LumerB

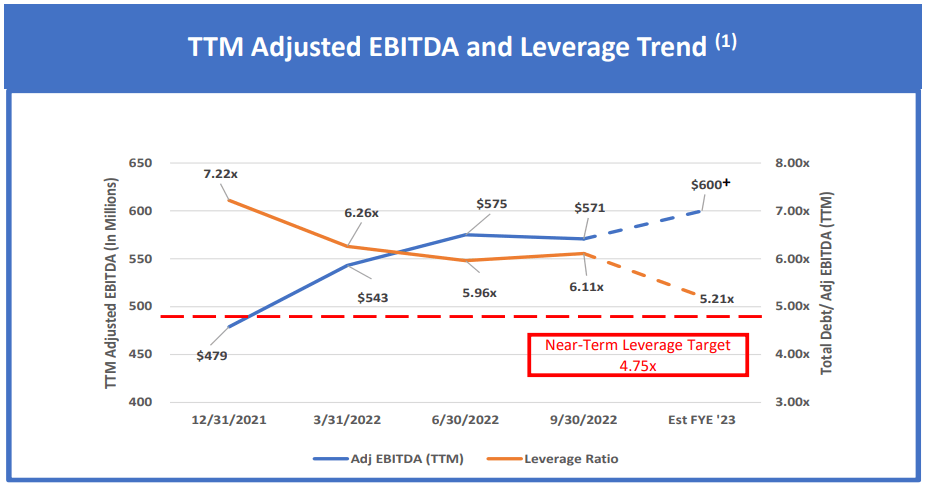

The latest news from NGL Energy Partners LP (NYSE:NGL) came on January 3, when management increased its Adjusted EBITDA guidance from “greater than” $600 million to “greater than” $630 million. Management also reported that NGL had paid down $227 million of debt in the quarter ending December 31, closing out the quarter with a total debt balance of $3.26 billion.

The most important takeaway from the announcement is that NGL probably paid down enough of its November 2023 senior notes to make the remaining balance manageable. Since the January 3 announcement, the bonds have traded up to par, indicating that the market is confident the company will meet its 2023 maturity.

NGL’s higher Adjusted EBITDA guidance and lower debt balance improve its leverage ratio from around 6.0-times to 5.2-times, consistent with management’s stated leverage goal, as shown below.

NGL Energy Partners

While NGL’s leverage remains high, it has undergone a remarkable improvement in a single quarter. Its downtrend has to continue to shore up any value that may reside in the common equity.

