dgdimension/iStock via Getty Images

NOW Inc. Has Upsides

In 2022, NOW Inc. (NYSE:DNOW) will look to grow its share of pipe valves and fittings for the wellhead hookups and tank battery facilities. As the upstream-related projects grow, it helped add midstream customers to the natural gas and associated produced water projects. It also added to the digital offerings, including eSpec digital product configurator and dryer equipment packages in the recent past. The renewable space has started providing stainless vein pump packages to a biodiesel refiner, bio water pumps for an electric truck vehicle manufacturer, and a carbon capture and storage project.

However, DNOW’s critical challenges include supply chain issues, geopolitical volatility, and possible demand destruction due to COVID. Its balance sheet remains robust given the zero debt and sufficient liquidity. But, free cash flows turned negative in FY2021. The stock’s relative valuation is attractive at the current level. So, I think the stock price is due for a rise, and investors may consider buying it in the short-to-medium term.

Market Activity And Outlook

NOW Inc.’s Filings

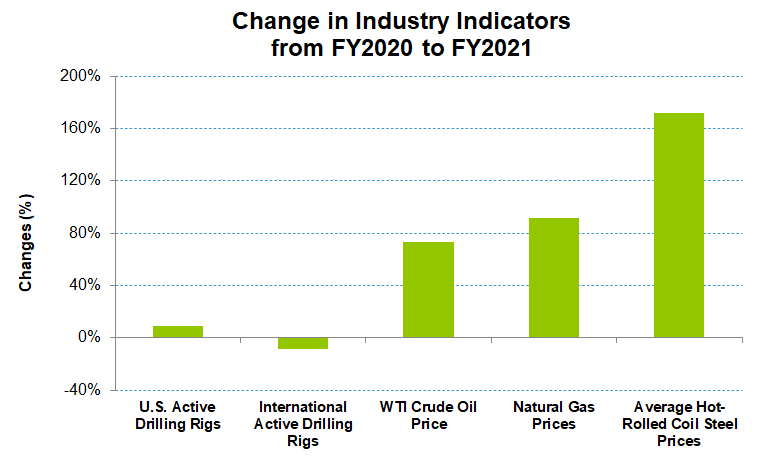

Over the past year, rig count, crude oil price, and completion activity have favored a recovery for DNOW’s US segment. The crude oil price spiked by 73% between FY2020 and FY2021, leading to a 9% drilling rig growth. In this scenario, the management has been addressing a key issue is the improvement in vendor consideration levels, which can affect margin favorably. The second critical issue has been the pricing of its line pipe and high steel content products to offset the effect of commodity inflation. In the US, the company is set to see improved market fundamentals. In Canada, activity in the energy space should increase. However, the international energy activity slowed down by 9% in the past year.

I discussed the company’s business in my previous article. With the private operators, DNOW looks to grow its share of pipe valves and fittings for the wellhead hookups and tank battery facilities. The integrated supply chain services customers deliver value-added services, including lowering their lifting costs. As the E&P capex grows, the company will improve its topline in 2022.

FRED Economic data

DNOW can recover more sharply in 2022 as the market expands. In Q1 2022, the company expects its US revenues to increase by mid-single-digits. Gross margin, however, can contract to 21.9% from 23.4% in Q4. On an annual basis, in FY2022, it expects revenues to increase in the low to mid-teen percentage range, translating into $200 million in additional revenue for the year. The EBITDA margin can expand by a high teen percentage range. The cost side, too, can run high following the current geopolitical matters and supply chain disruption. The COVID situation remains another uncertainty. While the continued recovery will keep DNOW on target, a worsening situation in China can derail its target.

Project Awards And Strategies

In Q4, the company’s PVF sales expanded through several new contracts in the Permian. It also signed an agreement to provide lithium extraction. It provided PVF for several compressor station repairs In the Southeast following hurricane Ida. In Haynesville, it secured orders for three well-pad facilities. The uptick in drilling and gathering systems rubbed off with the midstream takeaway capacity utilization. So, capex in midstream increased. Thus, the company added midstream customers in the natural gas and associated produced water projects.

DNOW has started providing stainless vein pump packages to a biodiesel refiner and bio water pumps for an electric truck vehicle manufacturer in the renewable and alternative energy market. It is also working on a carbon capture and storage project in Alberta. In the high-tech industry, it is working with a producer drilling wells to extract helium.

