Love Employee

This article first appeared in ‘Trend Investing marketplace’ on January 12, 2023; but has been updated for this article.

Today’s article will focus on Northern Graphite’s current mining operation in Canada (Lac des Iles), the potential for Northern Graphite to become a significant North American battery anode material (“BAM”) producer, and valuation of the company.

For a background on Northern Graphite you can read our past articles:

- Feb. 2022 – Northern Graphite Is Set To Become The Only North American Graphite Producer

- May 2022 – Northern Graphite CEO Greg Bowes Talks With Trend Investing

Northern Graphite [TSXV:NGC](OTCQB:NGPHF) – Price = CAD 0.56, USD 0.42

Northern Graphite 5 year price chart (source)

Yahoo Finance

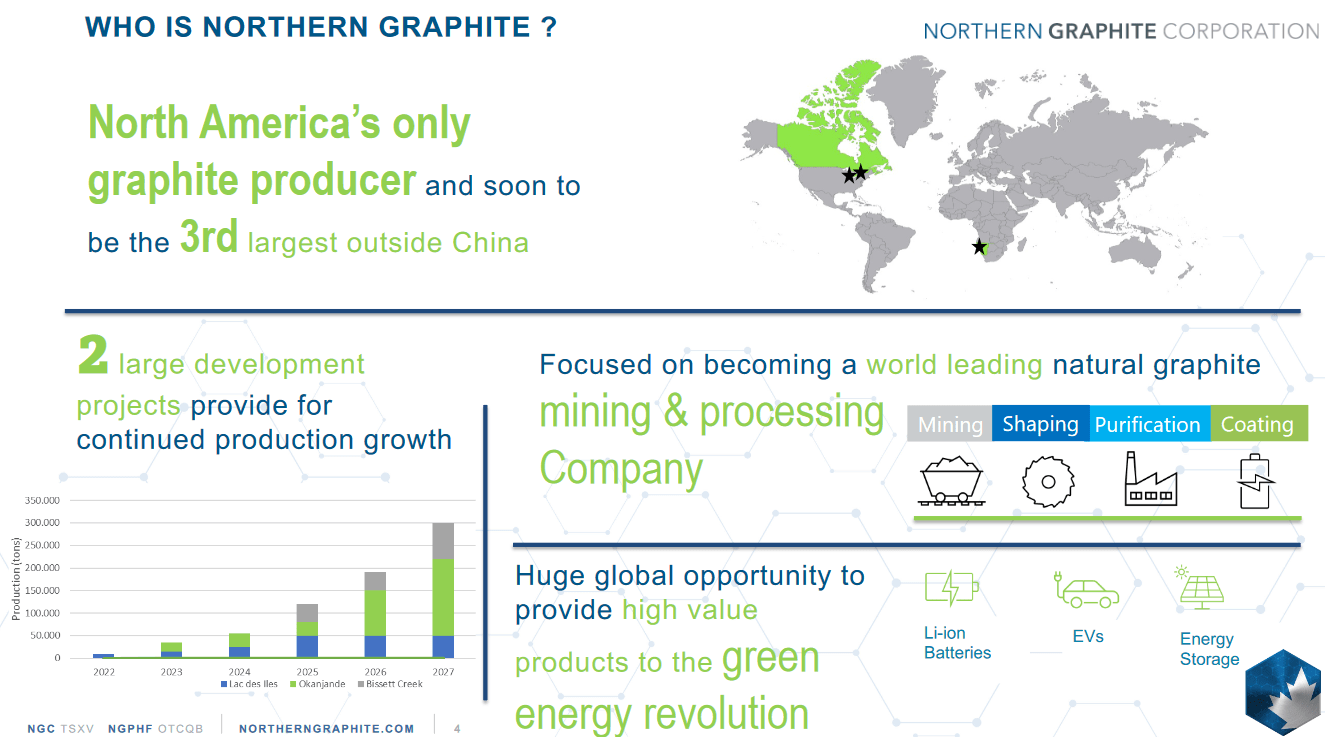

Northern Graphite (“Northern”) is a Canadian graphite producer with two Canadian graphite projects (one is an operating mine), Namibia graphite operations (set to restart mid 2023), and now what appears to be solid plans to move into the value-added space for battery anode materials (“BAM”).

Northern Graphite states:

Northern is the only significant graphite producing company in North America and will become the third largest outside of China when its Namibian operations come back online.

