Michael Nagle/Getty Images News

News Corporation (NASDAQ:NWSA) is a diverse media firm with operations in the US, UK, and Australia, owning well-known brands such as The Wall Street Journal, Herald Sun, and The Times. It is controlled by Rupert Murdoch and his family trust, who own 39.4% of the voting interest. NWSA has a rich history of growth, starting as a small newspaper in Adelaide and now owning two major media conglomerates globally. The company has a strong presence in the Australian pay-TV industry through its 65% ownership of Fox Sports and Foxtel, and leads the real estate classifieds space in Australia through its 61% ownership of REA Group. NWSA also owns HarperCollins, a leading book publisher, and has a significant digital property advertising business in the US through Move.

Q2 Earnings: Revenue Down 7% Despite Growth in Professional Information and Streaming Services, EBITDA Declines 30%

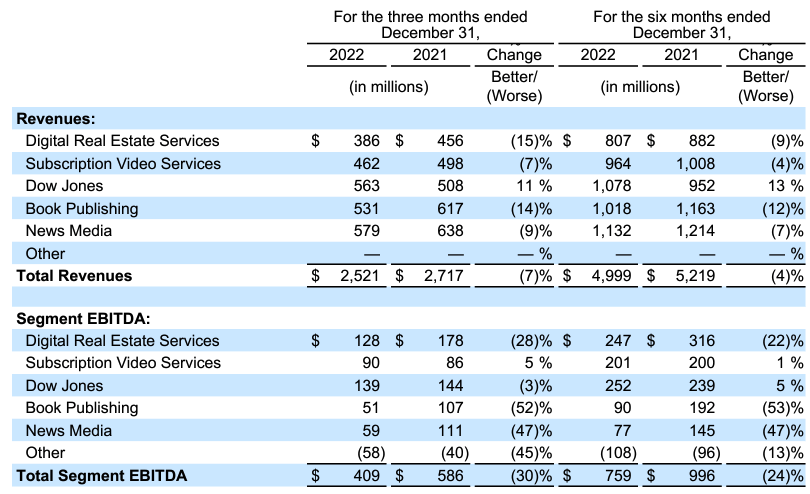

The quarter saw a 7% decrease in revenue, amounting to $2.52 billion compared to $2.72 billion in the previous year. The decrease was partly due to a 6% impact from FX. The total segment EBITDA for the quarter declined 30% to $409 million. At the Dow Jones segment, the professional information business saw a 45% increase in revenue due to the acquisition of OPIS and CMA and growth in its Risk & Compliance products. The Subscription Video Services segment also saw growth, with higher streaming revenues from Foxtel’s Kayo and BINGE offsetting broadcast revenue declines. The News UK segment saw continued growth from strong digital advertising revenue at The Sun, demonstrating the successful expansion into the U.S. and increased yield. The company is also engaged in discussions with CoStar Group regarding the potential sale of Move.

The drop in EBITDA highlights the company’s exposure to economic cycles. The decline, which was caused by unfavorable currency moves (17%) and other factors such as rising interest rates on digital real estate, declining sentiment in the technology and financial sectors on Dow Jones, softening consumer spending on books, and falling advertiser confidence on News Media, comes after the COVID-19 pandemic fueled a record high 18% rise in EBITDA a year ago. The EBITDA margin of 16.2% is much lower than the 21.6% achieved in the previous period, demonstrating the impact of cost inflation.

Company earnings release

Challenges in Evolving Publishing Industry

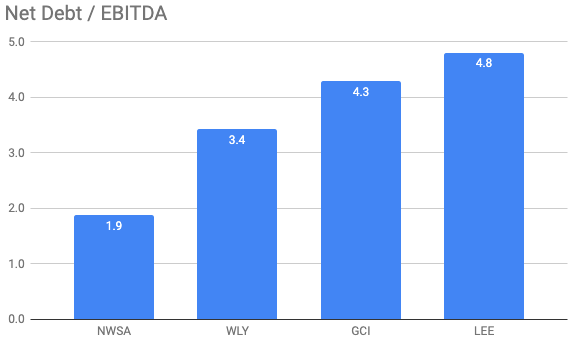

NWSA operates in an industry undergoing major changes, with the traditional print publishing model being disrupted by the abundance of news and information outlets in the digital space, made more accessible to consumers by technological advancements and device innovation. This presents significant challenges for NWSA as consumers shift from print to digital, with advertisers following suit. However, NWSA is better positioned than its publishing peers to make the transition, with well-established, respected brands and robust editorial resources compared to competitors who have been cutting back. NWSA is also financially stable, with the lowest leverage among its peers, it has the financial strength to transition to digital while exploring diversification opportunities.

Seeking Alpha

Despite the challenges facing the publishing industry, NWSA’s pay-television operations in Fox Sports and Foxtel provide some protection, though they too face growing pressure from digital streaming alternatives. NWSA’s REA Group has a strong growth outlook, and its digital property advertising business, Move, is making significant progress in the US market.

Navigating the Shift in Publishing Industry

The publishing industry, which constitutes a major portion of NWSA’s core earnings, is experiencing a major shift due to the growing influence of digital technology. The traditional dominance of the industry over consumers and advertisers is eroding as more people opt for digital sources for news and information, resulting in a decline in print-based audience and advertising revenue. This has forced many publishers to reduce their printing operations or shut them down entirely.

For example, The Tribune Publishing Company (owner of major newspapers such as the Chicago Tribune and New York Daily News) and Gannett Co. (GCI) (largest newspaper publisher in the US and owner of USA Today) have both reduced printing operations in response to declining revenue from print advertising and subscriptions. Tribune Publishing has cut print publication frequency, jobs, and consolidated printing operations, and in some cases, shut down print editions to focus on digital content. Gannett has reduced print publication frequency and consolidated printing operations while investing in digital growth through acquisitions and partnerships.

However, NWSA has some strong assets in its portfolio such as The Wall Street Journal and Fox Sports, which provide a solid foundation for the company. Additionally, NWSA’s investments in the digital video on demand space, specifically in the Kayo and Foxtel Now streaming services, are yielding promising results. Despite the challenges facing the legacy newspaper publishing business, it continues to generate substantial free cash flow, although at a declining rate.

NWSA’s low leverage and strong free cash flow position it well to weather the transition from traditional publishing to the digital age, and to explore other business opportunities.

Dividend and Share buybacks

Since 2015, the dividend has stayed at 20 cents per share as NWSA has used the cash to acquire new businesses. However, in September 2021 NWSA announced a USD 1 billion buyback.

Valuation

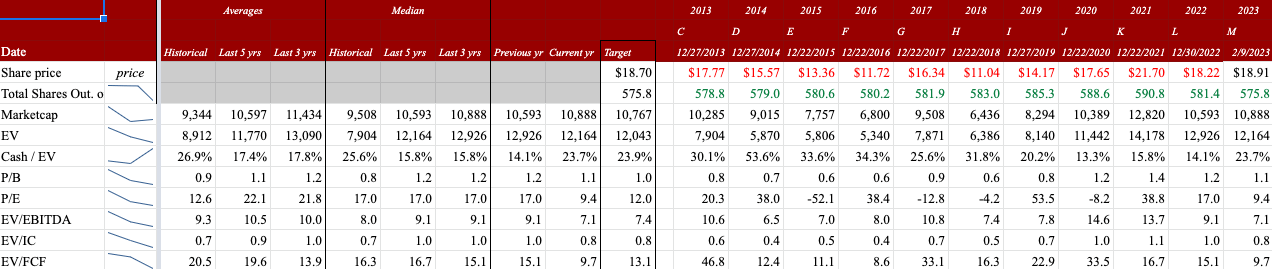

I think the shared are fairly priced as my fair value is $19 per share. I expect revenues to growth at 1% where the digital channel growth will be partially offset by the print media decline. I see a slight compression in margins moving forward. Below are my main assumptions.

Author estimates & company filings

At a share price of $19, the multiples are lower than historical. This makes sense due to the secular decline of printed media.

Author estimates, Seeking Alpha & company filings

Risk and Uncertainty

The advertising and marketing industry relies on the ever-changing corporate confidence and consumer sentiment. This is a major concern for the news media unit, which generates a significant portion of its revenue from advertising. As the current health crisis transforms into an economic crisis, other revenue sources, such as subscription video services and property-sensitive digital real estate services, may also be affected. A long-term challenge for NWSA is retaining its audience as the industry continues to shift to the online space. Even if the company can achieve this, it is important that its cost structure is adjusted to offset the reduced advertising revenue in the competitive digital market.

Conclusion

NWSA is in a strong financial position, with a solid balance sheet and steady cash flow. This stability sets it apart from other companies in the media industry and gives it the ability to adapt to the rapidly changing digital media landscape. The company’s portfolio of successful online real estate classified businesses in Australia and the U.S. contributes to its cash flow.

However, the publishing industry continues to face major challenges from technology and innovation changing consumer behavior and preferences. Although the company is trying to adapt its business model and monetize online content, it may still be affected by external factors. NWSA’s strong financial position provides some cushion, but acquiring assets to diversify earnings could be expensive. Overall, I believe the shares are priced fairly and recommend staying on the sidelines.

Be the first to comment