Mohamad Faizal Bin Ramli

Introduction

Despite seeing a decent start to 2022, it ended up being a tough year for the gold mining industry as central banks rapidly tightened monetary policy to combat inflation. Due to these headwinds, it was unavoidable that Newmont (NYSE:NEM) would see their share price soften in tandem. Although, like many times in life, this is a double-edged sword and therefore, their shares offer great insurance for the everyday investor wishing to hedge against the likelihood of weak economic conditions on the horizon in 2023.

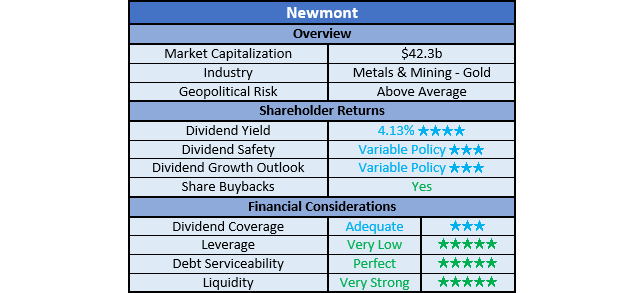

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

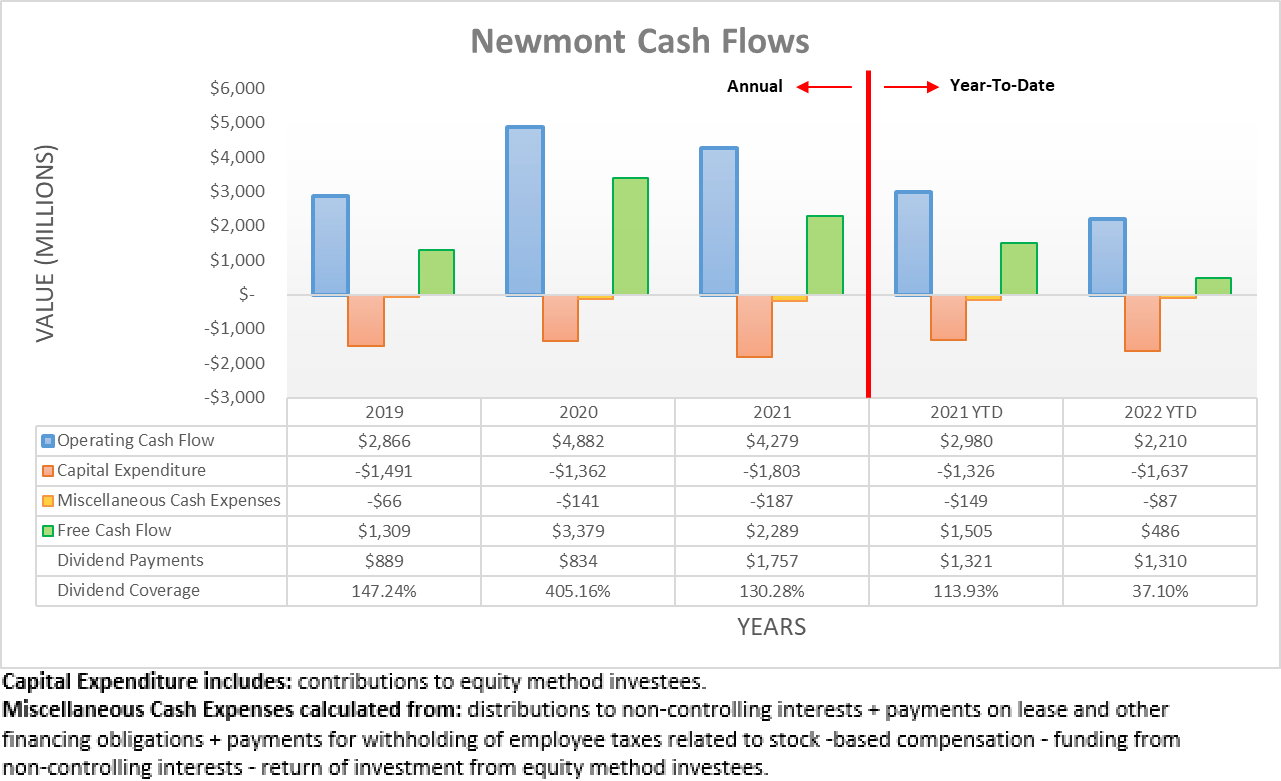

When reviewing their cash flow performance, quite unsurprisingly, it varied across the years along with gold prices. Most recently during 2022, the first nine months saw their operating cash flow land at $2.21b and thus down almost 26% year-on-year versus their previous result of $2.98b during the first nine months of 2021, which largely stemmed from softer gold prices. Although, the extent of this decrease was also partly due to even larger working capital movements during the first nine months of 2022, both in absolute terms and relatively speaking.

