JHVEPhoto

Investment Thesis

Newell Brands Inc’s (NASDAQ:NWL) sales growth should get adversely impacted by lower consumer demand, weakening discretionary spending, and retail inventory destocking. Margin should also get negatively impacted by inflationary pressure and volume decline in the near term. However, the company’s efforts of price realizations, productivity improvement, and overhead cost reductions should support margin recovery in the back half of FY23 and beyond. NWL is trading at a discount to its historical valuation. However, despite the low valuation, I prefer to be on the sideline due to near-term headwinds and have a neutral rating on the stock.

Revenue Outlook

Post-pandemic, NWL’s sales benefitted from accelerated discretionary spending driven by stimulus checks and increased demand in the home appliances and home solutions segment. As the economy gradually re-opened, increasing demand for writing and commercial business due to schools and offices reopening also added to sales growth.

However, the company started experiencing demand softening across the majority of its product categories in Q2 2022. This was due to lower consumer confidence in an inflationary environment and fading benefits from the stimulus-driven demand in the previous years. The company also divested its low-performing Connected Home and Security (CH&S) business in the commercial solution segment which also affected the top-line growth. The net sales trend worsened in Q3 with inventory destocking at retailers further exacerbating sales declines.

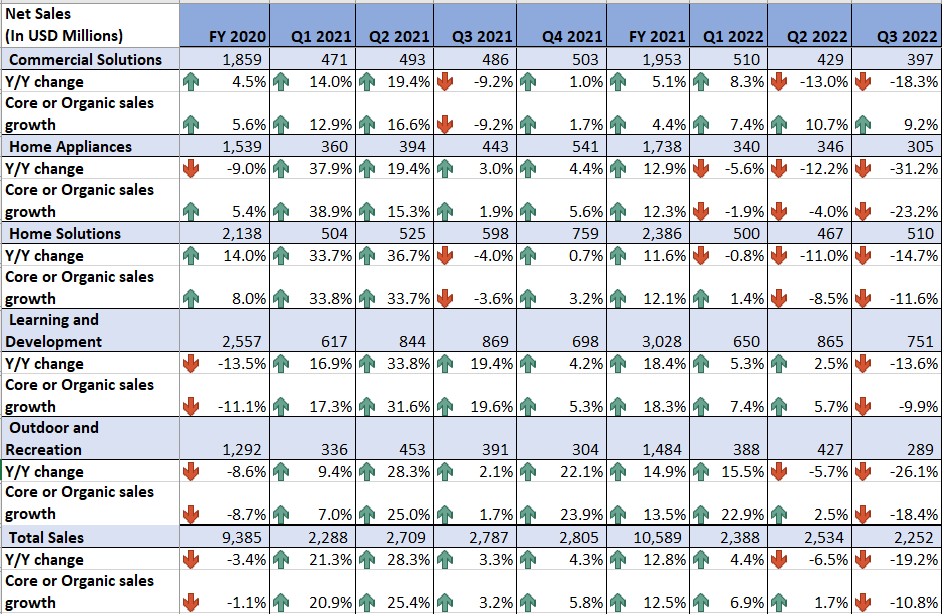

NWL’s Historical Net Sales (Company Data, GS Analytics Research)

Looking forward, I believe weakening consumer discretionary spending due to the inflationary environment and higher interest rates should impact NWL’s sales in the coming year. I also believe retail inventory adjustments, particularly for general merchandising products which started in Q3 last year still have some legs and should continue to impact sales growth moving further into 2023. Further, NWL is also facing headwinds in its international business from adverse FX movements. The company is planning to offset it with additional pricing in the international markets, which could lead to further volume decline overseas as well.

While the company continues to work on initiatives like product innovations to drive growth, I don’t think they will be able to offset the near-term headwinds. So unless the macroeconomic environment improves, I have a pessimistic view of the company’s revenue growth prospects.

Margin Outlook

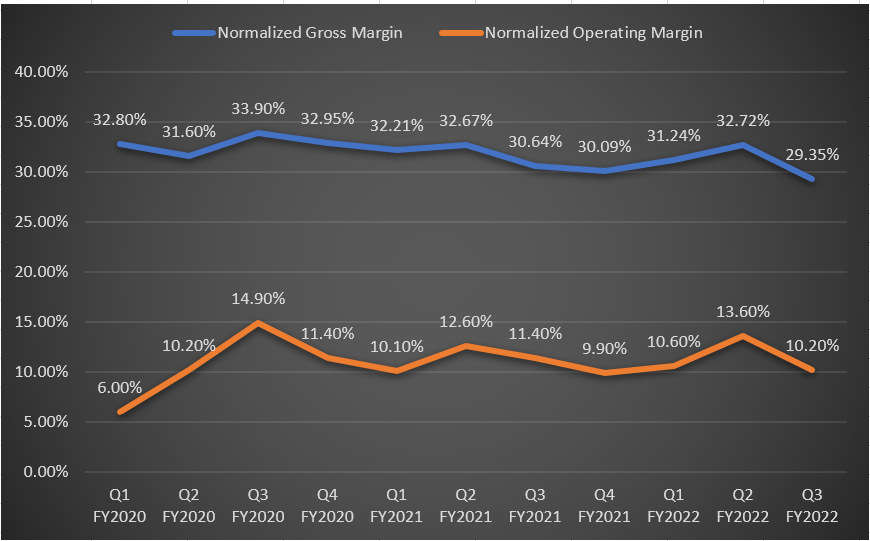

Like many other companies in the consumer sector, Newell’s margins were also impacted by inflationary headwinds since 2021. The company’s cost reduction initiatives and pricing increase helped it improve its margin in Q2 2022. However, a sharp decline in revenue in Q3 2022, led to a significant volume decline which resulted in a ~130 bps Y/Y decline in normalized gross and ~120 bps Y/Y decline in normalized operating margin in the quarter.

NWL’s Historical Adjusted Gross and Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking forward, the company continues to work on productivity initiatives like managing discretionary expenses, optimizing advertising and promotional spending as well as the company’s office footprint, reducing complexity by rationalizing SKU count, and redirecting investments towards higher margin business. These productivity initiatives coupled with price increases should help margins.

However, I believe volume deleverage will still be a big concern, at least for the next couple of quarters. If we look at consensus estimates, the sell-side is modeling revenues to decline over 20% in Q4 2022 and over 14% in Q1 2023. So, I expect margins to continue declining Y/Y in the near term. However, in the second half of FY 2023, we should begin seeing some improvements as comparisons become easier and management’s productivity initiatives continue to take hold.

Valuation And Conclusion

NWL is currently trading at a forward P/E of 10.57x FY 2023 consensus EPS estimate of $1.43, which is at a slight discount to its historical 5-year average forward P/E of 11.57x. The weakening consumer demand in the majority of the company’s product categories, retail inventory adjustments, volume decline, and an inflationary environment are major headwinds for the company’s revenue and margin growth in the near term. Hence, despite the low valuation, I would prefer to be on the sidelines until the revenue declines bottom and have a neutral rating on the stock.

Be the first to comment