Bet_Noire/iStock via Getty Images

Northwest Natural Holding Company (NYSE:NWN) is a regulated natural gas utility that operates primarily in the Pacific Northwest. Utility companies like this have long been among the favored holdings of conservative investors, such as most retirees, due to their financial stability and high dividend yields. Northwest Natural Holdings certainly satisfies the high yield requirement, as the company boasts a 3.99% yield at the current price.

Unfortunately, the fact that Northwest Natural Holding Company is a natural gas utility has hurt it somewhat, as the market seems to have expressed a marked preference for electric utilities today. However, as I pointed out in my last article on Northwest Natural Holdings, the market is making a mistake here, as the future of natural gas utilities is in no jeopardy from electrification. This fact has positioned Northwest Natural Holdings to be a very sustainable business to hold for the foreseeable future. Unfortunately, the stock looks a bit expensive at the current price, although Northwest Natural Holding Company does have a few advantages over its peers.

About Northwest Natural Holdings

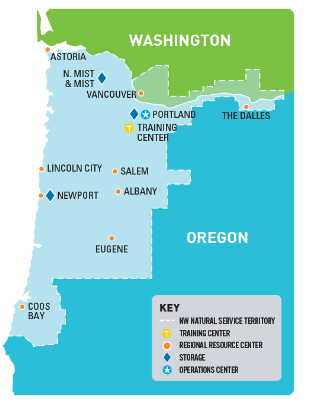

As stated in the introduction, Northwest Natural Holdings is a regulated natural gas utility that primarily serves customers in the Pacific Northwest states of Washington and Oregon:

Northwest Natural Holdings

Although parts of this territory are rural, we can clearly see above that the company’s service area includes a number of major cities. As a result, it serves a surprisingly large 2.5 million customers. That customer count is sufficient to make Northwest Natural Holdings one of the largest utilities in the United States. However, there are few differences between a large and a small utility in terms of their defining characteristics. Perhaps the most important quality is that these companies tend to enjoy remarkably stable cash flows. We can certainly see that stability by looking at Northwest Natural Holdings’ operating cash flows during each of the past eleven trailing twelve-month periods. Here they are:

Seeking Alpha

It is important to look at the Northwest Natural Holding Company’s trailing twelve-month periods as opposed to each quarter in isolation. This is because the company’s quarterly numbers tend to vary quite a bit. This is because the primary use of natural gas is in space heating, which results in a great deal of seasonal consumption variance. After all, it is not really necessary to heat a home or business during the summer months but it becomes much more important during the winter. As such, the company’s fourth and especially first-quarter numbers tend to be much stronger than its second or third-quarter figures every year. When we look at the trailing twelve-month figures, we eliminate much of this seasonal variation. As we can clearly see above, when we look at the company’s cash flows over time with the seasonality effects smoothed out, they are quite stable.

The reason for this stability is that most people consider the provision of natural gas to their homes and businesses to be a necessity. This is, in fact, supported by government policies as most governments provide money to low-income households to help them pay their heating bills and typically pass laws forbidding utilities to turn off the natural gas to a home during the winter. As a result of this necessary nature, most people will prioritize paying their natural gas bills ahead of making discretionary expenses during times when money gets tight. This is especially important during recessions, since low-income people tend to suffer the most during such events. There are a growing number of signs that the United States may soon enter a recession, so it is increasingly important to have your money invested in companies that will not be significantly harmed by such an event. Northwest Natural Holdings is one such company due to its general stability over time, as we can clearly see above.

Naturally, as investors, we are interested in far more than just stability. After all, right now money market funds are yielding 4% so it is pretty easy to match Northwest Natural’s dividend yield by putting your money in a far safer asset. We need a greater reward for taking on the additional risk of stock price changes, and that reward comes in the form of the company’s growth.

Northwest Natural Holding Company is in fact quite likely to deliver this growth. One of the ways that the company is going to accomplish this is by growing its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the price that it charges its customers in order to earn this allowed rate of return. The way that a company grows its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure.