Digitization And Renewable Initiatives

The company’s DigitalNOW platform and shop.dnow.com platform display product catalogs and help develop customized workflow solutions. Its eSpec digital product configurator and dryer equipment packages helped reduce greenhouse gas emissions and replace gas pneumatic systems.

In the non-traditional energy business, it provides stainless vein pump packages to a biodiesel refiner and bio water pumps for an electric truck. It received awards for zero-emission actuated valves for Canada’s carbon capture and storage project. It also received an order to extract helium in drilling exploratory wells. So, the company sees opportunities in carbon capture and high-tech industrial manufacturing.

Q4 Drivers And Margin Analysis

Seeking Alpha

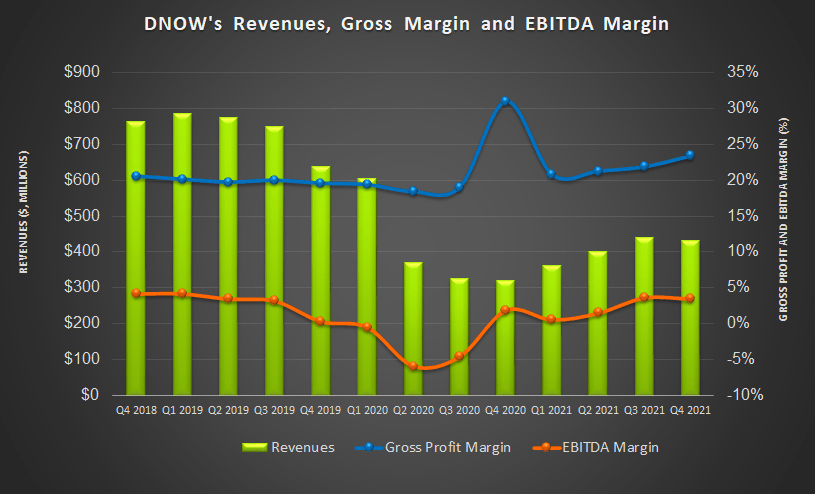

The company’s US revenues decreased by 3% in Q4 2021 compared to Q3, following the typical seasonal effects. Investors may note that the US energy centers contributed ~79% of total US revenues. However, revenues from Canada increased by 6% during this period as the Canadian energy market improved and the company expanded its customer base.

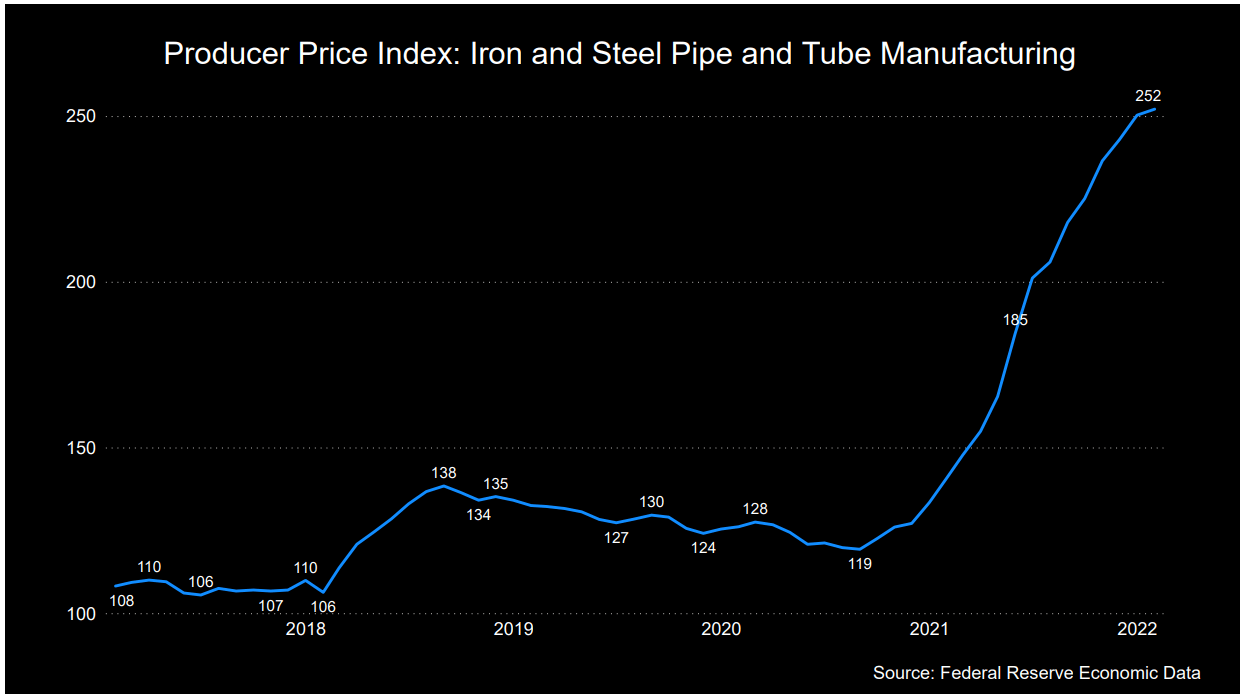

The company’s gross margin expanded by 150 basis points in Q4 due to lower transportation costs and lower inventory charges. While steel input price inflation adversely impacted costs, DNOW more than made it up through margin growth as it moved towards high-value products and leveraged better supplier-partner relations.

Cash Flows And Balance Sheet

In FY2021, higher working capital requirements pushed DNOW’s cash flow from operations (or CFO) significantly lower (84% down) than a year ago. Capex plus acquisition spend on Flex Flow was much higher in FY2021. In effect, free cash flow (or FCF) turned negative.

Its liquidity was $561 million as of December 31, 2021. DNOW does not have any debt, which puts it in a much more advantageous position than its peers (FAST, MSM, and MRC) as of December 31, 2021. During Q4, it amended its revolving credit facility, extending it through December 2026.

