Introduction and Thesis

I like regulated utilities. They have guaranteed rates of return and generally captive markets leading to long-term earnings per share growth. In turn, this leads to long-term dividend growth. In this article I discuss NorthWestern Corporation (NWE), one of my favorite utilities. The company is not well-followed, but it should be. NorthWestern’s trailing 10-year return exceeds that of the utility sector. In addition, the yield is over 3.7% as of this writing and the company is a Dividend Contender. Granted, there are utilities with higher dividend yields and growth prospects. But that often comes with risk of unregulated generating operations and weaker balance sheets. Sometimes, slow and steady is better. The utility does have a risk in that it does not generate all of its needed power. Capacity deficits are met by buying power in the open market, leading to cost risk. However, I think the positives outweigh the negatives here. I view the stock as a long-term buy.

(Source: NorthWestern Corporation)

Overview of NorthWestern Corporation

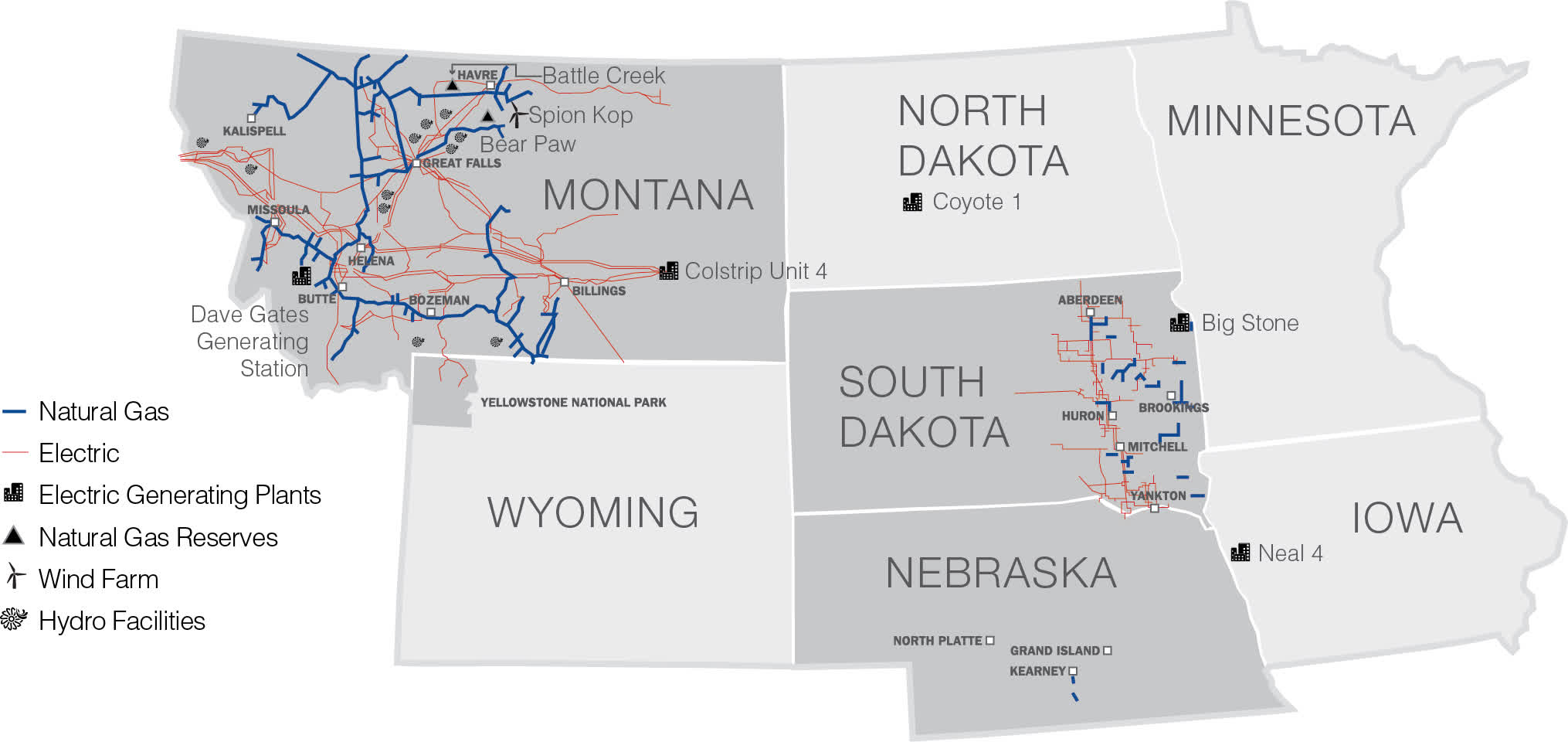

NorthWestern Corp. provides electricity and natural gas services in Montana, South Dakota, Nebraska, and Yellowstone National Park to about 734,800 customers. The company traces its roots to 1923. It took its current form in 2002, when Northwestern Public Service Co. bought Montana Power Co. The utility operates in two segments: Electric Operations and Natural Gas Operations. Electric Operations serves customers in Montana and South Dakota and owns about 35,285 miles of transmission and distribution lines. The company generates ~1,278 MW of power from 11 hydroelectric dams, a jointly owned coal plant, natural gas units, and three wind farms. The utility also purchases power on the market, since it does not generate enough for its peak needs. Hydro, solar, and wind make up 58% of electric supply. Natural Gas Operations owns about 9,483 miles of pipelines and storage facilities and serves all three states.