Despite the Good News, NGL Equity has Little Value

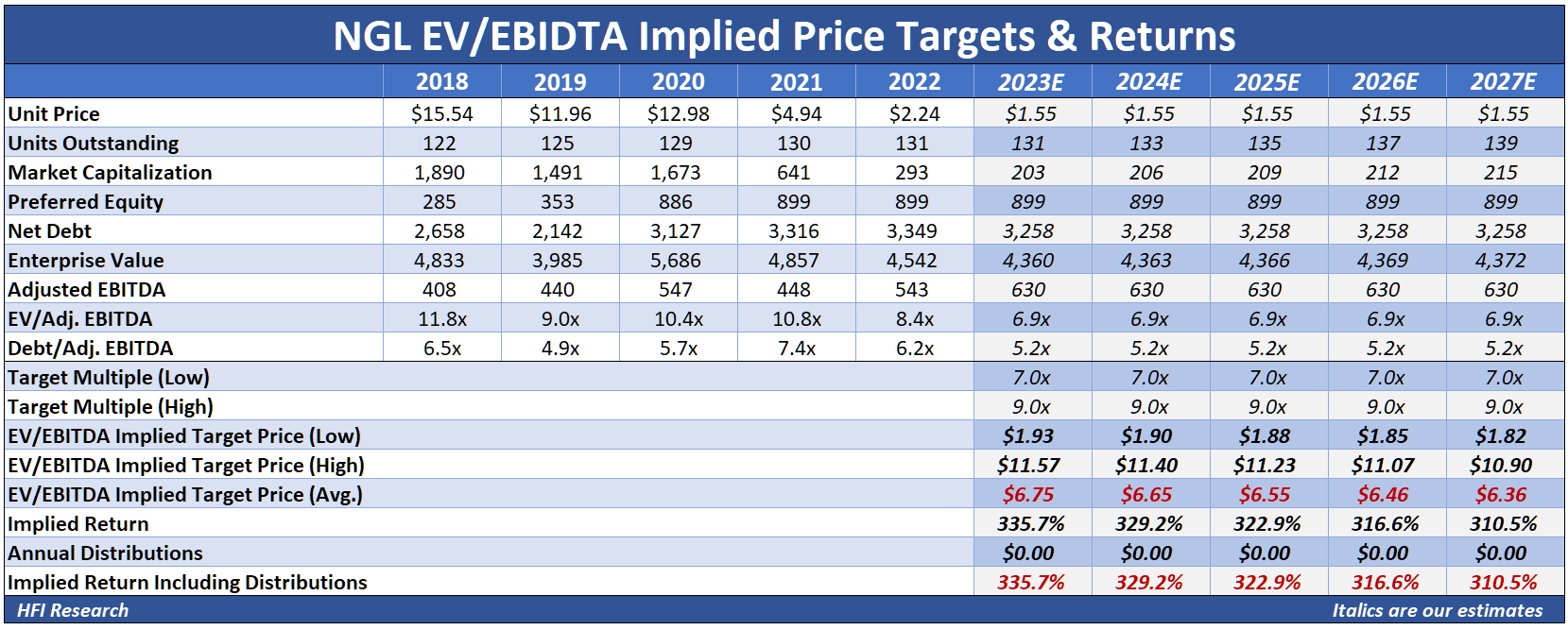

Using an EV/EBITDA valuation for NGL Energy Partners LP units based on management’s guidance paints a deceptively constructive picture of its common equity value. While the company’s net debt-to-Adjusted EBITDA remains at a high of 5.2 times, its Adjusted EBITDA of $630 million implies growth of 16.1% from the previous year and would suggest healthy cash flow generation.

Valuing the units based on EV and EBITDA in isolation implies a total return of more than 300% from the current unit price of $1.55.

HFI Research

Unfortunately, we question whether NGL Energy Partners LP’s Adjusted EBITDA outperformance is sustainable in light of its pitiful free cash flow generation over recent quarters. The past few quarters show the company’s onerous interest expense and large capex requirements consuming nearly all its cash flow.

NGL’s lack of free cash flow through the end of September implies virtually no value in its common equity. Consider that in the year ending September 30, it generated only $21 million of free cash flow.

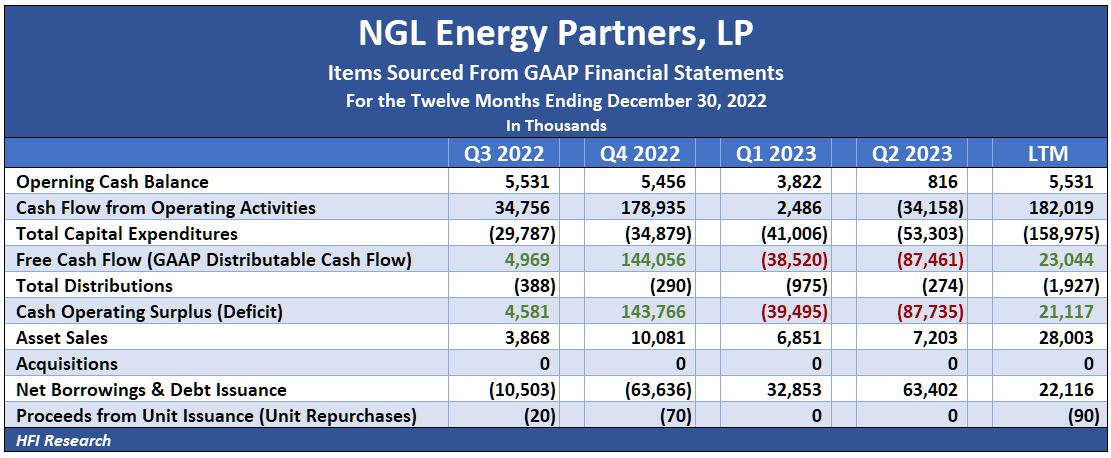

More recent performance has been atrocious. In the six months ending September 30, as shown in the table below, NGL generated a cash flow deficit of $127 million, albeit with a $166 million working capital build. It funded the deficit through $14 million of asset sales and by taking on an additional $96 million of long-term debt.

HFI Research

NGL Energy Partners LP’s credit metrics also point to distress. For the quarter ending September 30, EBIT stood at $72.4 million, while interest expense was $68.3 million, for a razor-thin interest coverage ratio of 1.06-times. Operating cash flow was negative due in part to a working capital build.

We’re curious to see how much free cash flow NGL generated in the quarter ending December 31. Taking management’s Adjusted EBITDA guidance and subtracting interest expense and our estimate of capex puts free cash flow at an average of approximately $60 million for each of the two quarters after September 30. Management’s announcement of $277 million of debt reduction suggests the December 31 quarter saw even greater free cash flow, since NGL had only $177 million of total liquidity on September 30 and was facing heavy seasonal working capital requirements associated with its gas blending business.

Even if NGL Energy Partners LP’s recent performance is exceptional, unless the company improves its cash flow generation on a sustainable basis and can generate at least $200 million of free cash flow annually for the next two years, the company’s common equity is at risk of total loss.

NGL Energy Partners LP’s Debt is the Best Investment Option, But Still Risky

NGL Energy Partners LP’s common equity has no prospect for a reinstated distribution until the company has met the obligations associated with its preferred units and until its leverage is reduced to levels that ensure its senior notes can be refinanced. Until then, its equity will remain at risk if an energy market downturn reduces cash flow. The equity will also remain at risk from higher interest rates on NGL’s credit facility and its Class B and Class C preferred issues. The Class B preferred distribution has already reset from a fixed to a variable interest rate, and the Class C preferred distribution will do so on April 15, 2024.