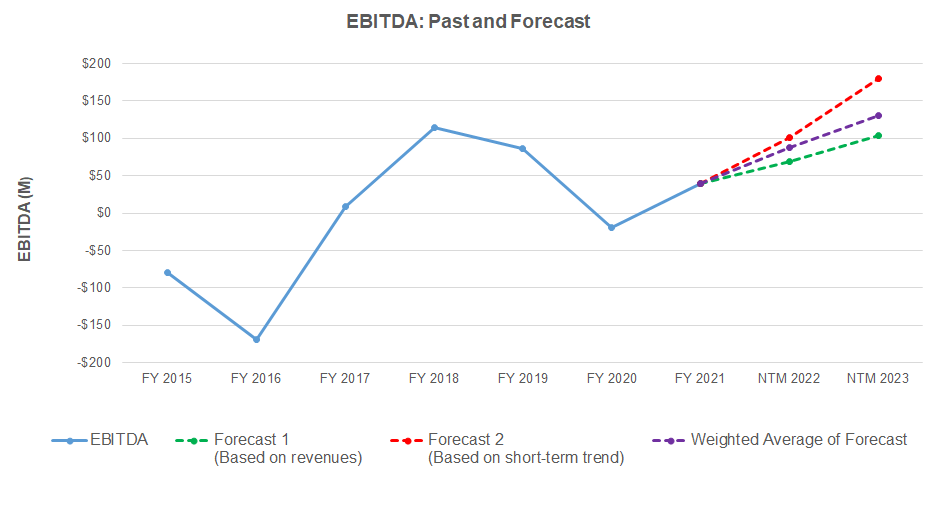

Linear Regression Based Forecast

Author created, Seeking Alpha, and EIA

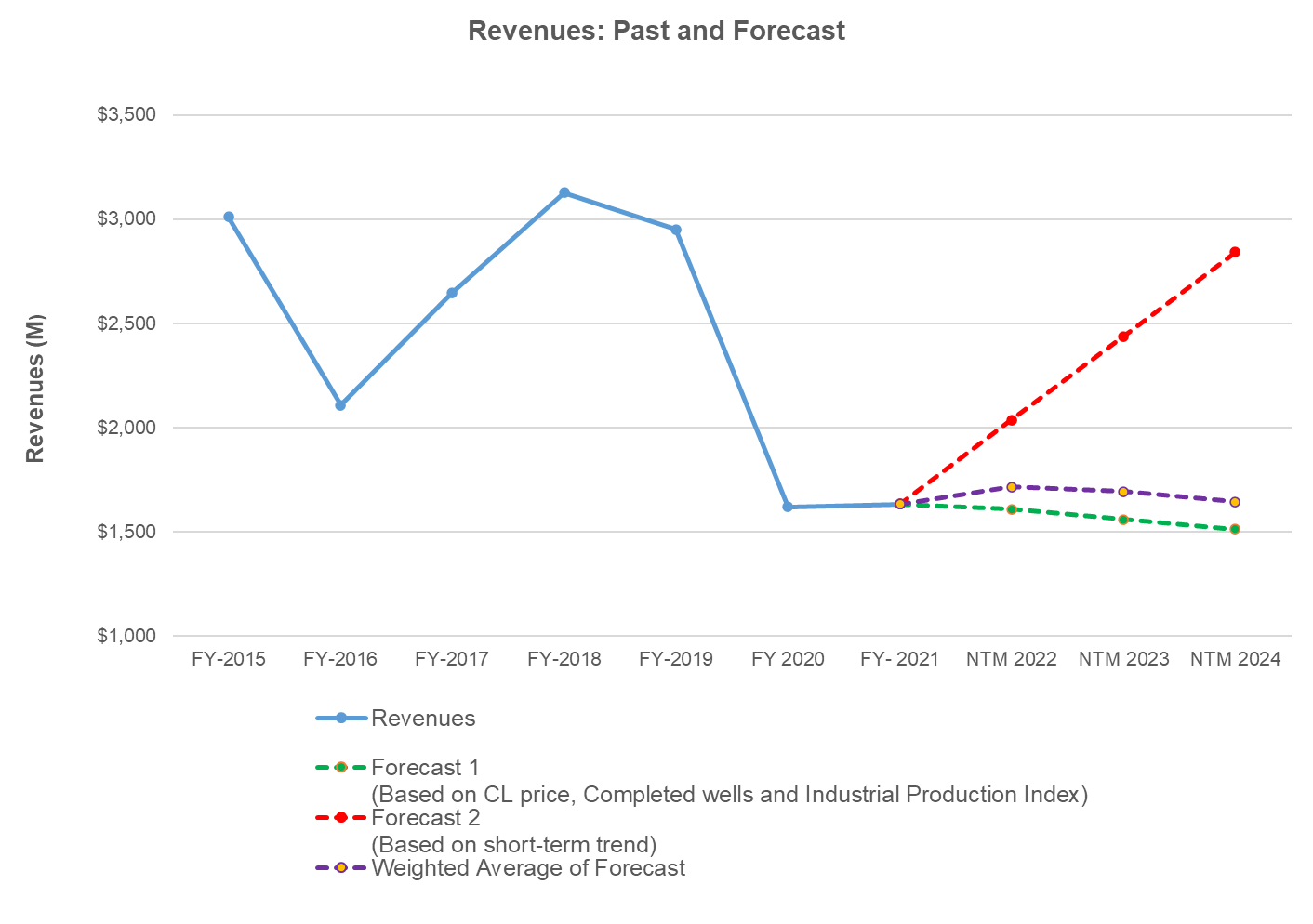

Based on a regression equation between crude oil price, completed well count, Industrial production Index, and DNOW’s reported revenues for the past seven years and the previous four quarters, revenues can increase in the next twelve months (or NTM) modestly. However, it can plateau in NTM 2023.

Author created and Seeking Alpha

Based on a regression model using the average forecast revenues, I expect the company’s EBITDA to more than double in NTM 2022 and will continue to increase in NTM 2023.