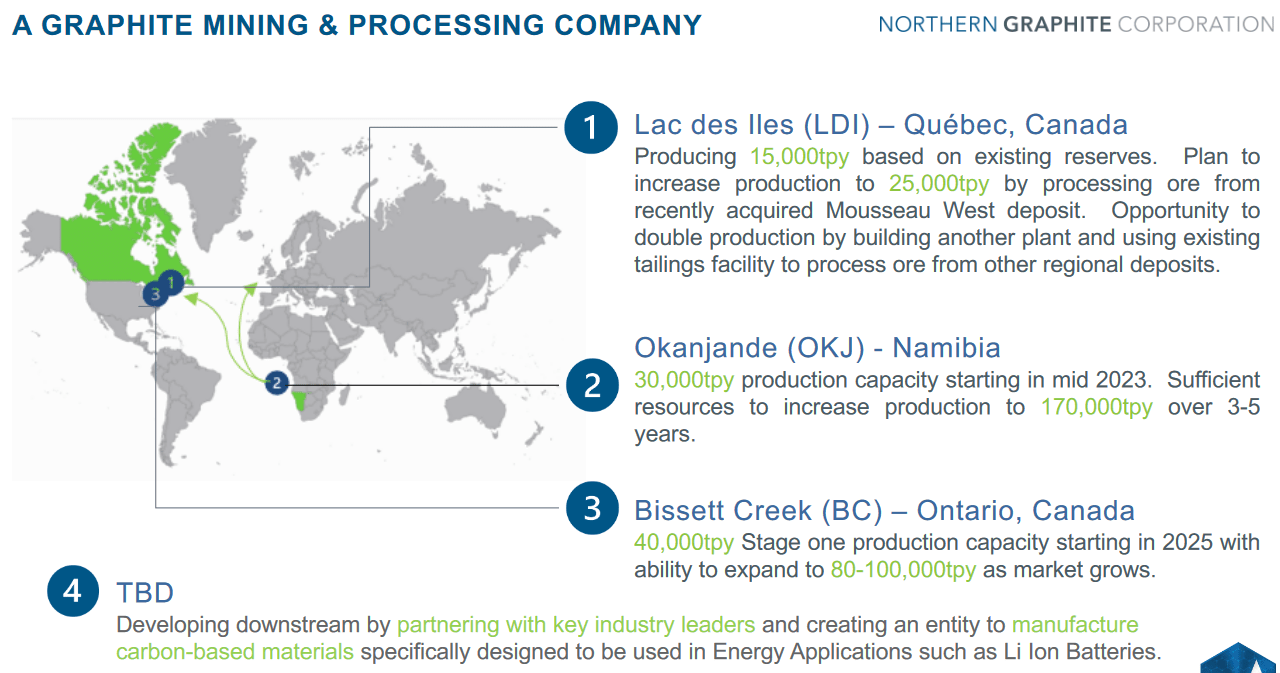

Northern Graphite’s operations/projects include:

- Lac des Iles (“LDI”) graphite mine (25,000 tpa flake graphite production capacity) and Mousseau West Graphite deposit in Quebec, Canada.

- Bissett Creek Graphite Project in Ontario, Canada. Advanced development stage with plans to become a 40,000 tpa producer by ~2025, then later expanding to 80-100,000 tpa of flake graphite production.

- Okanjande graphite deposit/Okorusu processing plant in Namibia. On standby with a capital cost of US$15.1m to restart operations. Plans to restart operations in mid 2023. Plans to build a large, new processing facility at the Okanjande mine which will be capable of producing up to 170,000 tpa of flake graphite.

- South Okak Ni/Cu/Co Project located 80 km north of Voisey’s Bay, Labrador, Canada.

A summary of Northern Graphite’s operations and projects (source)

Company presentation Company presentation

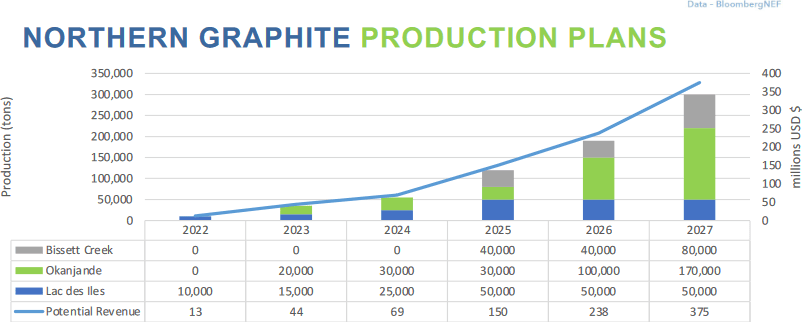

Northern Graphite’s flake graphite production growth plan to reach 300,000 tpa in 2027 (source)

Company presentation

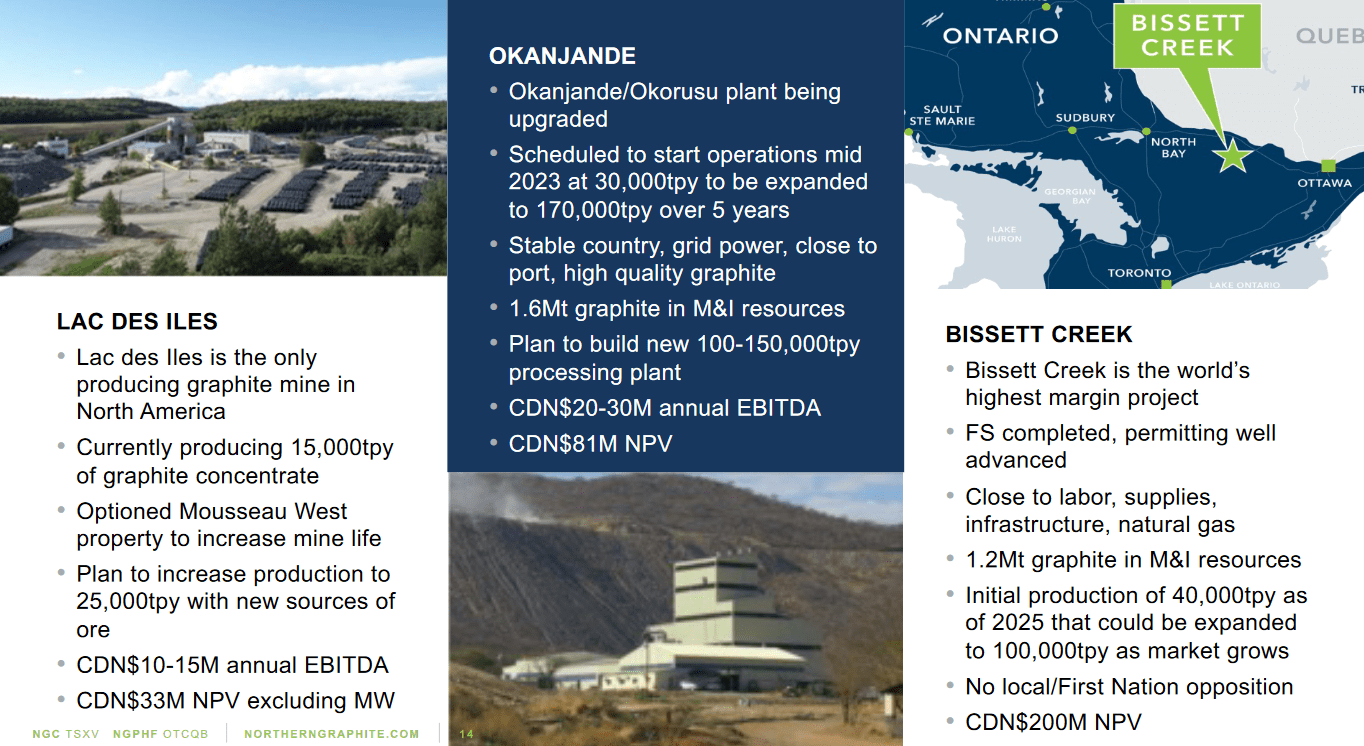

Lac des Iles (“LDI”) graphite mine and Mousseau West Graphite deposit

Northern Graphite summarize well by stating:

The Lac des Iles graphite mine in Quebec [LDI] is the only significant graphite producer in North America. The LDI mine has been in operation for over 20 years and will produce up to 15,000 tpy of graphite concentrate over the next two to three years of remaining reserves. Northern plans to expand production and extend the mine life by securing sources of ore from other locations. Northern acquired 100% interest in the Mousseau West Graphite deposit on October 5, 2022. This property is located approximately 80 kms, and in economic trucking distance, from Lac-des-Iles graphite mine in Quebec.

Regarding the next stage with the 100% owned Mousseau West Project feeding LDI Northern Graphite state:

Resources at LDI will be depleted in the next couple years and Mousseau West has the potential to significantly extend its life and return production to 25,000tpy, thus maintaining the jobs and economic benefits generated in the Antoine-Labelle Regional Municipality. There will be no processing plant or tailings pond at Mousseau West, only a quarry…….(Mousseau West) contains an Inferred Resource of 4.1 million tonnes grading 6.2% graphitic carbon…….The Company intends to update the resource estimate and complete a Preliminary Economic Assessment to evaluate the economics of mining graphite at Mousseau West and trucking it to Lac-des-Iles for processing.

Comment

It should also be noted that the Lac des Iles graphite mine is currently struggling to make significant profits due to low flake graphite prices and relatively high operating costs compared to larger peers in other countries such as Mozambique and China. It should also be noted in Q3 they produced more than they sold, so results should improve in Q4 if they sell all their production. Had they sold all 3,068t at US$1,572 (with cash costs at US$1,177) they would have made a gross profit of US$1.21m for the quarter, which is a lot better than the C$0.8m loss reported.

As quoted from Northern Graphite’s Q3, 2022 results:

- “Income from mine operations of $0.8 million.

- An operating loss of $0.9 million was recorded which includes general & administrative expenses, project evaluation, acquisition and integration costs and a foreign exchange gain.”

Northern Graphite Q3, 2022 financial results (source)

The key for flake graphite producers is to achieve economies of scale and/or become vertically integrated to become battery anode materials producers. This value add leads to higher selling prices of active spherical graphite and potentially better profit margins.

Northern Graphite’s battery anode material plans

As announced on January 10, 2023 Northern Graphite entered an agreement to select a site for construction for North America’s largest battery anode material plant. The agreement is with Innovation et Development Manicouagan (“IDM”). The announcement states:

Pursuant to the agreement, Northern has a 12-month period to evaluate several sites around Baie-Comeau to determine their technical and economic suitability for the proposed BAM plant. The sites range between 200,000 and 450,000m2 in size and have direct rail and port access as well as green hydroelectric power that would result in one of the lowest CO2 footprints in the industry……Baie-Comeau is located 400km from Quebec City in the Cote-Nord economic region and has direct rail and road access to the rest of North America as well as a deep water, all season port. It is eligible for Plan Nord incentives and other assistance is potentially available under programs offered by the Manicouagan region, the province of Quebec and the Canadian and US Governments. Construction of the proposed battery plant would be subject to identification and acquisition of an appropriate site, receipt of regulatory approvals and financing…..

Note: Innovation et Development Manicouagan is a non-profit organization leading different initiatives to mobilize economic development stakeholders in the RCMs of Manicouagan. The organization works in close collaboration with decision-makers at different levels of government, regional organizations, major prime contractors and SMEs to foster the emergence of projects that could strengthen innovation and growth in the community.

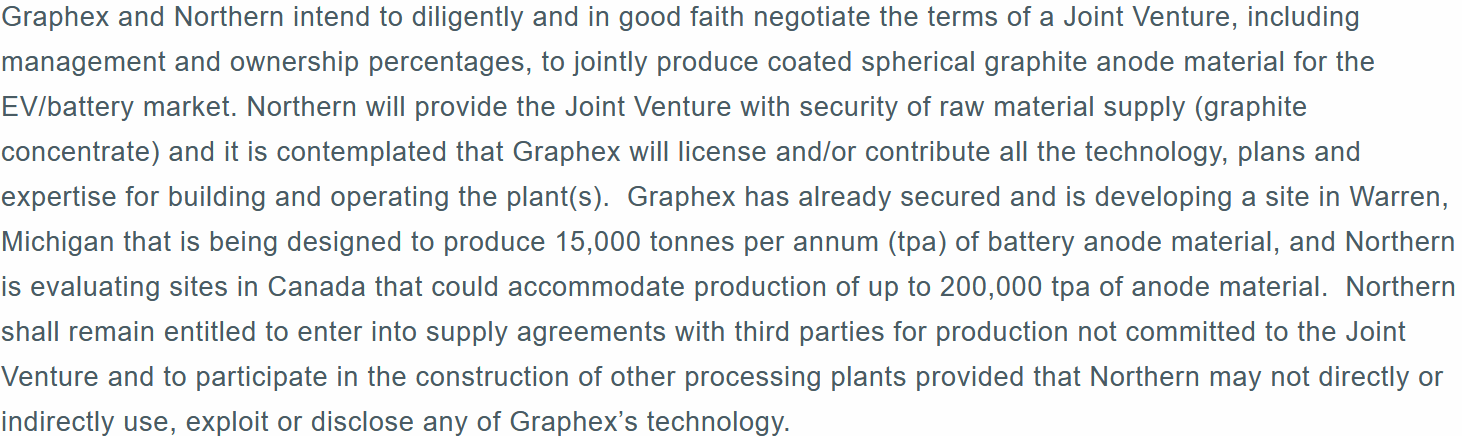

Given the announcement just a few weeks earlier on December 21, 2022 that Northern Graphite has a LOI with Graphex Technologies to produce natural graphite anode material, it would seem possible that a JV between the two companies may be formed to build the battery anode materials plant at Baie-Comeau.