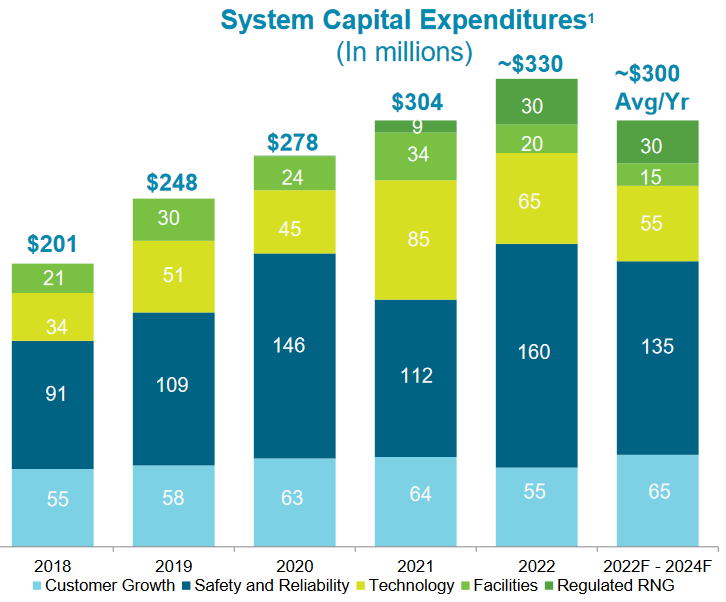

Northwest Natural Holding is doing exactly this, as the company plans to invest approximately $300 million annually over the 2022 to 2024 period. This is a slight decrease over the $330 million that the company actually spent in 2022 but it is higher than the company’s historical capital investments:

Northwest Natural Holdings

The fact that Northwest Natural Holding Company expects its investments to average $300 million per year over the 2022 to 2024 period is a sign that it will decrease its spending in 2023 and 2024 relative to 2022 levels. This is a bit disappointing, but as long as it grows the rate base, it is acceptable. I will admit that I would like to see a lot more visibility into the company’s planned capital spending than management has provided. The majority of the company’s peers have now provided guidance extending out to 2026 or 2027, yet Northwest Natural Holding has failed to provide such guidance.

Hopefully, the company will rectify this problem when it announces its earnings in a few weeks, but either way, it would appear to show less shareholder-friendliness than other utilities. The figures that the company has provided should grow its rate base at a 5% to 7% compound annual growth rate over the 2022 to 2024 period. Northwest Natural Holding Company has stated that it expects to continue that growth rate until 2026 so we can assume that the company’s capital spending during 2025 and 2026 will be at a level that is needed to do that.

Northwest Natural Holding has one advantage to its growth that many other utilities do not have. This is by virtue of the area in which it serves. For many years now, people have been migrating out of California in favor of Oregon. There are a variety of reasons for this, but those reasons are not relevant. The important thing is that the population of Oregon is increasing. This is beneficial for Northwest Natural Holding Company because utilities are largely confined to a single geographic area and as such, they are dependent on the demographic trends in that area. Thus, the fact that the population of Oregon is growing means that there are more customers available for the company within its service area.

Northwest Natural Holding Company is currently growing its customer base at a 1.5% rate annually, which is quite respectable for a utility. This means that the company has many more people every year paying their bills and thus contributing to the company’s revenue.

When we combine the company’s rate base growth with its customer growth, we see that Northwest Natural Holding should be able to grow its earnings per share at a 4% to 6% rate over the next few years. When we combine this with the company’s 3.99% dividend yield, investors should be able to expect an 8% to 10% total return annually on average from the company. That is certainly a reasonable return for a safe utility stock and it should be sufficient to compensate us for the higher risk of purchasing the company’s stock compared to simply putting our money in a money market fund.

As I stated earlier in this article, the market has lately given more favorable treatment to electric utilities than natural gas ones. This is partly due to the environmental, social, and governance trend that has dominated some of the major Wall Street asset management companies. The perception is generally that electricity is much more environmentally friendly while natural gas is going the way of the dinosaur.