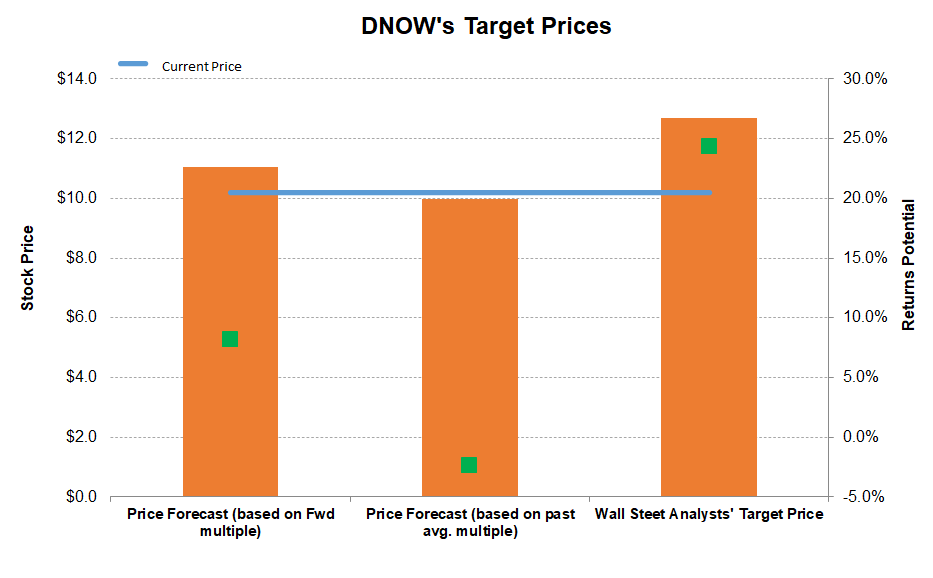

Target Price And Relative Valuation

Author created and Seeking Alpha

DNOW’s returns potential (94% upside) using the forward EV/EBITDA multiple (10.4x) is lower (8% upside) than Wall Street’s sell-side analyst expectations (24% upside) but higher than returns potential (2.4% downside) based on the past EV/EBITDA multiple.

The company’s EV/EBITDA multiple (22.4x) is in line with its peers’ (FAST, MSM, and MRC) average. DNOW’s forward EV/EBITDA multiple contraction is steeper than its peers’ EV/EBITDA contraction, typically resulting in a higher EV/EBITDA multiple compared to peers. So, the stock is undervalued on a relative basis.

What’s The Take On DNOW?

Seeking Alpha

In early 2022, DNOW’s strategies will hinge on the interplay between PVF (pipe, valves, and fittings) price hike and the cost rise in line-pipe and high steel content products. As the drilling activities rise, the company looks to grow its share of pipe valves and fittings for the wellhead hookups and tank battery facilities. Along with value-added services, their lifting costs will also be lower. So, in Q1, I think its revenues will increase, and its margin will expand.

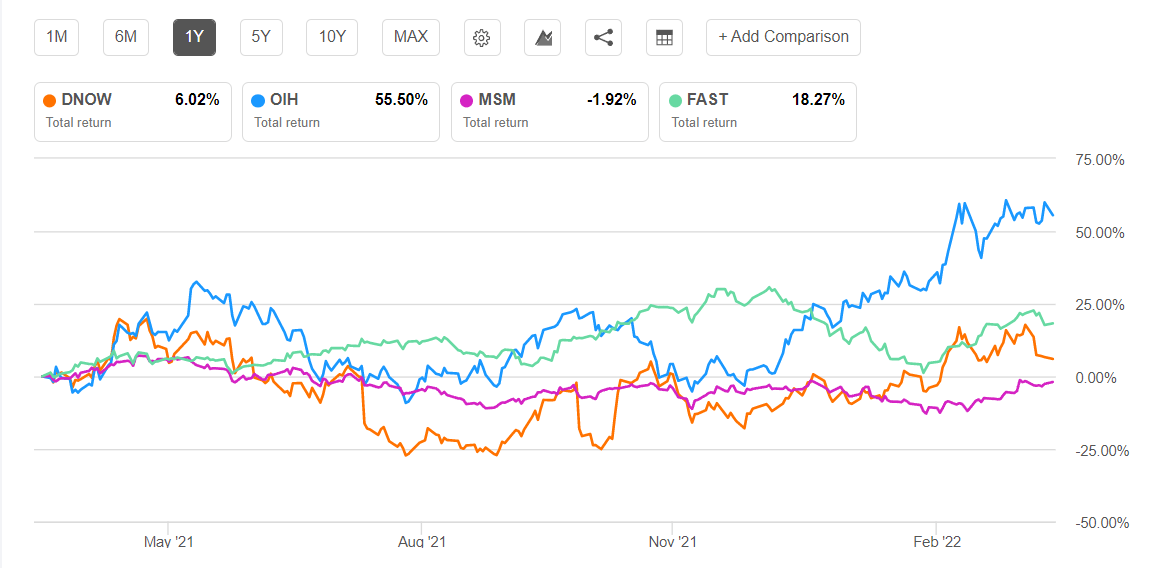

Supply chain issues and geopolitical volatility will keep commodity prices elevated on the cost side. The demand side, too, remains uncertain given the evolving COVID situation. True, it has no debt and robust liquidity. But, free cash flows turned negative in FY2021. So, the stock underperformed the VanEck Vectors Oil Services ETF (OIH) in the past year. Nonetheless, given the relative valuation, I think the stock price will rise in the short-to-medium term.

Be the first to comment