Grassetto

Northern Technologies International (NASDAQ:NTIC) is a global leader in plastic anti corrosion solutions. Its products are used to prevent piece corrosion, particularly in auto manufacturing. The company is also making advances in O&G anti corrosion solutions, and commercializes its own varieties of bioplastics.

In an article from February 2022 I issued a hold rating on NTIC, on the basis that the company was valued at a multiple that was not justified by its growth prospects. Since then, the multiple has expanded, because the company has generated fewer profits, while the stock price has remained stable.

In this review, I maintain my hold rating, although I also point to some one-time factors that reduced NTIC’s earnings in FY22, plus some interesting avenues for growth. Overall, although the company has a promising future, I believe the multiple is unjustifiably high.

Note: Unless otherwise stated, all information has been obtained from NTIC’s filings with the SEC.

Business description

Leading in VCI anti corrosion products: NTIC specializes in a type of anti corrosion solution called volatile corrosion inhibiting chemicals. The products (plastic bags, emitters, gels, etc.) release chemicals that cover the protected pieces and prevent corrosion. This is different from more traditional cathodic protection where a chemical bait is set to absorb most of the corrosion.

The magic of NTIC’s products is that the protection is the container bag itself, or a small piece of rubber inside a box. Cathodic protection requires a metal piece attached to whatever is being protected. NTIC’s products are therefore heavily used in the automotive industry where small pieces have to be protected.

Although NTIC does not enjoy patents on these products anymore, the company claims a 25% global market share on VCI products ($150 million in consolidated and JV sales over a $600 million market, according to the company’s investor presentation).

Expanding to O&G: The company has reached a limit in the traditional piece protection segment. The market is not growing faster than automotive is, and NTIC already has a substantial share of it. It has been trying for years to move into equipment protection, particularly in O&G.

In this segment it competes with more traditional cathodic protection, offering solutions that require less downtime or lower CAPEX investments (for example to unearth a pipe segment or empty an oil tank). Still, its solutions are the entrants, and the O&G industry has been slow to adopt them.

According to the company, the industry has long sales windows, and equipment owners are conservative. Recent revenue increases and agreements provide some hope in this area.

Bioplastics: NTIC purchases resins from the largest bioplastic producers (NatureWorks, BASF, Total-Corbion) and combines them into process specific plastics, such as extrusion, injection, etc. The company also sells finished products (cutlery, bags). It does not hold a particular moat in this segment.

Subsidiary and JV model: NTIC is a global company, and 60% of its sales are done by unconsolidated JVs. The company generates regular income from consolidated subsidiaries (Germany, China, India, Mexico and Brazil), and royalties plus equity income from JVs (all other European countries, ASEAN). The JVs are managed by local partners.

No manufacturing model: NTIC does not own manufacturing facilities. It contracts from independent manufacturers, or leaves manufacturing to its JVs.

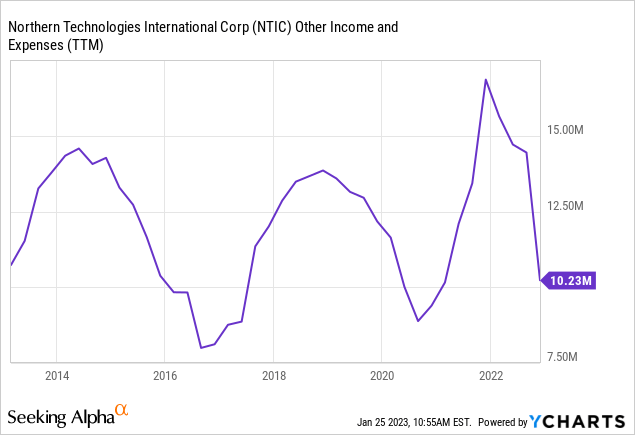

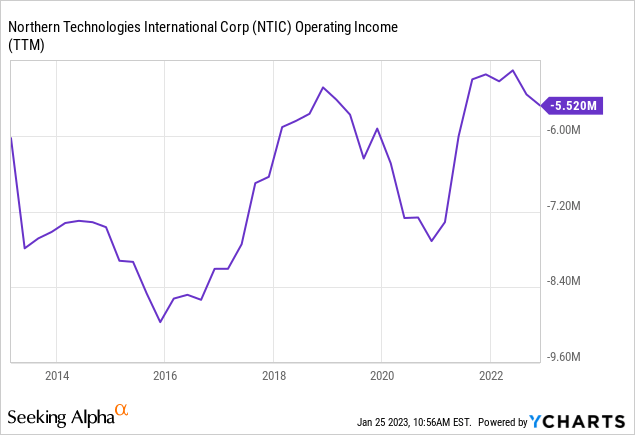

Cyclical exposure: As can be seen from the chart above of income from JVs, plus the chart below of operating income, NTIC suffers from cyclical exposure to industrials.

Low debt: NTIC holds only $5.5 million in a line of credit paying prime + 2.5%, a small debt level for a company generating around $5 million in net income. NTIC also has $6 million in cash reserves, although not all of it can be distributed as it is used by subsidiaries.

High insider and managerial ownership: Insiders own 24% of the company, and most officers have been in the company since the early 2000s or earlier, according to the company’s proxy statements.

Recent developments

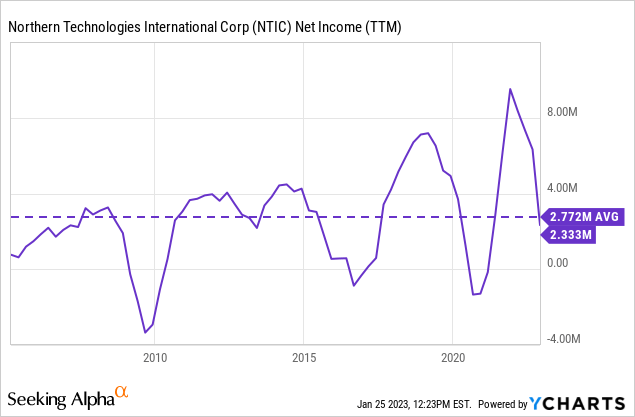

One year ago, I warned against what I considered unsustainably high earnings from NTIC. The non recurring portion was generated by a $4 million accounting gain from the acquisition of 50% of its India subsidiary.

This year, I warn the opposite. Current earnings are lowered by foreign exchange movements (dollar appreciation) that affected global operations.

India moves up the income statement: Most growth in revenue from the traditional corrosion segment was generated by the consolidation of the JV in India after 50% of it was acquired (now it is wholly owned). Conversely, income from JVs fell significantly for the same reason.

JVs are affected by FX: Unconsolidated JV sales fell 14% in FY22, but this actually means that on average, real sales grew. The dollar index (DXY^) rose 22% between September 2021 and September 2022. This means that on average the dollar appreciated 22% against the major world currencies. Because JV sales are accounted for in local currency, this reduces their dollar value.

A similar example comes from its major JV, EXCOR Germany. Equity income from the position in that JV fell 28%, with the euro falling on average 15% during the Sept 21-Sept 22 period.

O&G is taking off: NTIC has been investing in penetrating the O&G industry for years, and that is now starting to pay back.

NTIC announced new contracts for tank protection with British Petroleum. These are renewed contracts with more facilities included than in the previous contract, implying that the company’s products were satisfactory. The company also cites positive technical reviews from the American Petroleum Institute for the use of VCI technology.

All in all, the O&G segment has been growing revenues at a CAGR of 22% since 2017.

Bioplastics are also growing: Although the company does not have a compelling strategy in bioplastics, the segment is growing thanks to global traction for compostable plastics. 2017-2022 sales grew at a CAGR of 20%, including a 50% revenue increase in FY22 alone.

Slow JV acquisition continues: NTIC comments that most of its JVs were set up during the 1980s and 1990s. The company also mentioned that it has to elaborate plans to transition the businesses once its partners retire. With less developed equity markets, the JVs in many of those countries can be acquired for lower multiples. An example was the acquisition of 50% in the India JV in 2021. A new example was the much smaller consolidation of the Taiwan operations last year, because the partner passed away.

Valuation

Despite the company being financially strong, dominant in its core market and growing in other markets, I just cannot accept its current valuation.

The company’s net income has not grown in the past 20 years, and has been very cyclical. The 20 year average is $2.7 million. Adjusting the period to begin in 2010 or 2015 makes a small difference, with the average reaching $3.5 million.

This implies a multiple on earnings between 35x and 45x, for a business that has not grown. Despite the company doing very well last year, and the existence of several growth avenues (bioplastics, O&G and JV consolidation), I believe the required margin is too low.

Particularly, the new segments (O&G and bioplastics) still make only 12% of the global NTIC footprint (when the JVs’ sales are included), and their gross margins are lower than those of the classical piece protection segment.

Conclusion

Although NTIC has growing segments, a dominant position in a profitable market, and a strong balance sheet, I believe the multiples to historical earning averages at which it trades are excessive. Today, even the fastest growing, most profitable companies are trading below these multiples.

NTIC’s growing segments still represent a small proportion of revenues, and therefore could not carry an income statement that is tied to a profitable core market that is not growing.

Like in many other occasions, the problem is not the company, but price.

Be the first to comment