Author

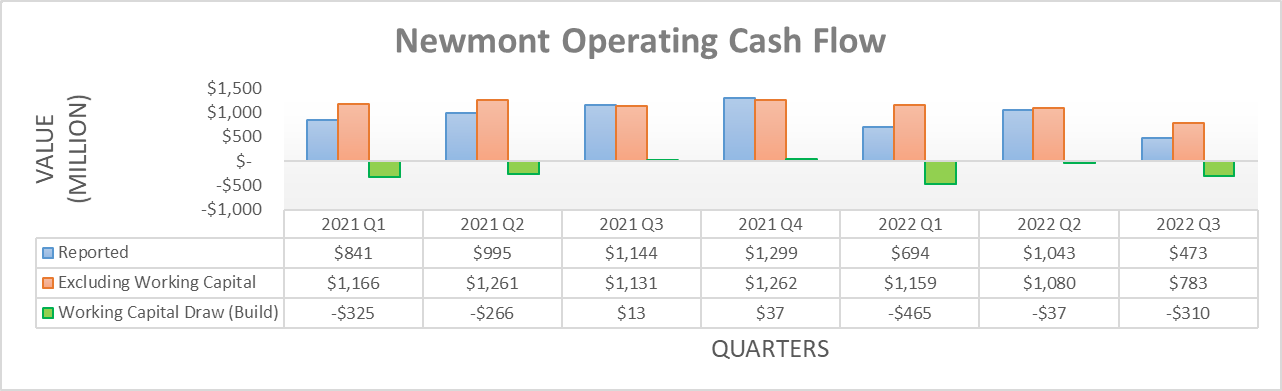

This dynamic is easier to view on a quarterly basis with the first, second and third quarters of 2022 all seeing respective working capital builds of $465m, $37m and $310m, which aggregate to a build of $812m. Whereas, the first, second and third quarters of 2021 saw respective builds of $325m and $266m, plus a draw of $13m, which ultimately aggregates to a build of $578m. If both of these were excluded from their reported results, it leaves their underlying operating cash flow at $3.022b during the first nine months of 2022 and thus sees a less significant decrease of circa 15% year-on-year versus their previous equivalent result of $3.558b during the first nine months of 2021.

Whilst their working capital movements increase their cash flow performance lumpy, this is par for the course in the mining industry, especially due to the inherent volatility of commodity prices. To their credit, they have still managed to consistently generate free cash flow every year since at least the beginning of 2019, which is impressive given the wide range of operating conditions and capital-intensive nature of their industry. Even though lumpy cash flow performance is not ideal and will never go away, mining companies are not sought for steady cash flow performance but rather, their value resides within offering easy-to-access exposure to the underlying commodity that is obviously the primary driver of their share price.

When looking ahead into 2023, there are many uncertainties that can keep investors awake at night but I suspect, most notably is the prospects for a recession or if not, weak economic conditions as the economy slows on the back of the now far tighter monetary policy. Gold prices can be swayed via different factors but as 2022 proved, quite possibly the most important factor is actually monetary policy, largely headed by the Federal Reserve in the United States. Following the inflationary shock of the Russia-Ukraine war in early 2022, the resulting inflation shock saw central banks rapidly tighten monetary policy, which in turn hindered gold prices as the year progressed.

Whilst a painful experience during most of 2022, in recent weeks, gold prices have been heading north as the market begins expecting the Federal Reserve to ease its tightening as inflation data shows signs of slowing, although this consumer price stability is likely to be accompanied by weaker economic conditions. As a result, this raises prospects of stronger gold prices during 2023 because as a rule of thumb, the worse the economy performs, the more dovish central banks will become and thus by extension, the higher the probability of stronger gold prices, which in turn makes their shares great insurance for the everyday investor. If economic conditions weaken more than expected, which is always a risk, having exposure to gold prices should act as a hedge to help increase portfolio stability or alternatively, maybe even allow investors to profit outright, depending upon their weightings and other exposures.