(Source: NorthWestern Corporation)

NorthWestern Corporation Revenue Growth and Margins

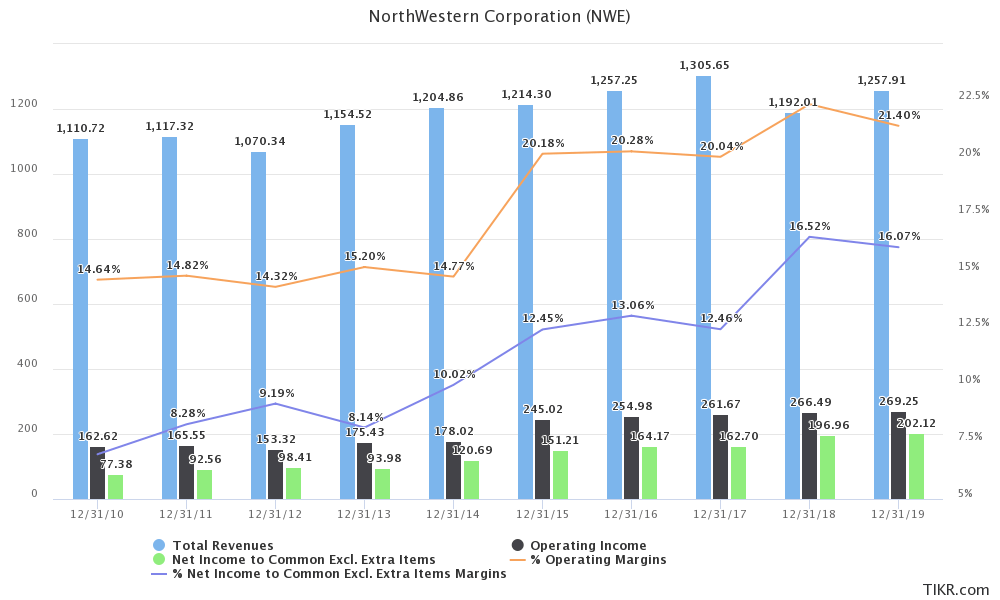

NorthWestern Corp. has generally increased revenue and margins over the past decade. For regulated utilities, revenue increases as the rate base increases. The rate base has increased at a compound annual growth rate, or “CAGR”, of 10.7% over the past decade. Revenue increases due to population growth and if a utility’s regulator permits a rate increase. NorthWestern, like most utilities, periodically applies for increases in the rate base and return on equity. Increases in revenue drop to the bottom line, leading to long-term increases in earnings per share.

NorthWestern does not operate in the highest-population growth region of the country. But with that said, above-average population growth will drive growth in the utility’s territory. In the past decade, CAGR for electric customers was 1.12% over the past decade, which is greater than the national average of 0.86%. The CAGR for natural gas customers was 0.92%, compared to 0.61% for the national average. Over the next five years, population in Montana is expected to grow at 4.39%, South Dakota at 4.8%, and Nebraska at 3.29% annually. These exceed the national average of 3.27%. This growth will drive increases in the rate base and thus revenue.

NorthWestern is very dependent on Montana for revenue (~80%), where the utility is permitted a ~9.65% return on equity and a ~7.42% return on rate base. The utility also was approved for a $10.5 million rate increase. This is a good sign that future revenue will be higher.