As for the bonds, the market prices of NGL’s 2025 and 2026 senior notes indicate financial distress. NGL’s 2025 notes have a coupon of 6.125% and trade at 88 cents on the dollar to yield 12.6%. Its 2026 notes have a coupon of 7.5% and trade at 84 cents on the dollar to yield 13.8%, according to FINRA. The high yields on these notes reflect the risk of default. They also point to the high cost of debt to which the company will be subject unless it reduces leverage.

With so little cash flow available for paying down debt and such a high cost of capital, we understand the market’s concerns about NGL’s ability to repay its senior notes.

The low prices and high yield on NGL Energy Partners LP’s senior notes, coupled with the senior claim they have to the company’s assets, make them a better alternative than its common and preferred equity. The common equity is at risk of total loss and the preferred equity is at risk of recovering a fraction of par value in a bankruptcy. But if we were NGL bondholders, we would rather avoid a bankruptcy scenario given the potential for drawn-out proceedings and uncertain recovery prospects. We, therefore, recommend avoiding all of NGL’s securities, from the common equity to the preferreds to the bonds.

Conclusion

NGL Energy Partners LP has to grow Adjusted EBITDA, generate free cash flow, and/or pay down debt in order to avoid bankruptcy in 2025. Until it does, NGL’s common equity will have little value, and the company will effectively be run for the benefit of its debtholders and preferred unitholders, which are the only classes of security holders likely to realize value in a restructuring.

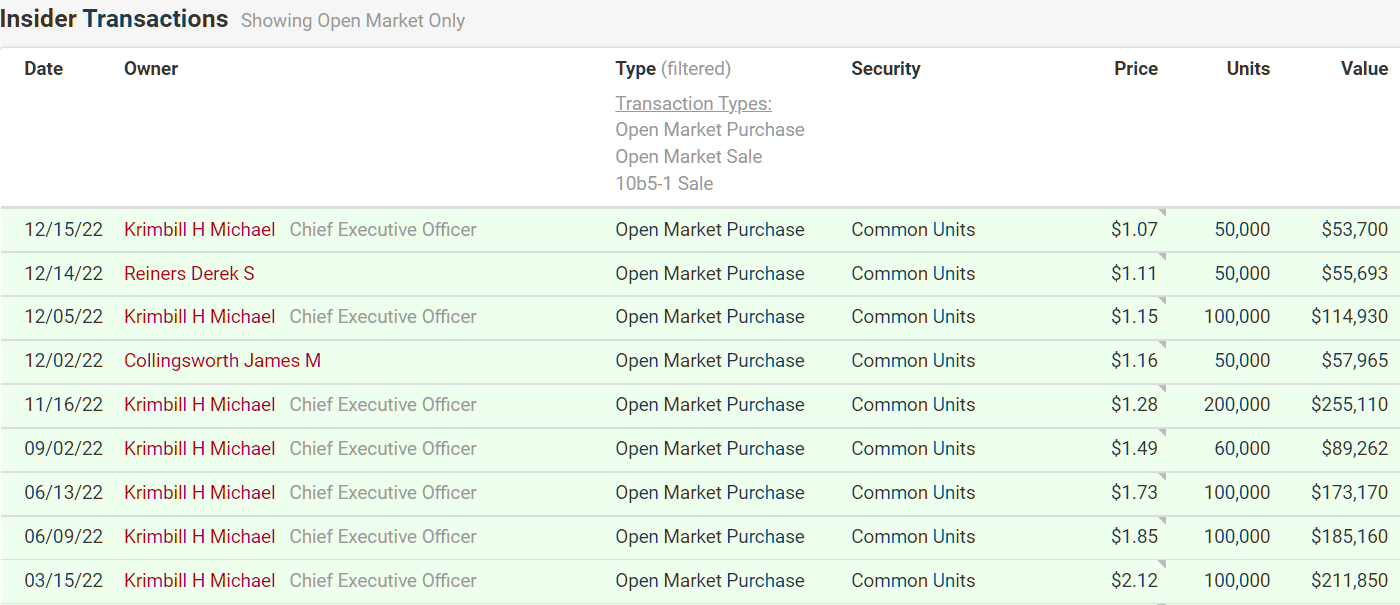

We should note that even though bankruptcy and a complete wipeout of value is a real prospect for common unitholders, management is putting up a fight to avoid that outcome. In fact, it appears optimistic, given the substantial insider common equity purchases made throughout 2022.

BamSEC

We recommend watching the NGL Energy Partners LP play-by-play from the sidelines. The only course we would consider pursuing is to buy equity after a restructuring. And even then, we would like to see new and improved management, as well as a sustainably strong performance from its water assets. For the time being, with NGL Energy Partners LP’s outlook bleak, we rate its units as a Sell with no price target.

Be the first to comment