Whilst billionaires have unfettered access to any form of investment, the everyday investor with far less capital does not necessarily have as many options, or as ease of access to certain options. When it comes to gold, it is not necessarily a simple process to store physical gold and if outsourced, will obviously incur costs that impose a drain on the investment. Likewise, gold ETFs simplify this process and increase liquidity via being market traded but at the same time, they still incur annual costs, similar to every other ETF.

Admittedly, it is true that holding gold exposure via a gold mining company increases operational risks at the company level versus holding physical gold, such as strikes or natural disasters. Although on the flip side, unlike storing physical gold or owning gold ETFs, holding their shares allows the investor to receive dividends that easily offsets this additional risk, at least in my eyes.

Newmont Third Quarter Of 2022 Results Presentation

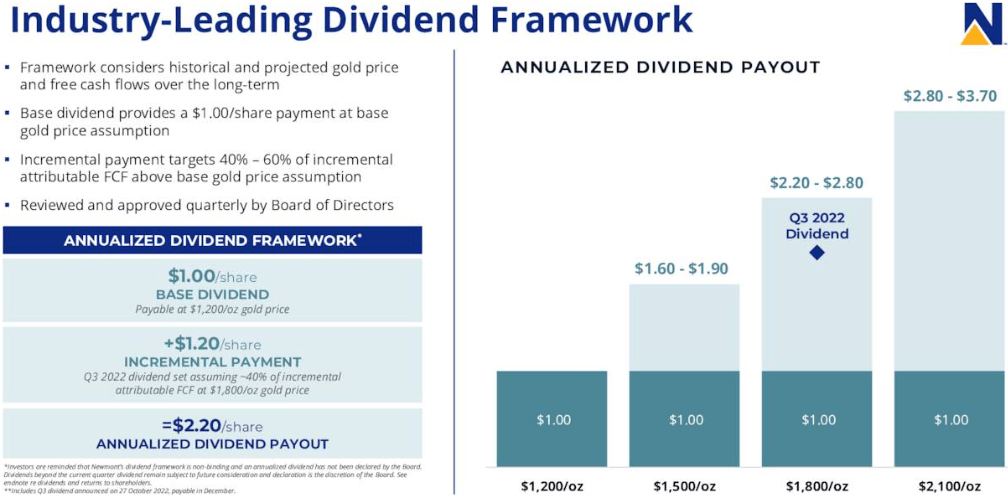

To handle the unavoidable volatility of the gold mining industry, they have implemented a variable dividend policy, whereby their dividends scale accordingly with the prevailing gold price. Apart from rewarding shareholders during the good years, this also helps reduce the pain during the bad years as it lessens their cash outflows and therefore, helps support their financial position that itself, also helps further decrease their operational risks.