(Source: TIKR.com)

NorthWestern has successfully raised its margins over the past decade. This has come by controlling costs, particularly operating expenses. Over the past decade, operating expenses have been relatively flat. For instance, total operating expenses were $948 million in 2010 but were $989 million in 2019. We can see that in 2013-2015 time period, NorthWestern’s margins jumped. This is likely attributable to the acquisition of 11 hydroelectric dams in Montana during that time. But margins continued to rise each year to 2019. I believe that this is a result of the utility’s transition away from expensive coal power to hydro, solar, and wind power plus natural gas peaking units. Today, roughly 60% of power is from renewal sources, which benefits NorthWestern, as costs will be lower, in turn leading to higher margins. In general, the cost of operating a coal plant is more expensive than renewable energy.

Risks to NorthWestern Corporation

The major risk to NorthWestern is that it falls short of meeting its peak power needs by about 645 MW. This means the company must buy power on the open market, usually when demand and thus prices are high. The unmet peak power is expected to rise in the future. This deficit can potentially lead to higher costs, lower margins, and affect cash flows. The utility is attempting to partially address this deficit by purchasing an additional 185 MW of power generation (or 25%) of the Colstrip 4 coal plant. This would increase NorthWestern’s ownership stake to 55%. The deal is for $1.00 (one dollar) with a 5-year agreement for NorthWestern to sell 90 MW of power back to Puget Sound Energy. It would reduce the peak capacity deficit by a decent amount. In addition, NorthWestern is adding 60 MW of natural gas capacity in South Dakota further reducing the deficit.

The utility also faces risks for a regulatory environment that does not permit rate base or rate of return increases. Interestingly, NorthWestern has relatively minor exposure to coal power, so the risk of increased environmental regulation impacting the utility is low.

NorthWestern’s Dividend and Safety

NorthWestern has paid a growing dividend for 14 years, making it a Dividend Contender. The current forward dividend is $2.40 per share, giving a yield of over 3.7% at today’s stock price. The dividend is reasonably safe from the perspective of earnings. Consensus 2020 earnings per share is $3.51. Hence, the payout ratio is approximately 68.4%, which is in the 60-70% range desired by the company. This is above my threshold of 65%. But it is a good value for utilities, which tend to have higher payout ratios. Many larger utilities have payout ratios over 70%, such as Duke Energy (D), or Southern (SO), or Dominion (D).

The dividend is also reasonably safe from the perspective of operating cash flow. Utilities often have high capital expenditures exceeding operating cash flow. The difference is made up by debt. With that said, in 2019, the dividend cost $115 million and operating cash flow was $316 million, meaning that the annual dividend can be paid without interruption.

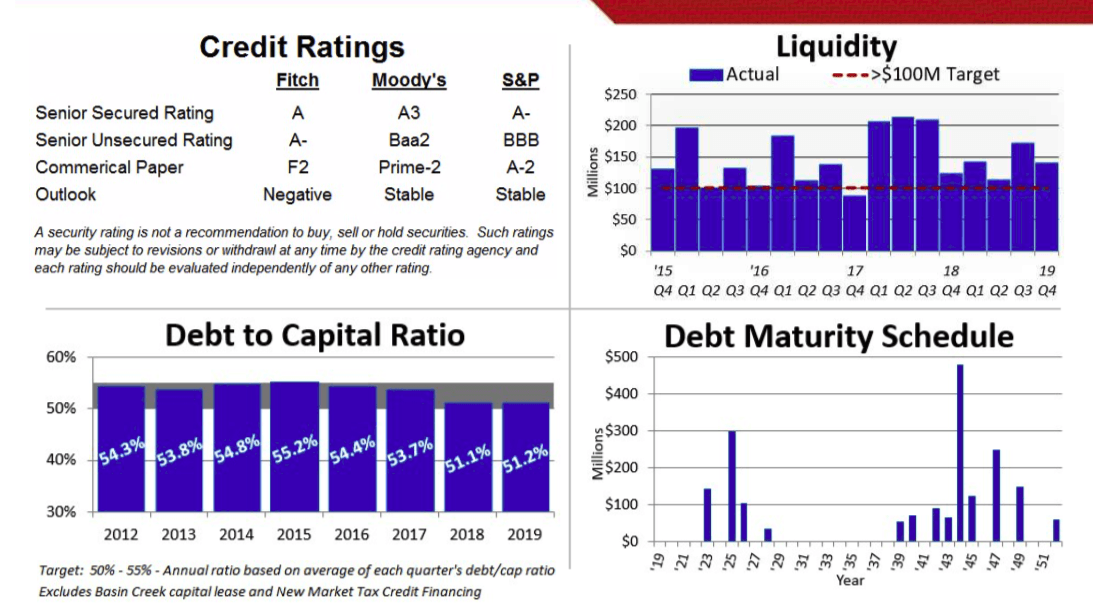

Most utilities have high debt loads, and NorthWestern is no exception. At end of 2019, the utility carried no short-term debt, and long-term debt was $2,233 million. This was offset by only $5 million in cash. But interest coverage is about 2.8X and cash flow coverage is about 3X, meaning that NorthWestern can meet its obligations. The risk, of course, is the aforesaid high capacity deficit, which can potentially lead to fluctuations in earnings and cash flow. However, the utility has liquidity over its $100 million target. All three major rating agencies give NorthWestern investment grade credit ratings. The debt-to-capital ratio is just slightly over 50%. Lastly, no long-term debt matures until 2023, providing the company flexibility in the face of market conditions and also economic downturns. Overall, I think the dividend is secure from the perspective of debt.

(Source: NorthWestern Investor Update, March 2020)

NorthWestern’s Valuation

Now let’s examine the valuation of NorthWestern. The forward price-to-earnings ratio based on consensus 2020 earnings per share of $3.51 is now about 18.4. This is above the trailing 10-year average multiple of ~16.2X.

However, utilities have more recently been valued at a higher-than-historical-average multiple. This is largely due to low interest rates for U.S. Treasuries and perceived stability of utility dividends. Hence, we will use 18.0 as the earnings multiple to determine a fair value of $63.18. Applying a sensitivity analysis using P/E ratios between 17.0 and 19.0, I obtain a fair value range of $59.67-66.69. The current stock price is ~97% to ~108% of my estimated of fair value. The current stock price is ~$64.40, suggesting that the stock is slightly overvalued based on earnings.

Estimated Current Valuation Based On P/E Ratio

|

P/E Ratio |

|||

|

17.0 |

18.0 |

19.0 |

|

|

Estimated Value |

$59.67 |

$63.18 |

$66.69 |

|

% of Estimated Value at Current Stock Price |

108% |

102% |

97% |

(Source: DividendPower.org Calculations)

How does this compare to other valuation models? Morningstar is known to use a fairly conservative discounted cash low model and provides a fair value of $64.86. The Gordon Growth Model gives a fair value of $80 assuming a desired return of 8% and a dividend growth rate of 5%. An average of these three models is ~$69.35, suggesting that NorthWestern is undervalued at the current price.

How does NorthWestern compare to other similar utilities? We make the comparison to three other companies: Portland General Electric Company (POR), Black Hills Corporation (BKH), and Avista Corporation (AVA). One can see from the comparison that NorthWestern is probably fairly valued relative its peers.

Technical Comparison of Valuations

|

NorthWestern |

Portland General Electric |

Black Hills |

Avista |

|

|

Price-to-earnings ratio (Fwd.) |

17.4 |

20.0 |

18.6 |

21.1 |

|

EV-to-EBITDA (TTM) |

12.1 |

9.7 |

12.8 |

12.0 |

(Source: Dividend Power and Seeking Alpha)

NorthWestern is a very safe stock and is not volatile with a trailing 5-year beta of ~0.46. The utility has a conservative balance sheet and has the advantage of being a regulated monopoly. Morningstar gives it a narrow moat. Value Line gives the stock a safety score of “2”, financial strength rating of “B++”, a stock price stability of 100, and an earnings predictability of 85. These are good scores but not the best. The stock’s debt has an investment grade credit rating from all three major rating agencies, as seen in the chart above.

Final Thoughts on NorthWestern

Market volatility is now below 50 as measured by the CBOE VIX since April 3rd. This is still high compared to the long-term average of 19, but it is dropping. In addition, the Fear & Greed Index is no longer in extreme fear. Many stocks have bounced back from their 52-week lows but are still trading quite a bit below their 52-week highs. NorthWestern is no exception to this trend. Arguably, the stock is not as good a deal as it was couple of weeks ago. But this is a conservatively run regulated utility. It has a monopoly in its territory and decent rate of return. The utility has managed to grow its rate base, revenue, earnings, and dividend over the past decade. The stock price cratered to the low $50s and the yield was over 4% in response to COVID-19 and the oil price wars. It is still slightly undervalued despite a recent bounceback. In addition, NorthWestern’s dividend yield is ~3.7% and the dividend has been raised for 14 consecutive years. I think that the utility will become a Dividend Champion in time. Granted, 2020 will be tough, but the conservative balance sheet should let the company weather the storm. I was adding to my position a couple of weeks ago, and I view the stock as a long-term Buy.

If you would like notifications as to when my new articles are published, please click the orange button at the top of the page to “Follow” me.

Disclosure: I am/we are long NWE. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment