up 11% since the June quarter.)

- Management expects a 4th quarter exit from the Permian at or above 600,000 per day, a gain of 15% year-over-year.

- In refined products, volumes tracked pre-virus rates.

- Northern Mexico refined products volumes tracked 25% above last year.

- Corpus Christi Crude System averaged 340,000 barrels per day above the MVCs with October average 390,000 barrels per day.

- The pipeline segment generated $155 million in EBITDA up $10 million year over year.

- DCF equaled $93 million or 2.12 times.

- Total debt decreased to $3.1 billion (face value not fair value).

- NuStar essentially paid off its revolver, leaving $993 million.

- Leverage ratio was 3.93 at quarter’s end, just below its goal of 4. (Based on fair value)

- For the year of 2022, capital expenses are expected to range between $105 to $125 million.

The Business

With NuStar facing a significant change in interest rates within its Preferred D shares during 2023, the company’s business needs to be performing at elite levels in order to offload it. So next, we look at some internals.

- Refined product demands continues to perform at or above pre-virus levels. (Large refinery marketers are confirming this strength even outside of NuStar’s business.)

- Viewing possible negative effects on petroleum products, management reminded the analysts:

everybody is going to have some — see some effects, but I think that we’re relatively insulated from some of those things. And given that the United States is simply any way you look at it, it’s structurally short of the products that we need. We’re structurally short of crude globally, even in a recessionary environment and we’re particularly short here of refined products.

- Demand remains above the five-year range.

- Expects hefty FERC inflation adjustments next year.

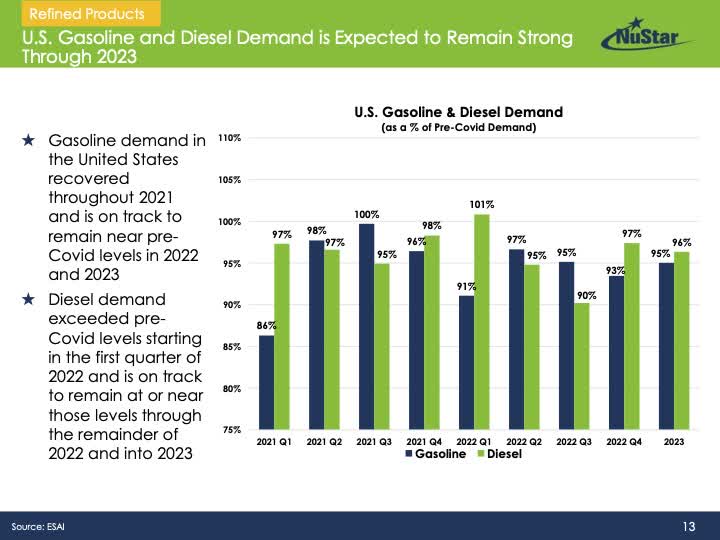

From the company’s latest presentation, a few slides are included. The first shows the gas and diesel percentages versus pre-virus levels.

NuStar Energy

Both are expected to remain near the pre-virus levels through 2023.

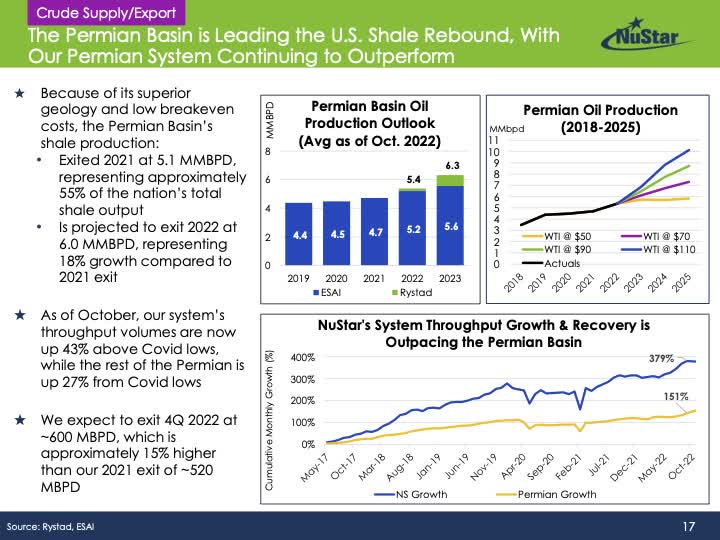

The next slide is a summary of the NuStar Permian assets.

NuStar Energy

Of importance, notice the above right portion of the slide showing strong continued growth from this basin through 2025. predictions almost double it from 2022.

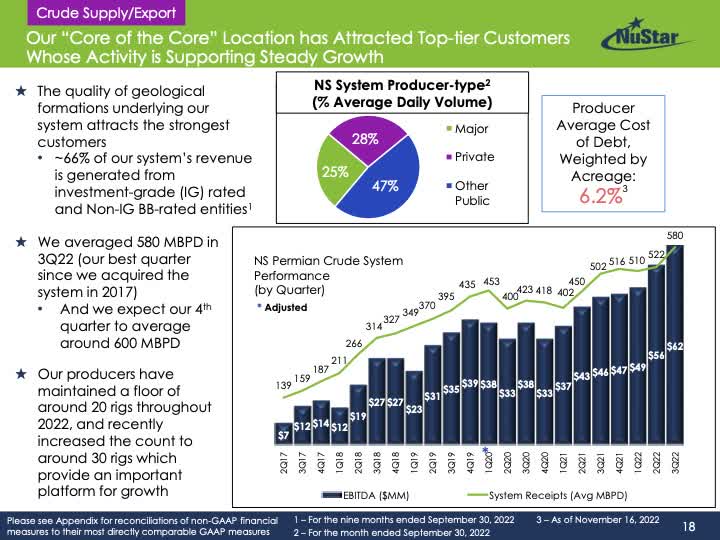

Next, a slide with actual EBITDA from the Permian is included.

NuStar Energy

Again, of significant importance is that in the last quarter, EBITDA grew to $62 million. It will even be higher in the December quarter with rates expected at 600,000 b/d up from 580,000 b/d. We discuss this further later in the article.

Looking Further at Cash Flows

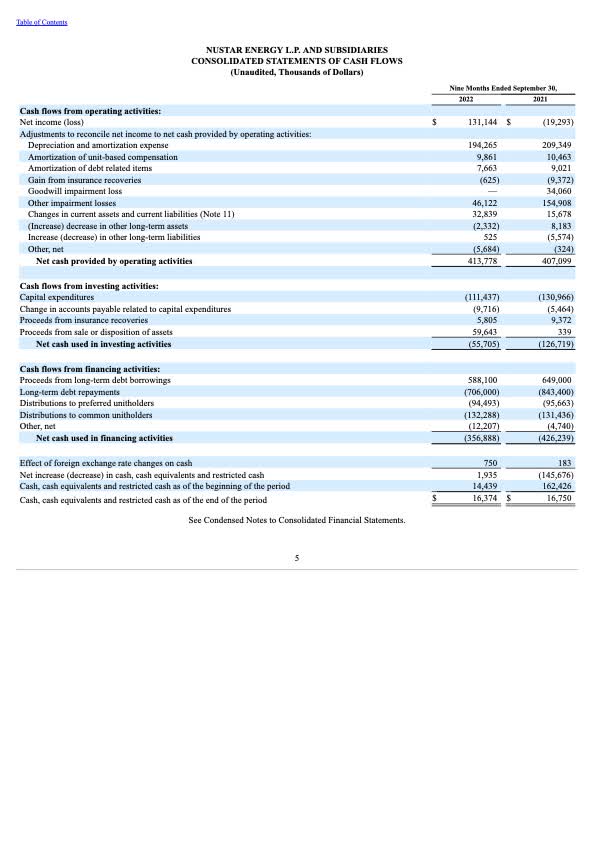

Next is a look at cash flows using numbers provided in the last 10-Q.

NuStar

The chart shells out a variety of valuable information. From that table, we assembled a simpler table for estimating extra cash generation for the next four quarters, December 2022 through September 2023. Included in the table was a charge of $226 million incurred in November for purchasing 30% of the Preferred D shares. More on this repurchase later.

| Cash Evaluation (Millions) | Three Qrds | Full Year * |

| Cash Generated | $415 | $550 |

| Distribution Plus | $230 | $310 |

| Difference | $230 | |

| Purchased Debt (Preferred D) | $226 |

* Ratio’d 4/3 tiimes

The company needs cash growth, approximately $100 million, for capital expenditures to remain cash flow neutral. Apparently, management expects growth from Permian Basin with an estimate for the 4th quarter of 600 MB/day, above the 580 in the 3rd quarter. Adding the last few quarters in EBIDTA from the Permian using the above slide yields $210 million. At 600,000 entering into 2023, a simple ratio approach yields $260 million or $50 million above last year. In an addition, repurchasing 30% lowers interest payments from $65 million to $45 million a savings of approximately $20 million. Other minor growth, including expected continued improvement from the lucrative basin should provide NuStar with approximately $70 – $80 million in cash for capital.

It is tight, but over the next four quarters, NuStar should generate enough cash to pay down the Preferred D debt incurred leaving $70 – $80 million plus for capital. When investors consider the other portions of the business summarized above, it seems more than plausible that NuStar should remain cash flow neutral internally. Remember that management still continues its internal evaluation for cash flow savings saving having already identified $100 million thus far, $50 million being from capital in 2023. A reduction of $50 million in 2023 might equal the reduction needed for 2023 spending to drop near $80 million. Investors will have to wait and see at the year end report. Some of the savings comes from the Permian, with 2022 spending creating tentacles now being filled in from the producers. Also, the leverage now slightly exceeds 4 with the exit of 2022. Total debt at face value equals $3.32 billion.

A Brightly Shining Star

As stated above, the company put itself in position to begin early the repurchase of D shares. The target is now 2024 to complete the purchase moved up almost two years. The next slide summarizes the transaction.

NuStar Energy

The company formally announced the transaction:

On November 16, 2022, NuStar Energy L.P., a Delaware limited partnership (the “Company”), entered into a purchase agreement with EIG Nova Equity Aggregator, L.P. and a purchase agreement with FS Energy and Power Fund (collectively, the “Purchase Agreements”), pursuant to which the Company agreed to purchase an aggregate of 6,900,000 units of its Series D Cumulative Convertible Preferred Units (the “Units”), at a price per Unit of $32.73, or an aggregate purchase price of approximately $226 million. The transactions contemplated by the Purchase Agreements closed on November 22, 2022, and the Company funded the transactions using borrowings under its unsecured revolving credit agreement.

With the D share repurchase underway and what appears to be the needed cash to extinguish the purchase within twelve months, NuStar finances just improved significantly. At $775 plus million EBITDA estimated for the next four quarters, leverage based on face value decreases to near 4.1. Once paid off, the leverage once again falls to less than 3.9.

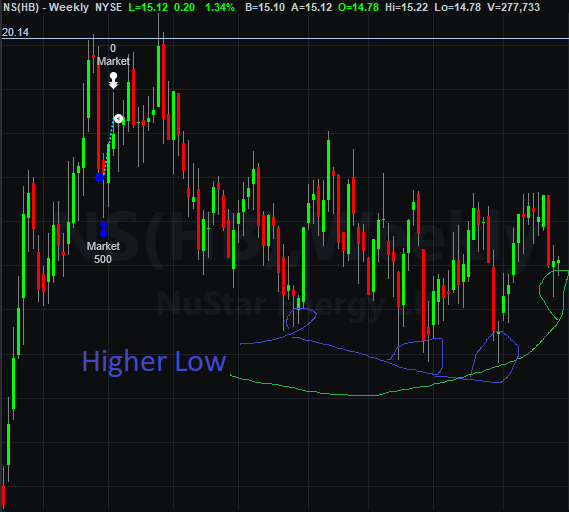

Charts, Always Charts

Next, included is a weekly chart for NuStar generated using TradeStation Securities software.

TradeStation

Of most importance for investors is that, thus far, the lows are higher in the $15 range, significantly above the $13s prior. We moved our short call options to $17.5 from $15 to compensate for what we believe will be a higher range going forward. NuStar pays $1.60 a year in distributions. We believe that a forward range might be between $15 and $18 to $20. With improving financials, lower payouts for preferred shares, the price range also stands to continue improving. We don’t see any change yet in distribution for at least two more years, but the ability for management to accelerate the process will improve and investors will likely drive the price range higher.

Risk/Reward

Risks do abound much in today’s financial environment. A recession both in the world and in the United States stands as almost a certainty. But management discussed the shortage already in place in the general energy markets. NuStar will see significant inflation adjustments in its contracts through the higher level of inflation already in the market place. Another risk, government’s interference into the fossil fuel business still exists with this Administration’s unfortunate distaste for fossil energy. Also, once the D shares are purchased, the company faces a major refinancing of $600 million in 2025. See slide 28 in the latest presentation. Yet, the company’s management plans, especially in recent years, are working itself through the difficult period.

We can’t see a scenario outside of a worldwide shutdown such as in 2020 that could derail NuStar Energy L.P.’s progress. NuStar’s finances jumped a major huddle. We are continuing to hold our investment and may add small margins in the future.

Be the first to comment