kemalbas

Brazil’s central bank, like many other central banks around the world, followed in the Fed’s footsteps in 2022 and increased benchmark interest rates aggressively to counter rising inflation. Thanks to falling inflation in recent months, the bank has held Brazil’s benchmark Selic interest rate steady at 13.75% since October 2022. However, the effects of prior increases, which numbered 12 in total, are still reverberating across the country’s banking industry.

Brazilian lenders have, for example, taken a more cautious approach to unsecured lending as borrowers in the space are viewed as riskier bets during times of elevated interest rates and weaker economic growth. These headwinds have weighed on the unsecured lending business and led to a negative shift in investor sentiment toward players with high exposure to the lucrative but risky space. This includes Nu Holdings Ltd. (NYSE:NU), known as Nubank, the largest digital bank by customer base in Brazil.

Since its founding in 2013, when it started offering credit cards to customers with poor credit histories who had been sidelined by traditional banks, NU has aggressively tightened its grip on Brazil’s unsecured lending market. It today offers a wide range of consumer banking products and services to millions of Brazilians through its digital channels and is a household name, with its customer base representing 39% of the country’s adult population as at Q3 ’22.

Disconnect between stock and business

Despite becoming the dominant digital bank in Brazil in the span of a decade, NU has lost more than half its value since its IPO in December 2021 as investors price in factors like higher interest rates and its impact on unsecured lending. NU’s profile as a leading fintech player, while good for publicity, has served against it in the market in the past year as investors have generally been bearish towards growth stocks and tech names.

With NU currently trading around 10% above its 52 week low (which is also its all time low), there is a great opportunity to buy a good business at a great price. The growing disconnect between the stock and the business means the upside could be immense. NU’s total annual revenues have increased almost fourfold from $425.1 million in 2020 to $1.47 billion in the trailing twelve months, while GAAP losses have narrowed from $171.5 million to $133.3 million over the same time. During this time, NU has expanded to Mexico and Latin America, increased its customers more than threefold from 20.1 million in Q1 2020 to 70.4 million in Q3 2022, and launched a slew of new products, including offerings in insurance, investments and even crypto.

Meanwhile, the stock has lost more than half of its value even as the business’s performance and growth prospects remain stronger than ever and the company, which marks its tenth anniversary this year, charts its way to profitability.

Growing when it matters and making bold decisions

When it comes to fast growing industries like fintech, the real test of whether or not a company has a winning business model is its ability to sustain growth in times of general industry weakness. NU has been doing precisely this, growing its customer base and revenues robustly amid general weakness in the unsecured lending industry.

Total revenue surged 171% to a record $1.3 billion on an FX-neutral basis for the quarter ended Sept 30, even as customer numbers hit 70.4 million and engagement remained high at 82%. In terms of profitability, gross profit increased 90% to a record high of $427 million on an FX-neutral basis while net income came in at $63.1 million on an adjusted basis.