Author

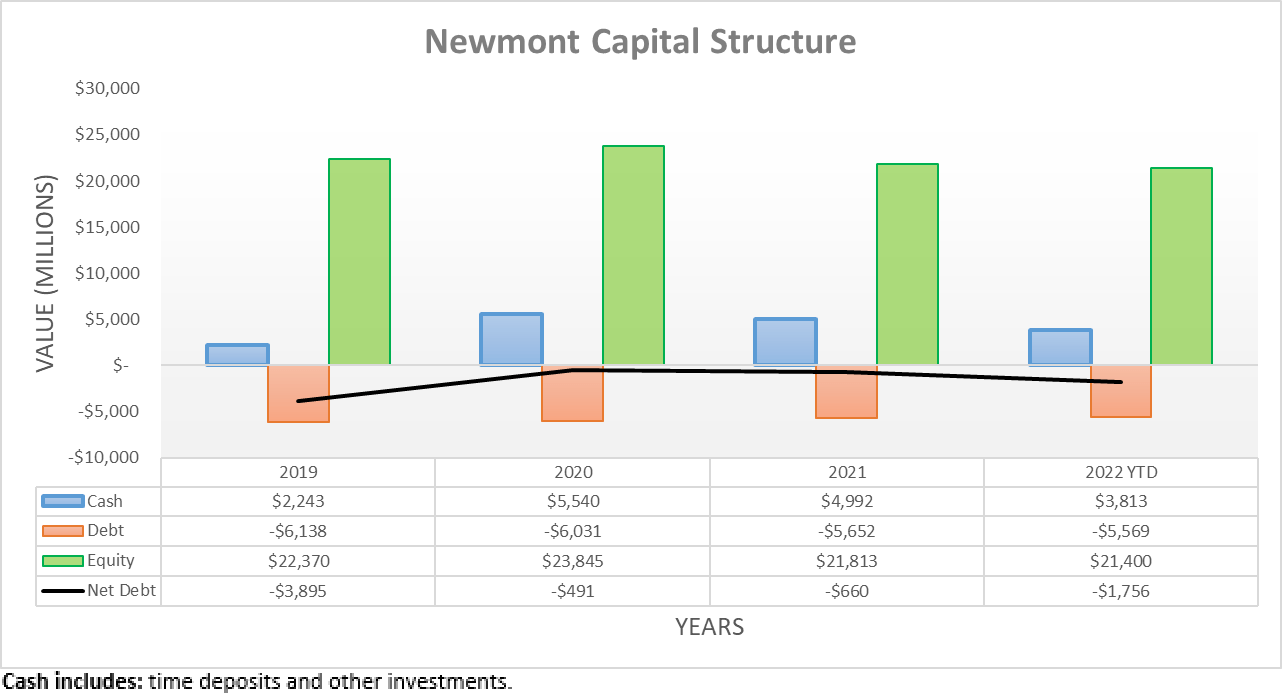

After rapidly deleveraging several years ago back during 2019 and 2020 and almost eliminating their net debt, they have taken a more lax approach towards their capital structure, thereby allowing their net debt to begin edging higher as the years pass. As a result, it is now back to $1.756b following the third quarter of 2022 versus its previous levels of $660m following the end of 2021 and $491m following the end of 2020, although it nevertheless remains far below its previous level of $3.895b following the end of 2019.

Author

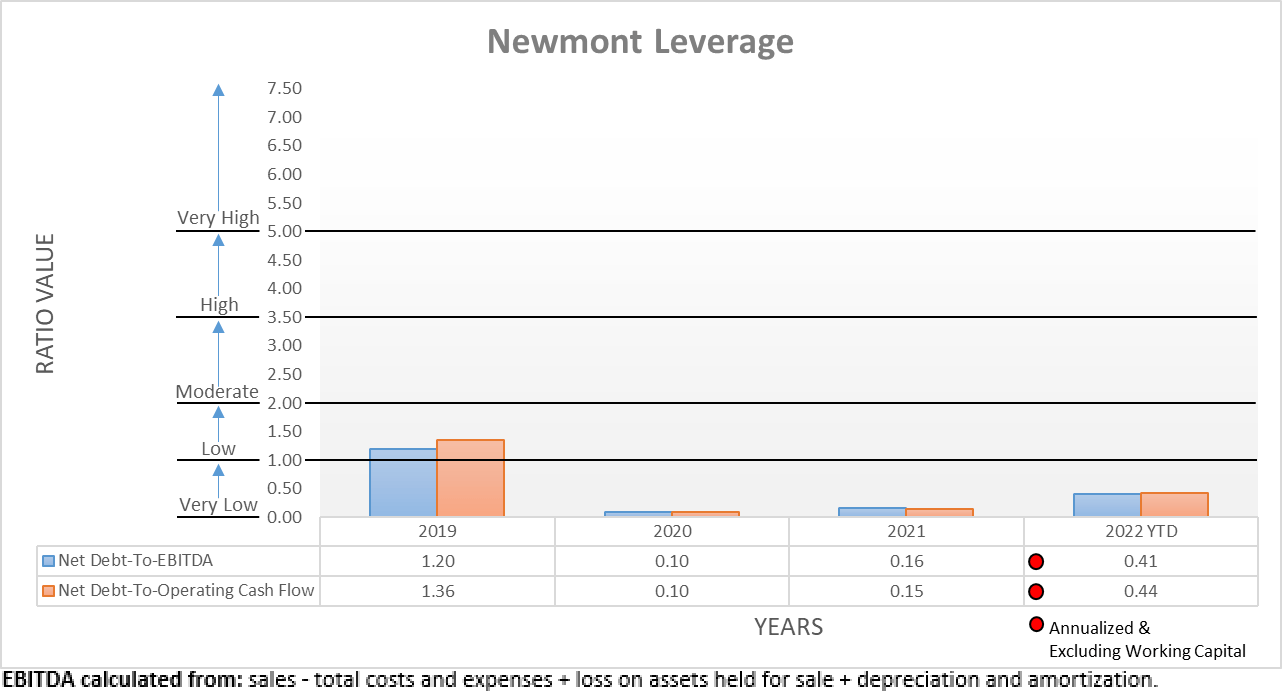

Despite seeing softer financial performance during the first nine months of 2022 and modestly higher net debt, impressively, their leverage remains very low. To this point, their net debt-to-EBITDA landed at 0.41 with their net debt-to-operating cash flow following not far behind at 0.44 and thus, both are easily beneath the threshold of 1.00 for the very low territory. Even if the prospects for stronger gold prices in 2023 were to be completely wrong, their very low leverage significantly limits the downside risk as they can safely handle much higher leverage without it posing any solvency issues.

Author

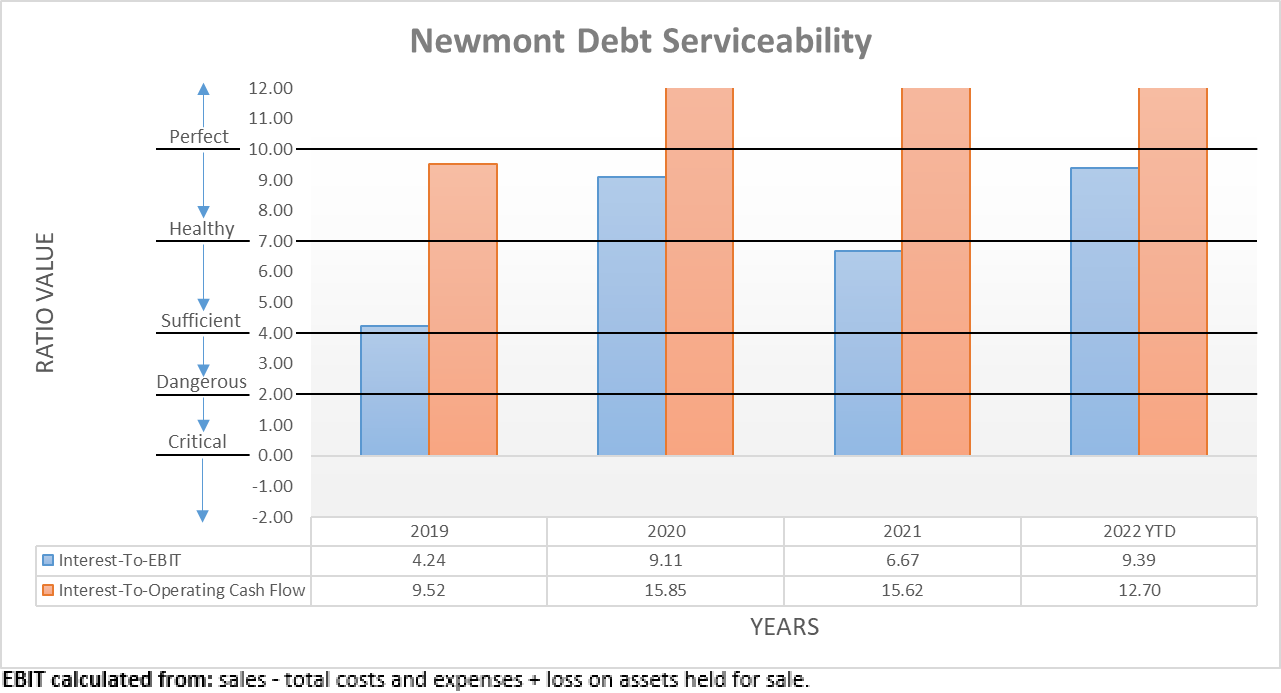

Quite unsurprisingly, the strength afforded by their leverage translates into their debt serviceability that enjoys perfect interest coverage. Regardless of whether compared against their EBIT or their operating cash flow, the respective results of 9.39 and 12.70 are not worrisome and once again, this further helps support their financial position in the same manner as their very low leverage.

Author

Further cementing their financial position is their very strong liquidity, which sports a current ratio of 2.72 and most importantly, a cash ratio of 1.64. Even if weak gold prices were to spoil 2023, this ensures they would have zero problems navigating the year and when combined with their very low leverage, it also helps remove any issues regarding debt maturities within the foreseeable future. That said, as one of the largest gold mining companies, if required, they should still be able to easily access debt markets to bolster liquidity, regardless of where monetary policy heads.

Conclusion

A rock-solid financial position helps limit downside risk during downturns as the market does not see solvency issues and just as importantly, it also increases their appeal during better years as they can return more cash to shareholders instead of repaying debt. When combined with the solid history of generating free cash flow, I feel they make great insurance for the everyday investor who does necessarily have the means to store physical gold and would prefer to see dividends that physical gold ETFs simply cannot provide and thus, I believe that a buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Newmont’s SEC filings, all calculated figures were performed by the author.

Be the first to comment