Some details on a possible JV between Graphex and Northern Graphite (source)

Map showing the proposed location of the BAM plant in Baie-Comeau in Quebec, Canada (source)

Northern Graphite announcement January 10, 2023

Comment

Perhaps the most interesting aspect of the plan is the sheer size. A 200,000 tpa BAM plant is huge and would make it by far the largest in North America.

By comparison Syrah Resources Vidalia BAM facility being built now in Louisiana is planned to reach an initial 45,000 tpa, with Tesla (TSLA) already signing an off-take agreement for 25,000 tpa (8,000 tpa + 15,000 tpa). Syrah was also recently awarded a grant of up to US$220m from the US Department of Energy (“DOE”) to help fund their Vidalia expansion to 45,000 tpa and has also applied for a loan with the DOE’s Advanced Technology Vehicles Manufacturing (“ATVM”) loan program.

Northern Graphite does have 3 graphite projects potentially capable of providing the needed flake graphite feed for the BAM plant. The question is how will they fund a 200,000 tpa BAM plant. Will Canada follow the USA’s generous lead, or will the USA fund the project with a loan?

Battery anode material sells for US$6,000+/t, compared to flake graphite at US$500-2,500/t (source)

Company presentation

Valuation

Northern Graphite trades on a market cap of C$68m.

Northern Graphite state in their Q3, 2022 financials announcement:

As at September 30, 2022 the Company held $4.7 million in cash and equivalents and held $9.1 million of current restricted cash (out of which $7.6 million was released subsequent to September 30, 2022), working capital of $27.5 million and long-term debt was $15.3 million (senior secured loan). Working capital includes $18.4 million of inventory consisting of 6,648 tonnes of graphite concentrate and approximately 7,000 tonnes of recoverable graphite in the ore stockpiles.

Note: The inventory value above of C$18.4m exceeds their debt of C$15.3m.

We were unable to find an analyst’s price target.

Comparison to peers valuation as of Nov. 2022 (source)

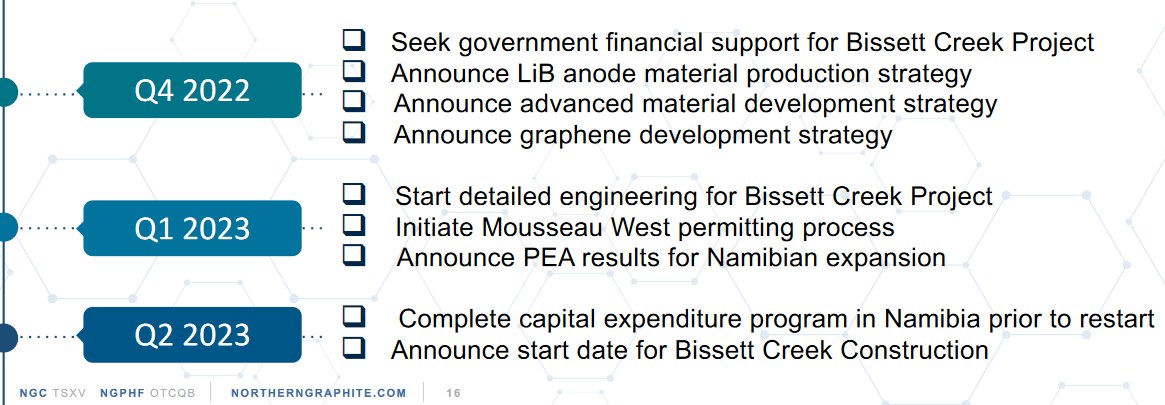

Near term catalysts (source)

Company presentation

Risks

- The EV boom stalls or moves to graphite free anodes. Looks very unlikely for now.

- Graphite prices falling. Surging demand should eventually see graphite prices grind higher. EV anode demand will be the key driver and that requires battery anode material (active spherical coated graphite) which sells at a premium (US$6,000/t +).