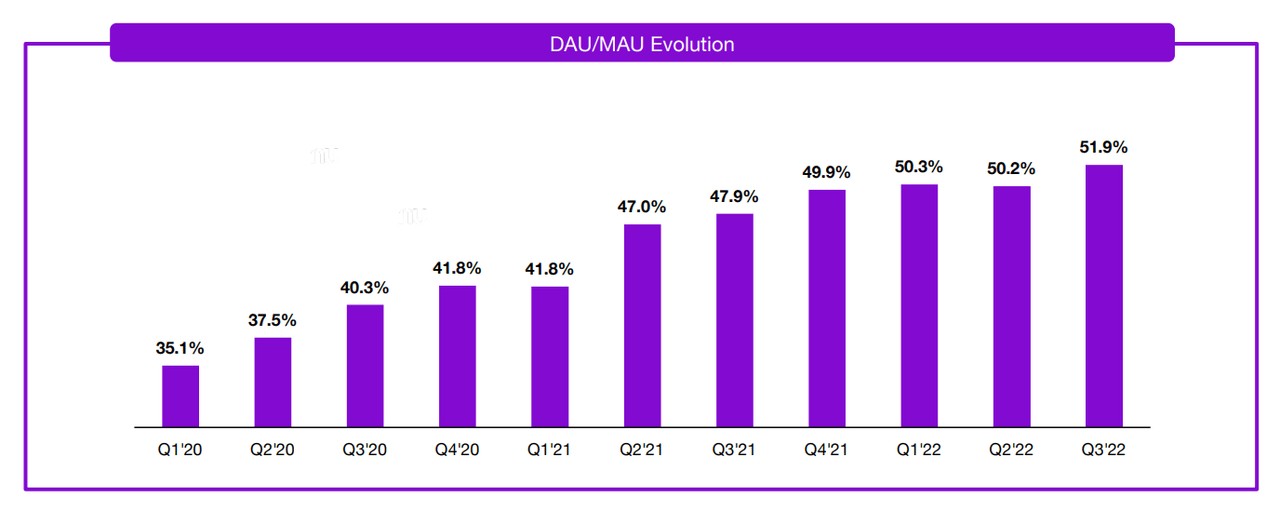

The highlight in NU’s Q3 performance that impressed me is the level of engagement as measured by the Daily Active Users to Monthly Active Users (DAU/MAU) ratio. NU has been able to steadily grow this ratio since Q1 2020. As the chart below illustrates, more than half of its monthly active users log into the app daily vs 35.1% in Q2’20.

Nubank Q322 Earnings Presentation

The fact that existing customers are using NU’s services more frequently is bullish when you think of the important role that user stickiness plays in any digital platform’s growth prospects.

I also like the fact that NU’s management hasn’t shied away from making bold decisions that can improve profitability. In July 2022 it implemented a new policy where new deposits in accounts in Brazil remunerate customers only if the amount stays in the account for more than 30 days. The customer will then receive that period’s income retroactively, meaning the account’s value proposition is not lost entirely.

This move has lowered its cost of funding, with the benefit of that expected to be seen fully in 2023. NU’s CFO Guilherme Lago, noted on the Q3 earnings call that cost of funding has been declining, reaching 95% of CDI – Certificate of Interbank Deposit is the local interbank benchmark rate, which is attached to Brazil’s key interest rate.

Lower costs of funding have a positive impact on earnings since they increase the amount a bank makes for every dollar lent to customers. In connection with this, BofA Securities analyst Mario Pierry in September increased NU’s price target to $5.50 from $5.00 as he sees lower funding costs helping earnings growth in the coming year.

Strong financial shape and diversification

While NU is still not profitable on a GAAP basis, its margins are improving, it has positive adjusted net income and its balance sheet is remarkably strong. It has total debt of $556.03 million against total cash of $3.69 billion as per the last report.

NU’s growth could further accelerate if its foray into secured lending is successful. It is looking at ramping up its secured lending line of business which includes payday lending and investment-backed loans.

Improving the quality of its credit portfolio amid high interest rates is a strategic move as it will help cushion gross margins. Secured lending generally requires lower upfront provisions relative to unsecured lending, meaning growth in NU’s secured loan book will put less pressure on gross margins and accelerate its march to GAAP profitability.

Borrowing a leaf from Terry Smith

Warren Buffett’s Berkshire Hathaway (BRK.A) (BRK.B) bought a $1 billion stake in NU in 2022 after investing $500 million before the 2021 IPO. Considering his long-term investing philosophy, this is a positive sign. I choose to emulate this great legend when it comes to NU and view it as a long term play that is executing in line with if not ahead of expectations.

There’s another legendary investor whose philosophy I have also adopted when thinking about NU and the investment approach best suited to the opportunity. This legendary investor is British fund manager Terry Smith, founder and CEO of Fundsmith, a London-based hedge fund. Smith noted in his 2022 annual shareholder letter that the fund continues to apply a simple three step investment strategy: Buy good companies, don’t overpay and do nothing.

I believe investors can profit from this approach in NU as its current share price represents a discount given the growth and prospects of the underlying business. I’m down around 20% since I first bought NU but I’m comfortable with my investment here despite the red blob in my brokerage account, which while discouraging, hasn’t scared me away or deterred me from adding on dips.

Be the first to comment