However, there are things that natural gas utilities like Northwest Natural Holding Company can do to improve their environmental credentials. One of these things is the use of renewable natural gas. Renewable natural gas is produced naturally when organic compounds decay. The gas is then upgraded so that it matches the consistency of fossil natural gas. It can be used by ordinary natural gas appliances such that nobody would really know the difference. As decaying organic matter can be found pretty much anywhere, there is no need to drill into the ground or frack shale to obtain it. Northwest Natural Holding Company has committed to the use of this compound in its network. In fact, by 2045, the company expects that at least 30% of the natural gas that it delivers throughout the state of Oregon will be derived from renewable sources:

Northwest Natural Holdings

This is a part of the company’s plan to achieve net-zero carbon emissions by 2050. In this case, Northwest Natural Holding has committed to achieving this goal both in its own network and by its customers. Thus, the company is taking some steps in order to ensure that it is fully offsetting the carbon emissions that come from the company’s customers burning the natural gas that they receive from the company.

Admittedly, it does not seem likely that Northwest Natural Holding Company will be able to benefit from interest from the various environmental, social, and governance funds that have taken in enormous amounts of money over the past few years. In a recent article, I discussed how valuable obtaining this interest could be for investors. As a result, we may continue to see the company’s stock price continue to struggle against electric utilities. However, as we have discussed over the past several paragraphs, Northwest Natural Holdings should be able to deliver a somewhat comparable total average annual return by virtue of its much higher dividend yield. As such, there may still be some reasons to hold it despite the fact that it is unlikely to ever be perceived as “green.”

Financial Considerations

It is always important to investigate the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. Thus, a company’s interest expenses may increase following the rollover depending on the conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flows to decline may push it into financial distress if it has too much debt. Although utilities like Northwest Natural Holding Company tend to have remarkably stable cash flows over time, bankruptcies have occurred in the sector so we should still be cognizant of this risk.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company’s equity can cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, Northwest Natural Holding Company had a net debt of $1.4499 billion compared to $1.1209 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.30 today. Here is how that compares to some of the company’s peers:

|

Company |

Net Debt-to-Equity Ratio |

|

Northwest Natural Holdings |

1.30 |

|

New Jersey Resources (NJR) |

1.72 |

|

NiSource, Inc. (NI) |

1.44 |

|

Atmos Energy (ATO) |

0.88 |

|

Southwest Gas Holdings (SWX) |

1.73 |

As we can clearly see here, Northwest Natural Holding Company appears quite reasonably levered relative to its peers. This is a good sign as it indicates that the company is probably not using too much leverage to finance its operations. As such, the company’s debt probably does not present a particularly outsized risk to investors.

Dividend Analysis

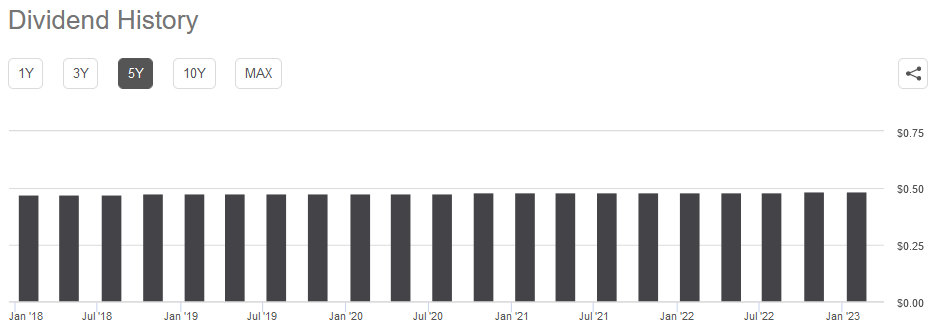

One of the primary reasons why investors purchase shares of utility stocks is because of the high yields that they typically pay out. Northwest Natural Holdings is certainly not an exception to this as the company’s 3.99% yield is quite a bit higher than the 1.61% yield of the S&P 500 Index (SPY). It is also substantially higher than the 2.42% yield of the U.S. Utilities Index (IDU). This latter point may partly be due to the market not particularly liking natural gas utilities. Northwest Natural Holding Company also has a 66-year streak of annual dividend growth, although the growth has been hardly noticeable in recent years:

Seeking Alpha

The fact that the company does consistently grow its dividend is fairly nice during inflationary times, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can obtain with the dividend that the company pays us. This can be a problem for retirees and others that are dependent on their portfolios to generate the income that they need to pay their bills or cover other expenses. The fact that the company increases the amount that it pays us each year helps to offset this effect and maintains the purchasing power of the dividend. With that said, Northwest Natural Holding Company’s recent dividend increases have been nowhere close to enough to keep up with inflation so holders of the stock still lost purchasing power in 2022 but it is still better for the company to boost its dividend than to simply hold it steady.

Naturally, though, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut since such an event would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a company’s ability to pay its dividend is by looking at its free cash flow. The free cash flow is the money that is generated by a company’s ordinary operations that are left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the money that can be used to do things that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on September 30, 2022, Northwest Natural Holding Company reported a negative levered free cash flow of $186.2 million. This is obviously not nearly enough to cover any dividend yet the company still paid out $60.5 million in dividends during the period. At first glance, this could certainly be concerning as it appears that the company cannot actually afford its dividend.

However, it is not uncommon for utilities to cover their capital expenditures through the issuance of debt and equity. These companies will then pay their dividends out of operating cash flow. This is because of the enormous expenses involved in constructing and maintaining utility-grade infrastructure over a wide geographic area. If utilities were to pay everything out of their free cash flow, then they would never be able to sustain themselves as they almost always have negative numbers.

During the twelve-month period ending September 30, 2022, Northwest Natural Holding Company had an operating cash flow of $144.6 million. That was more than enough to cover the $60.5 million that was paid in dividends with a great deal of money left over for other purposes. Thus, the company’s dividend does appear to be reasonably sustainable and investors should not really have to worry about a cut.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility like Northwest Natural Holding Company, one metric that we can use to value it is the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to the company’s forward earnings per share growth and vice versa. However, there are scant few companies that have such a low ratio in today’s richly-valued market. That is particularly true in the low-growth utility sector. As such, it makes sense to compare the company’s valuation to that of its peers in order to determine which stock offers the most attractive relative valuation.

According to Zacks Investment Research, Northwest Natural Holding Company will grow its earnings per share at a 4.30% growth rate over the next three to five years. That is in the 4% to 6% range that we calculated earlier so the figure is probably pretty solid. Assuming this growth rate, the stock has a price-to-earnings growth ratio of 4.16 at the current price. Here is how that compares to some of the company’s peers:

|

Company |

PEG Ratio |

|

Northwest Natural Holdings |

4.16 |

|

New Jersey Resources |

3.33 |

|

NiSource, Inc. |

2.56 |

|

Atmos Energy |

2.49 |

|

Southwest Gas Holdings |

3.20 |

As we can see here, Northwest Natural Holding Company looks a bit expensive relative to its peers. This has been the case for a while though as I have pointed out in my previous articles on the company. Thus, it may not make sense to wait for the stock to decline relative to its peers as it seems pretty unlikely that this will happen. Northwest Natural Holding Company is still positioned to give a reasonably attractive total return though as its dividend yield is quite a bit higher than most of its peers and the company is growing at a decent rate. It may be best right now to pick it up anytime the stock declines.

Conclusion

In conclusion, Northwest Natural Holding Company is a regulated natural gas utility in the Pacific Northwest that offers some real opportunities for investors. Admittedly, Northwest Natural Holding Company is likely not going to be as popular as an electric utility across the market, but natural gas as a fuel is not going away anytime soon. Northwest Natural Holding Company is poised to deliver a respectable total return to its investors and boasts a reasonably strong balance sheet. The only real downside here is that Northwest Natural Holding Company is a bit expensive at the current price.

Be the first to comment