Cindy Ord/Getty Images Entertainment

While most speculative SPACs were crushed in 2022 and some have rallied big in early 2023, Nextdoor Holdings (NYSE:KIND) has lingered near $2. The social media space has struggled recently due to tough comps and a weakening advertising market. My investment thesis remains ultra Bullish on the local focused company due to the high monetization opportunity and the large cash balance to invest for the future regardless of whether a recession occurs.

Source: FinViz

Don’t Get Distracted By Losses

The stock market has dramatically shifted focus from companies with strong growth to favoring ones with strong cash flows. Nextdoor has been left behind due in part to large ongoing losses.

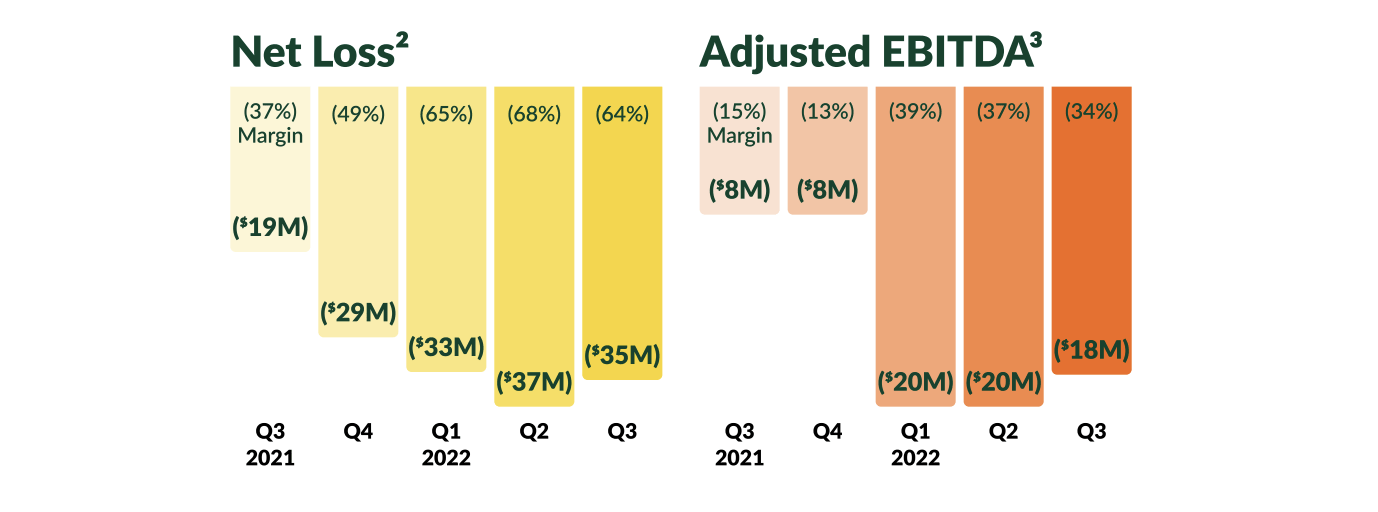

For Q3’22, the local social company reported an adjusted EBITDA loss of $18 million, only down slightly from the $20 million loss in the prior quarter. The adjusted EBITDA margin was an alarming 34% loss only down 3 percentage points from Q2 levels.

Source: Nextdoor Q3’22 shareholder letter

While the losses are very large, Nextdoor has a cash balance of $605 million. Since the local social platform doesn’t face any near-term liquidity issues, investors shouldn’t get stuck on ongoing large losses considering the large margins of larger peers at scale.

The guidance for Q4’22 was an adjusted EBITDA loss of ~$18 million on revenues of only $51 million. With all of the tech giants slashing employees including signs Elon Musk eliminating up to 70% of the jobs at Twitter, Nextdoor might find the ability to grow without aggressive spending. On the flip side, Google (GOOG, GOOGL) announcing a 12,000 job cut could signal the advertising market remains weak, potentially impacting the upcoming guidance from Nextdoor when reporting Q4 results.

Massive Opportunity Ahead

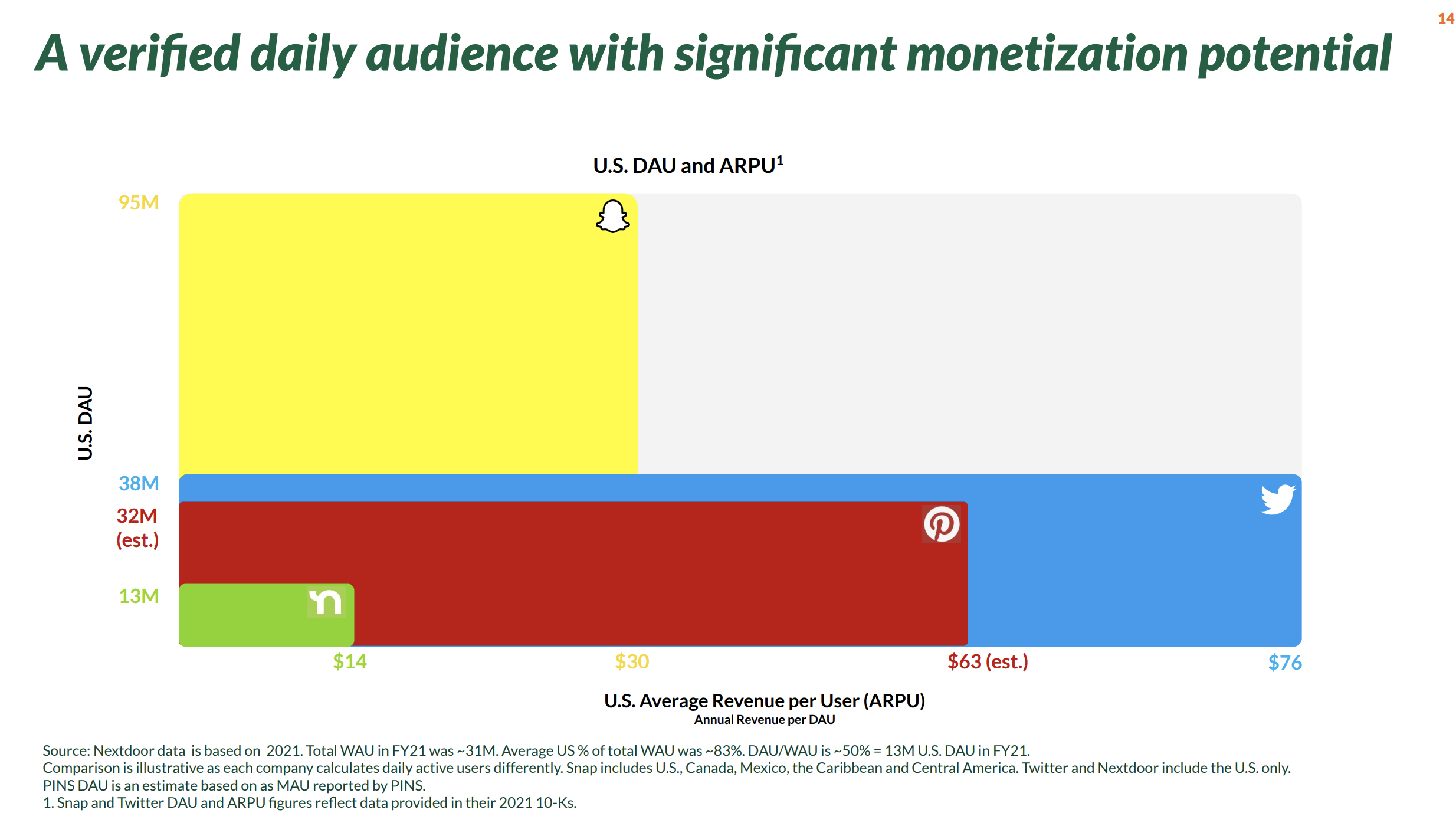

The key to the investment story is the large opportunity still in front of the building social platform. Nextdoor very much under-monetizes other social media firms that don’t come close to matching the numbers from Meta Platforms (META).

Based on data supplied by Nextdoor, the company only generates $14 in revenue per U.S. DAU compared to Twitter and Pinterest (PINS) up at ~$70. In addition, the company has the potential to vastly expand users beyond the estimated 13 million DAUs when these firms average ~35 million domestic users.

Source: Nextdoor Q3’22 shareholder letter

Nextdoor constantly highlights higher users due to the use of weekly average users (WAUs). The company reported 36 million WAUs to end 2021 and grew the number to 38 million in Q3’22.

Of course, these are total user numbers. The U.S. portion is a majority of the users with Nextdoor ending 2021 with only 26 million domestic WAUs. The company had 31 million U.S. WAUs by Q3’22.

Based on these numbers, Nextdoor has about double the WAUs as the DAUs. On the flip side, the local social company only has 8 million international WAUs during Q3’22. Nextdoor has substantial opportunity to grow beyond the current meager international user base.

These international numbers don’t monetize to a great extent currently, leading to some of the user growth recently without revenue growth. For Q3’22, international users grew from 5.8 million to 7.8 million WAUs for ~35% growth while revenue hardly grow YoY.

Roblox (RBLX) ran into similar problems recently where users were growing, but revenue and bookings struggled. Eventually, the U.S. user base returned to growth and, when combined with the higher international base, led to 20% bookings growth just reported in December.

Nextdoor ran into similar strong comps where Q3’19 revenues were only $20 million and the company printed $53 million by Q2’21 for over 150% total growth in just 2 years. The market is extrapolating too many negative outcomes into the nearly flat revenue growth in Q3’22.

The stock has a meager market cap of only $800 million with an enterprise value of just $200 million, at the end of September. The cash balance will definitely dip due to ongoing cash burn, but Nextdoor is only poised to burn $100 to $200 million over the next few years based on the current losses. With some cost cuts, the local social company could reduce adjusted EBITDA losses back to the $8 million quarterly rate in 2021 before management ramped up spending to capture a larger market opportunity.

In fact, the company had so much cash that the BoD just repurchased 23 million shares with $77 million in cash during the Q2/Q3 quarters. The stock definitely isn’t without risk due to the competitive ad market and questions on whether smaller firms will effectively monetize a user base as well as larger firms. Remember, Facebook monetizes at far higher rates than even Pinterest and Twitter providing enormous upside to ARPU to ever match the sector leader.

Takeaway

The key investor takeaway is that Nextdoor should’ve started the year with a big bounce similar to other beaten down former SPACs. The market appears far too focused on ongoing losses when the company doesn’t face a liquidity issue.

Investors should use this opportunity to buy the beaten down social media company trading below 1x EV/S for a sector where the average valuation is closer to 4x EV/S targets.

Be the first to comment