Deagreez/iStock via Getty Images

Investment Thesis

Nucor (NYSE:NUE) gets crowned as a Dividend King. Its Q4 results were middle of the road. But what truly stands out and why investors should take notice here is that Q4 marked a low point for steel prices.

With steel prices having found their bottom, it’s difficult to get excited about Nucor’s 2023 prospects and valuation.

Let’s get to it.

Nucor’s 2023 Prospects

NUE Q4 2022

Yesterday, during Nucor’s earnings call management stated,

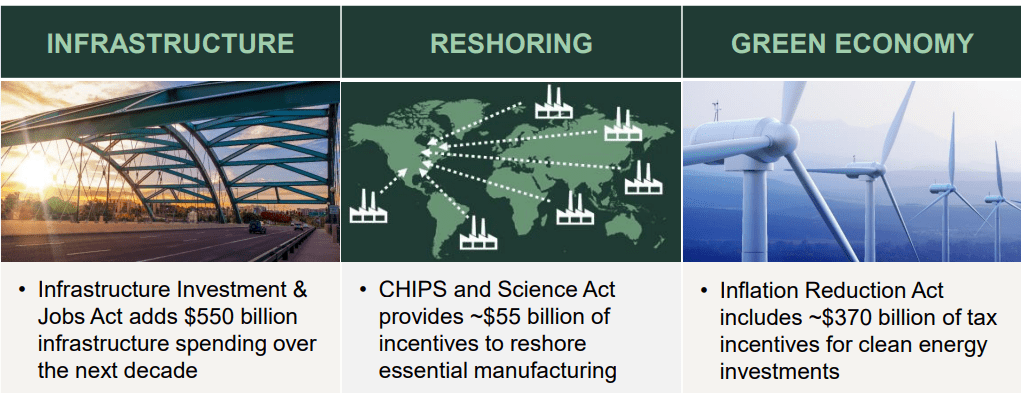

[…] non-residential construction spending continues to be robust, federal support for infrastructure and energy projects will begin to show impacts on demand in 2023.

Other positive drivers of demand include re-shoring of manufacturing, energy infrastructure demand, clean energy and storage projects, EV factories and semiconductor plants.

These are the key themes to think about for 2023, reshoring of manufacturing, large infrastructure investments, and grid modernization. A continuation of the key drivers of 2022. No new news here.

Won’t Steel Prices Drop Due to the Competition?

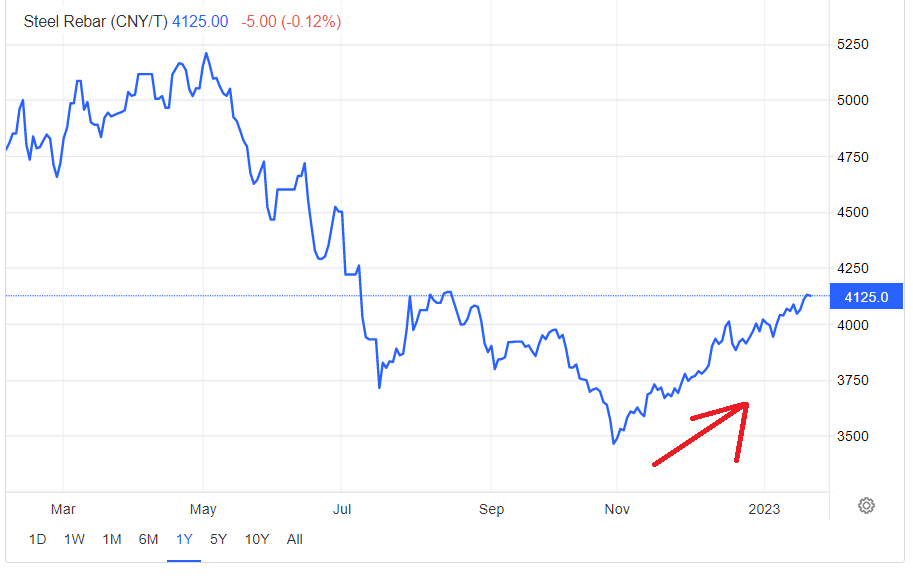

Trading Economics

As you can see above, since November, steel prices have found a hard floor in October. What this means is that demand for steel is going up. And what this also means is that there are plenty of companies around the world with very cheap workforces eager to ramp up their steel production to match steel demand.

But the problem for them is that energy costs outside of North America are uneconomically high. And in some cases, such as in Europe, the government is actually asking them to reduce production.

Construction News

I’m not saying that those steel companies are no longer producing steel. I’m simply stating that this provides Nucor with a significant competitive advantage in its ability to undercut competitors and gain market share.

The Wonders of Cash Flow

NUE investors presentation

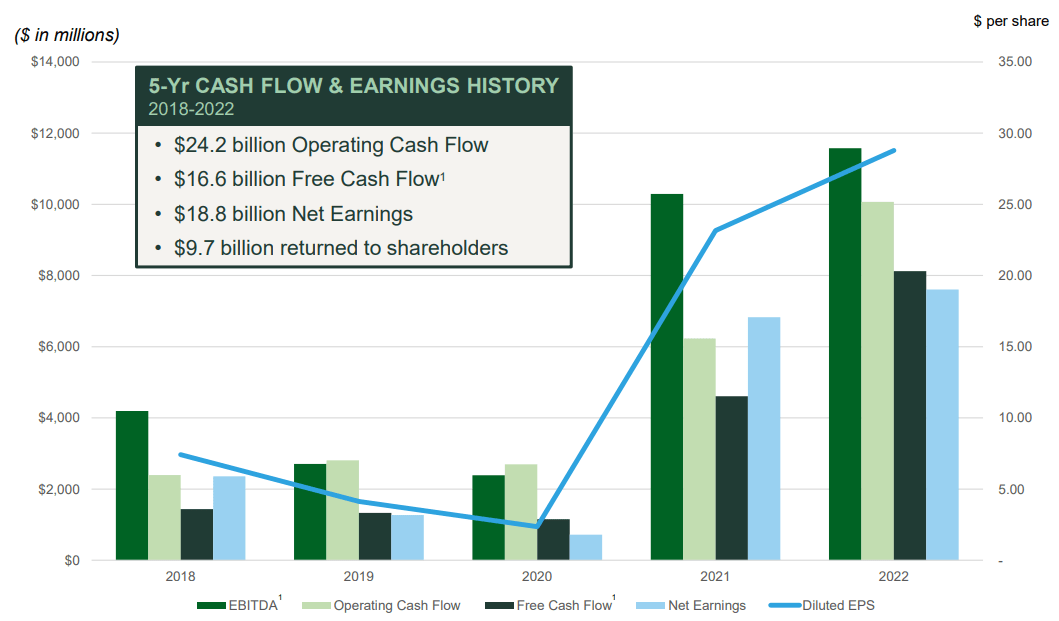

In the graphic above we see the wonders that cash flows can do to a very capital-intensive cyclical business.

What you see is two consecutive years of record cash flows. Having strong cash flows for two consecutive years can be a blessing or course.

It can be a curse if management starts to forget the prior period and starts deploying excess free cash flows into empire-building projects and squandering precious capital.

But it can be wonderful if the cash flows allow the business to transform its balance sheet.

More specifically, note that in Q4 of last year, Nucor’s balance sheet held about $4 billion of net debt. Now, twelve months later, its net debt has fallen to $2 billion of net debt.

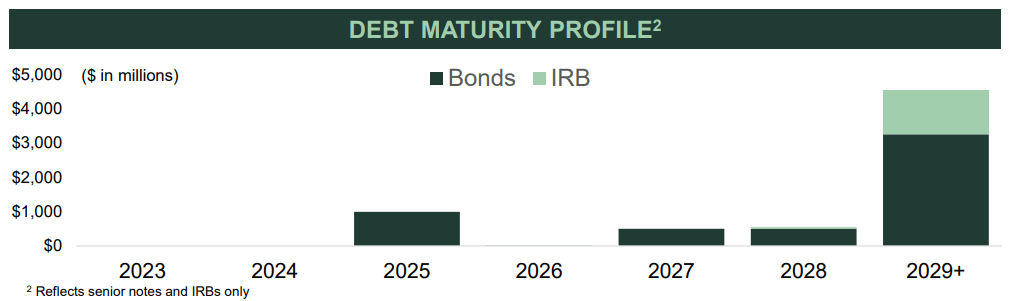

NUE investors presentation

What you see above is a reminder that Nucor’s balance sheet holds some debt that it’s easily manageable in 2025, and then nothing of significance until 2029 and beyond.

Looking ahead to 2023, Nucor will continue to be committed to returning 40% of its earnings back to shareholders. This could see Nucor returning at least $1 billion back to shareholders on top of increasing its intrinsic value.

Nucor, Dividend King

Dividend Kings are companies that have to be in the S&P500 (SPX) and paid out a raising base dividend for 50 years. Nucor has achieved this.

This isn’t all that important in the grand scheme of things. But it’s important to a certain group of investors and it typically get a loyal following of investors that only invest in Dividend Kings. Something to keep in mind.

More concretely from my perspective, I should note that Nucor has the strongest credit rating in the North American steel sector. This means that when steel prices turn lower, Nucor’s balance sheet will provide it with ample staying power.

The Bottom Line

I believe that through its dividends and buybacks, Nucor will return at least a 3% combined yield. But if steel prices remain stable at the current price Nucor could be a very compelling opportunity in 2023.

Again, as I alluded to throughout, Nucor is a large and very well-established Dividend King. It’s cheap but not the cheapest steel company around.

My point is that this is the sort of company that makes sense to invest in if you don’t want too many frills.

Be the first to comment