INDU BACHKHETI/iStock via Getty Images

Investment Thesis: Nexstar Media Group could see further upside from here on the basis of strong growth in Political Advertising revenue as well as growth in earnings and free cash flow.

In a previous article back in May, I made the argument that Nexstar Media Group, Inc. (NASDAQ:NXST) could see a potential rebound in revenue ahead – but that the company might also face some inflationary pressures.

However, this has not deterred the stock so far – with price up by nearly 20% since my last article:

investing.com

The purpose of this article is to elaborate on why I see further upside ahead for this company – particularly taking the most recent quarterly results into account.

Performance

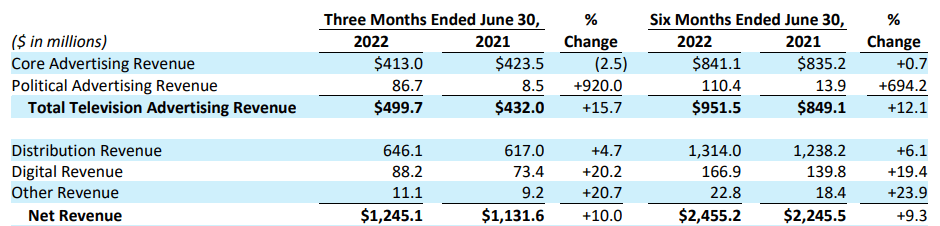

With U.S. midterm elections approaching in November, revenue is likely to continue seeing a significant rise given spend on political advertising. Already, we see a sharp increase in revenue for Q2 2022 as compared to last year:

Nexstar Media Group Q2 2022 Earnings Release

Moreover, for the six months ended June 30 for 2021 and 2022 – we can see that free cash flow to net revenue is also up slightly.

| June 2021 | June 2022 | |

| Net Revenue | 2245.5 | 2455.2 |

| Free Cash Flow | 664.7 | 779.4 |

| Free Cash Flow to Net Revenue Ratio | 29.60% | 31.74% |

Source: Figures sourced from Nexstar Media Group Q2 2022 Earnings Release. Free Cash Flow to Net Revenue Ratio calculated by author.

From this standpoint, while we have seen a strong seasonal boost in political advertising revenue – the fact that free cash flow has kept up with revenue growth is particularly encouraging.

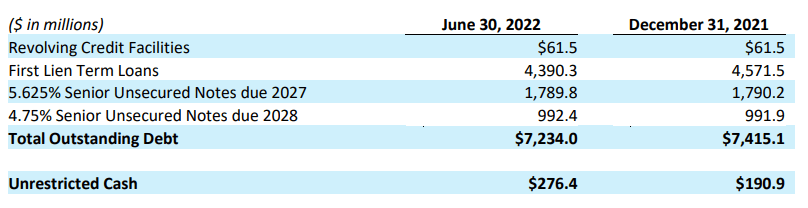

Moreover, the boost in cash flow has meant that the company has also been able to reduce its total outstanding debt by just over 2% as compared to December 2021.

Nexstar Media Group Q2 2022 Earnings Release

Looking Forward

With respect to the previous point that I made about inflation potentially affecting television subscription rates – I may have overestimated this risk as inflation can also potentially benefit the company going forward.

For one, the company has more scope to raise advertising prices under such an environment and thus further boost revenue growth. In addition, as a reader pointed out in my previous article – the fact that the company owns “over-the-air” TV channels still allows the company to draw in an audience and thus remain appealing from an advertising standpoint.

Previous Comment on Seeking Alpha

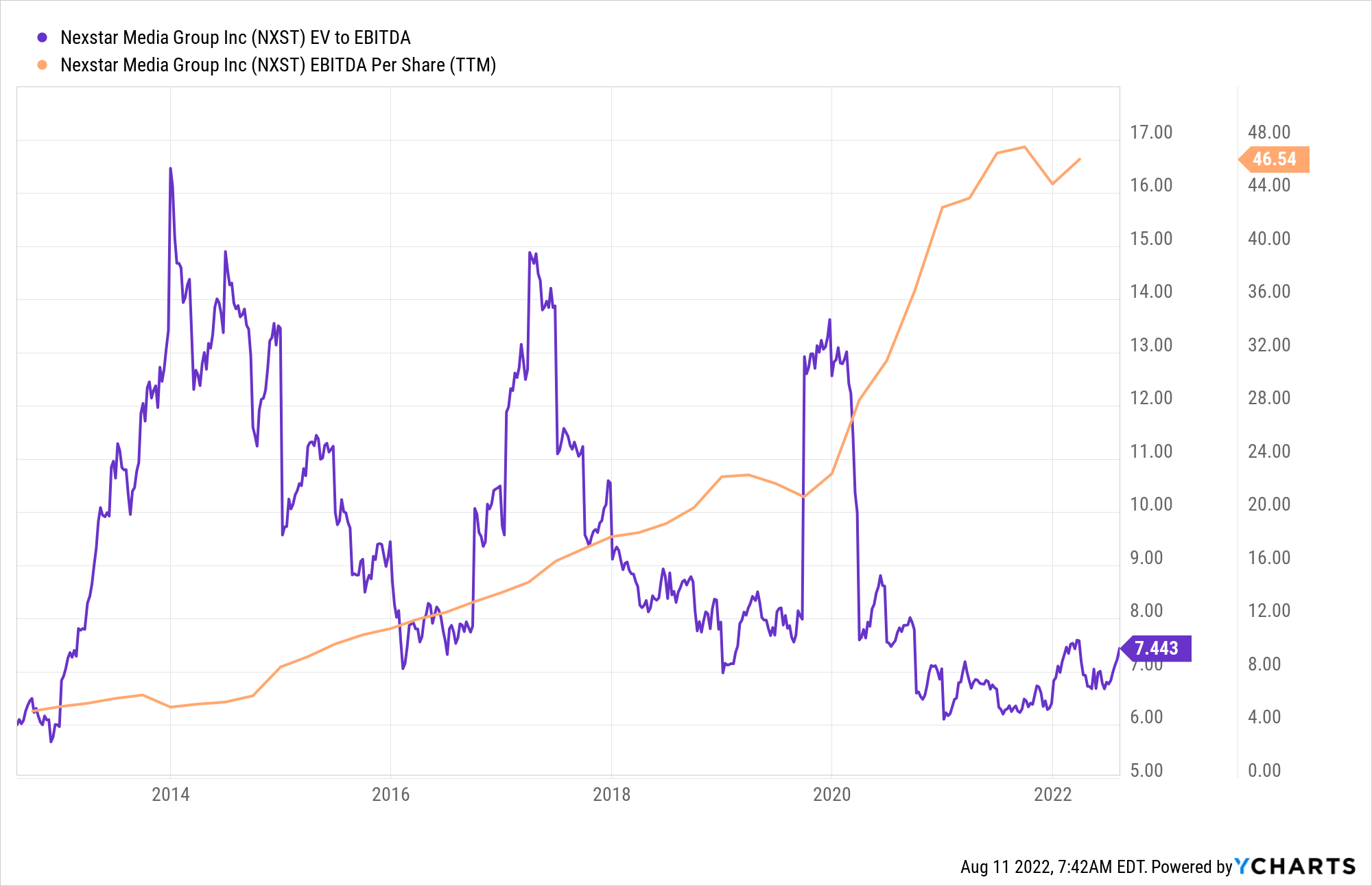

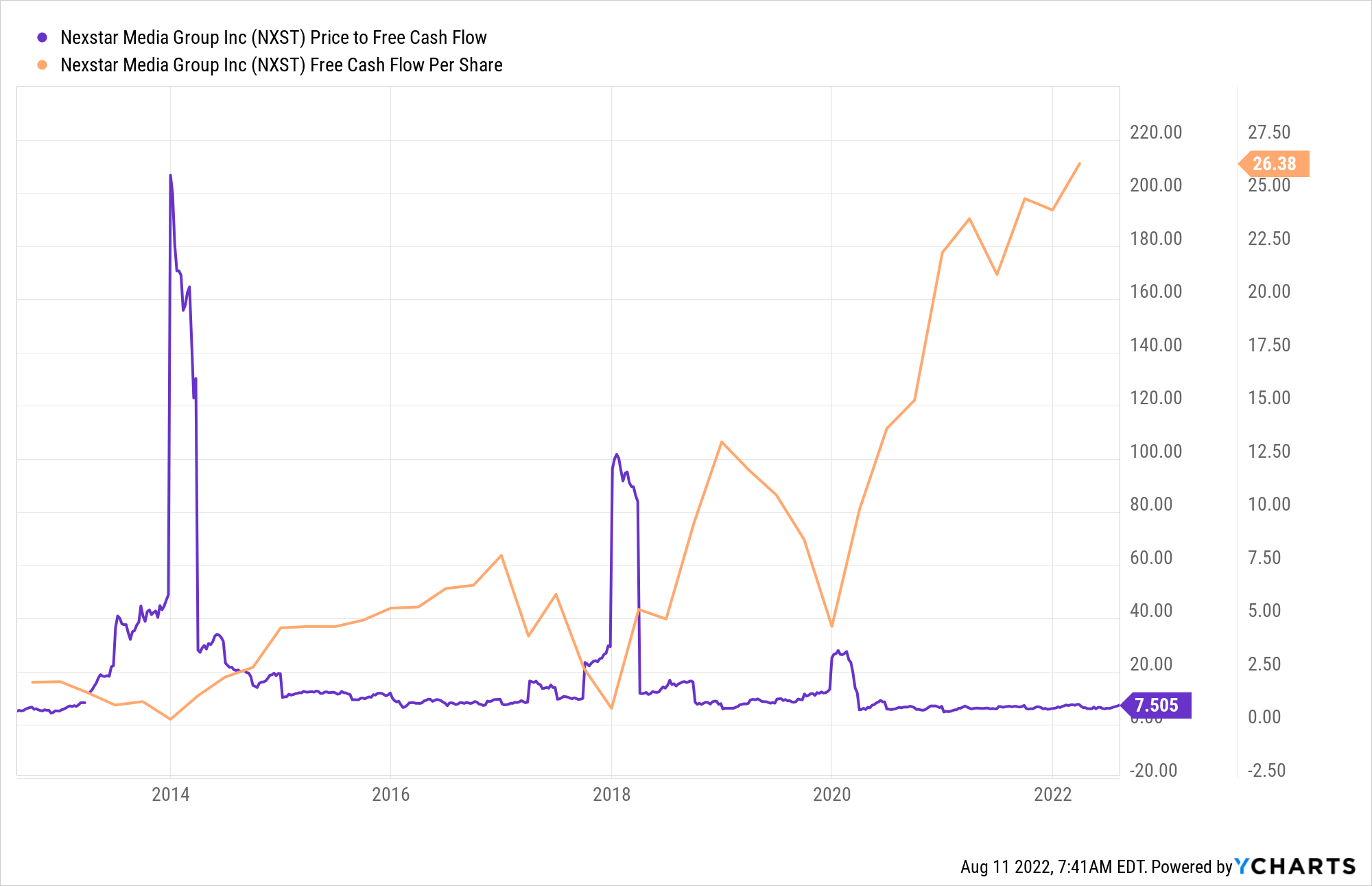

From a valuation standpoint, we can see that both earnings and free cash flow per share trade near 10-year highs – while EV to EBITDA and price to free cash flow trade near 10-year lows:

EV to EBITDA

ycharts.com

Price to Free Cash Flow

ycharts.com

In this regard, I take the view that given continued upside in earnings and free cash flow – the stock is in a good position to see further upside from here.

One potential risk for the company is the effect of a temporary drop-off in Political Advertising after November of this year – once the U.S. mid-terms conclude. While spend is expected to grow strongly in 2024 with the upcoming Presidential Elections – 2023 could be a relatively more quiet year for Political Advertising.

Additionally, we can see that while Political Advertising revenue was up strongly on that of last year – that of Core Advertising only grew marginally and in fact declined slightly on a three-month basis.

From this standpoint – should we see a plateau in earnings or free cash flow growth in the coming year – then this could lead to some downside for the stock.

Holistically, I take the view that the stock is set for further long-term upside given a boost in Political Advertising this year and in 2024, along with Nexstar Media Group also having the ability to raise advertising prices in line with inflation.

Conclusion

To conclude, Nexstar Media Group has continued to show impressive growth in both earnings and free cash flow. My overall view is that the stock will continue to see growth from here.

Additional disclosure: This article is written on an “as is” basis and without warranty. The content represents my opinion only and in no way constitutes professional investment advice. It is the responsibility of the reader to conduct their due diligence and seek investment advice from a licensed professional before making any investment decisions. The author disclaims all liability for any actions taken based on the information contained in this article.

Be the first to comment