- Mining risks – Exploration, funding, permitting, production, project delays. The current graphite production at Lac-des-Iles is struggling to be profitable (high OpEx and low flake graphite prices) and in 2-3 years Northern Graphite will need to switch using Mousseau West as graphite feed. The planned BAM plant will require significant capital to be raised to fund it. A JV may occur, cheap development bank debt, or a government grant or loan would be very helpful.

- Company risks – Management, liquidity, currency risks.

- Sovereign risk – Canada is low risk. Namibia is high risk.

- Stock market risks – Dilution, lack of liquidity (best to buy on local exchange – TSXV), market sentiment.

Further reading

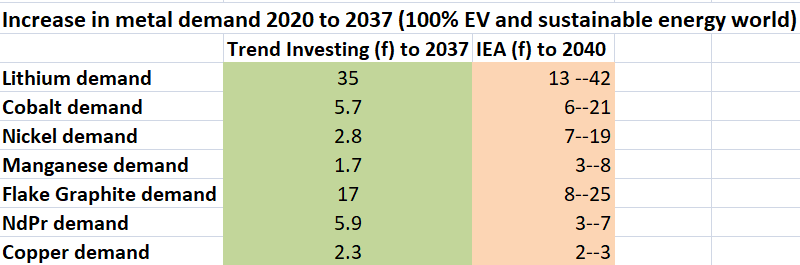

Flake graphite demand set to surge as the EV boom takes off – Trend Investing v IEA demand forecast for EV metals (Trend Investing) (IEA)

Trend Investing & the IEA

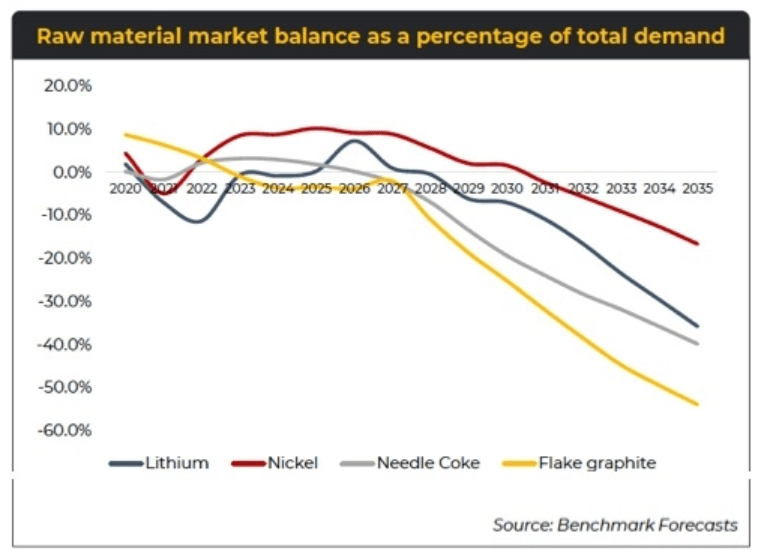

Graphite deficits are coming soon – BMI graphite-market-balance benchmarkweek-2022 (source)

Benchmark Mineral Intelligence

Summary of Northern Graphite (source)

Company presentation

Conclusion

The flake graphite business is not easy. Those companies that are making profits typically have very low operating expenses due to large scale efficient operations typically in cheaper labor countries or regions. Generally low, but improving (China price was up 32.3% in 2021) graphite prices, has been the problem.

Looking ahead graphite demand is set to surge. Analysts are already talking about flake graphite deficits beginning perhaps in 2023 and widening by 2027. The IEA forecasts flake graphite demand to increase by 8x to 25x from 2020 to 2040 and Trend Investing forecasts graphite demand to increase by 17x from 2020 to 2037. These forecasts imply that graphite has the second highest demand profile, only beaten by lithium.

Trend Investing’s view is that the best placed graphite companies will be those such as Syrah Resources and Northern Graphite (potentially if funded) that can achieve low cost flake graphite production and vertical integration to achieve volume production of battery anode materials (active spherical graphite).

Valuation looks appealing on a market cap of only C$68m given the potential growth ahead; however investors should be cautious given the current very weak cash flows from the Lac des Iles graphite mine.

Risks are numerous to execute the company’s graphite expansion and BAM plans. The flake graphite price falling is another key risk. Please read the risks section.

We rate Northern Graphite as a cautious smaller dollar speculative buy. We see strong potential upside if graphite prices improve and if the Company can execute their plans effectively; however we also see plenty of risk.

As usual all comments are welcome.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment